As inflation falls and the Federal Reserve begins to cut interest rates, BlackRock strategists say investors need to be nimble and seize new opportunities as they arise.

The BlackRock Investment Institute said in a recent note they are now overweight euro area high yield credit, US dollar-denominated emerging market debt and US stocks.

The strategists cited a more “supportive backdrop for risk-taking anchors” as the primary reason. “We had preferred investment grade credit but now eye fixed income where spreads haven’t tightened as much,” they said.

Indeed, over the past year, US treasury bonds as well as other developed market (DM) sovereign bonds have been unusually volatile on the back of uncertainty surrounding monetary policy and inflation.

Despite this backdrop, spreads have steadily tightened as the future of inflation and monetary policy grows increasingly more predictable.

The strategists said: “Even as sovereign bond yields were volatile over the past year, the spread between them and credit yields has tightened steadily.”

This is why they shifted to an underweight view on global investment grade (IG) credit in September of 2023.

“That change funds risk taking in pockets of credit where the risks seem better compensated for,” they explained.

“We favor high yield and stay neutral: Its yield is attractive and returns are less sensitive to interest-rate swings.”

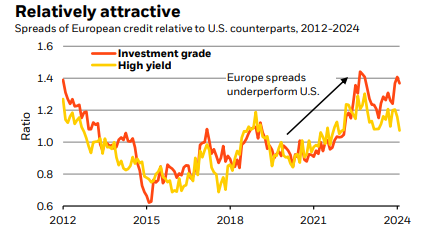

One trade they prefer is European credit over US credit, given the difference in spreads between European credit compared with their US counterparts.

“US IG and high yield credit spreads are further below their 10-year average than European peers,” the strategists said.

“European spreads have underperformed since 2020 partly due to a different sector composition and weaker growth in Europe, in our view. Yet we think the excess yield in European credit compensates for the risks.”

The strategists expect markets will embrace a more supportive near-term outlook going forward, anticipating inflation to fall near the Fed’s 2% target this year.

But beyond 2024, they argue markets will be faced with resurgent inflation which will come into view later this year.

“Robust US growth, nearing Fed rate cuts and falling inflation have lessened the market’s recession worries. That’s good news for emerging market (EM) assets, in our view,” they said.

As such, the firm is now overweight EM hard currency debt – mostly denominated in US dollars, since spreads look “more fairly valued” than US high yield.

They expect broader credit spreads to remain tight for now given the supportive macro backdrop, and strong demand for new issuance of US investment grade and high yield credit bonds.