Japanese equities may seem like a consensus amongst many asset managers, but it is still only in narrative and has yet to appear in positioning.

This is because most global equity strategies are still underweight the region, according to Yue Bamba, head of Japan active investments at BlackRock.

“People are still underweight, so the pressure from a positioning perspective is still for it to go up,” he told FSA in an interview. “It’s consensus in the narrative, but not in the positioning.”

“Japanese equities have done well, but we feel pretty strongly that positioning is still too light.”

The MSCI World Index has just 6% allocated to Japanese equities, whereas the average global equity fund has only 4.68% allocated to the region, according to data from FE fundinfo.

Since this figure includes many passive exchange-traded-funds (ETFs) with a mandated 6% allocation, it suggests the average active global equity strategy has even less allocated to Japan.

Japanese equities have rallied 28.7% over the past year, compared to 13.2% from the Asia ex Japan index and 24.1% from the MSCI World index.

Despite the strong rally over the past 12 months, some managers managers argue there is still upside due in Japanese equities to the positive long-term structural trends.

Improving corporate governance regarding shareholder returns, an improving macroeconomic backdrop and a plethora of high-quality listed companies in Japan are often cited as key reasons.

When discussing Japan with BlackRock’s clients, Bamba said: “the question that we get a lot is: is this real? How much longer is this going to go on for? Did we miss the trade? Japanese equities have already done quite well.”

“Our answer to that of course, is that it is structural and it’s going to go on.”

Since Japanese corporate governance reforms started to gain traction a year ago, Bamba said client interest has shifted more from “what’s going in Japan?” to “I want exposure to Japan, what are some practical ways of doing that?”

“It definitely feels like the interest is becoming stronger and more concrete,” he said.

Despite the attractiveness of small-cap Japanese equities, it is still large caps that have been attracting more attention among clients, Bamba added.

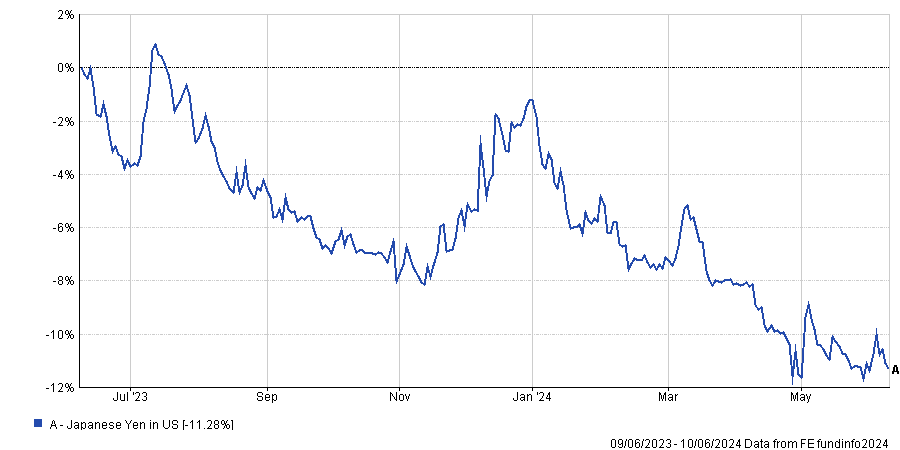

One issue however that does come up a lot during conversations with investors is concern over the risks posed by the Japanese currency.

The Japanese yen has declined 11.3% relative to the US dollar over the past year, offsetting significant gains for US-dollar denominated investors.

“We think FX is a bit of a side show. FX is not what investors should be focused on too much,” Bamba said.

“All the fundamental drivers of the market: inflation, deflation, growth – all those things have nothing to with FX.”

“In the past, you know, we’ve had FX induced rallies, exporters doing well on a weaker Yen, etc. but this one is much broader than that.”

He pointed to the breadth and strength of the current Japanese equity market rally, which has seen auto manufacturers, semiconductor companies, banks and construction companies all perform well.

“It’s important that you have the domestic sectors contribute to the rally as well because it makes it so much broader,” he explained. “That is what’s happening right now, which is new and different to prior rallies.”

One reason why many global active managers have yet to increase their allocation to Japan may be due to the slow-moving nature of the asset management industry, he added.

“Most of our clients are long-term investors, and long-term investors take time to choose an allocation and to complete their due diligence process, select a manager, deploy the capital.”