The Asia high yield market is now in a fundamentally different place to a few years ago as the distress in the China property sector has faded, according to Stephen Gough, managing director, portfolio manager and head of the Asia Liquid Credit Platform at BlackRock.

“Asia high yield has been persona non grata for a long time because of the challenges of the defaults in the Chinese property sector in 2021 and 2022 and also China being shut from the rest of the world. Other sectors like Macau gaming are big parts of that index and obviously they weren’t having visitors,” he said.

“It was a bit unloved after two years of bad returns. But as you pick through the credit, the Asia high yield market is now in a different place in the sense that it’s far more diversified, which makes it a more palatable opportunity.”

After two years of poor returns, during the first half of the year, Asian high yield was actually one of the standout performers as US dollar-denominated Asian high-yield bonds delivered a 10.5% total return compared with just 2.5% from US high yield and 3.2% from global high yield.

In fact, most of this was driven by a rally in distressed names including China property as well as various frontier sovereign bonds.

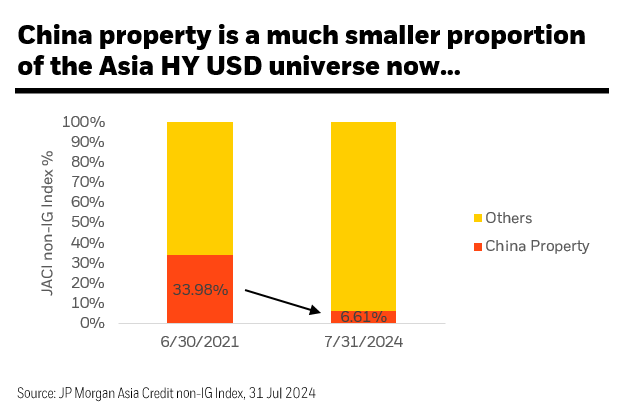

When the property crisis in China first hit, the sector accounted for more than a third of the JP Morgan Asia Credit Non-Investment Grade index compared with just over 6% now (see chart).

While Gough sees opportunities in China property because the ones that have survived are in a far better position, overall he is keen to point out that China property remains a much smaller part of the overall index and the outlook for the asset class as a whole is benign.

“Ultimately, what you have is still wider spreads than DM, you have predominantly a double-B index, which is pretty safe. It’s very rare that double-Bs move through the spectrum to default. And the third thing you have is despite all these positives, actually it is a market where a lot of the companies have cash and so they don’t need to come to market. So, you have this positive technical of cash being returned,” he said.

He also emphasises that the overall macro backdrop in Asia is positive, despite concerns about slowing growth and depressed consumer spending in China.

“Yes, China may be slowing more than people would like but ultimately it’s still growing. We’re talking about whether it’s growing 4% or 5% rather than whether there is a recession. So, still the backdrop is pretty supportive for the region and we haven’t had that inflation problem like in DM. As the Fed cuts, I do believe more central banks here will follow and again that will be supportive,” he said.

In terms of sectors, most of Gough’s calls are in line with market consensus such as financials, Macau gaming and Indian renewables, although he noted that in the last couple of months the firm had been trimming its exposure to those sectors.

He also noted that some of the firm’s Asia fixed-income strategies were overweight high yield compared with investment grade and had been taking more off-benchmark exposure, particularly in Australia and Japan”

“We’ve looked at Japan, which traditionally wouldn’t sit in our benchmark; not huge sizes but to just give us a little bit more breadth because ultimately what we’re trying to do is buy this mispriced credit spread and that’s been quite good for us,” he said.

“We’ve been looking at things like Australian RMBS, where we can buy triple A-rated securities at a spread of 120-130bp, where there are no triple A-rated securities in the JACI index, but a single A would probably be at 50 to 70bp. So we can pick up extra spread, probably taking less credit risk and certainly taking less volatility.”