The recent downturn in biotech stocks may be one of the worst in the history of the sector, but it is proving to be a fertile hunting ground for some funds.

“Biotech is actually the sector with the highest dispersion and therefore the most mispriced securities,” said Agustin Mohedas, a portfolio manager at Janus Henderson. “So, it’s the biggest opportunity to generate alpha of any sector.”

There has been a tendency for biotech companies to go public earlier in their lifecycle, a trend that was exacerbated by the latest era of easy money following the Covid pandemic.

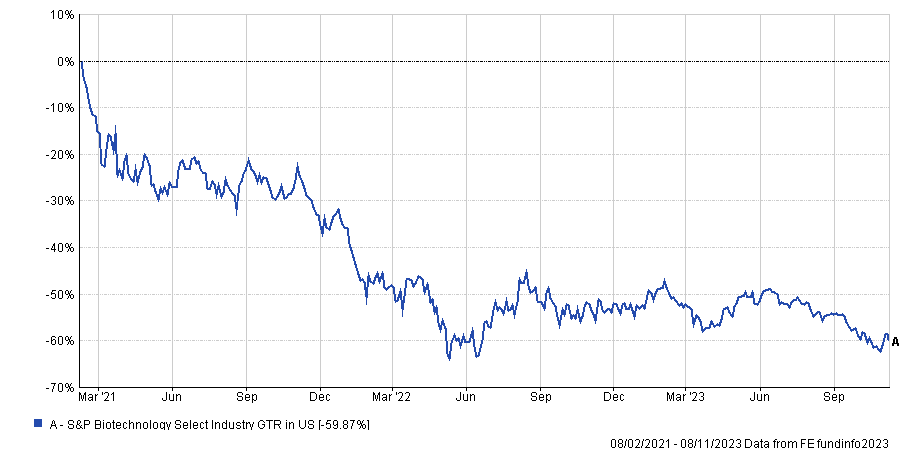

Many biotech executives saw an opportunity to raise money during a boom period for the sector and wider equity market, but since then, biotech stocks are down roughly 60% from their peak in 2021 as higher interest rates start to bite for many newly listed biotech companies with no clear path to commercialisation.

However, this has given some active managers, such as Mohedas (pcitured), a much larger universe of stocks to not only buy when they are overlooked and beaten down, but to short when they are doomed to fail.

The dispersion and the potential to capture “the full opportunity set of biotech” is why Mohedas’ team was “really excited” to have both public longs and shorts when Janus Henderson launched its Biotech Innovation Fund at the end of 2019.

The gap between the biotech winners and losers is the biggest of any industry in public markets. Over the past decade, the top five performing stocks in biotech on average were up 287%, whereas the bottom five on average were down 78%.

“Our job is to pick more of those winners and avoid or potentially short those losers,” Mohedas told FSA.

According to an investor presentation from Janus Henderson, the Biotech Innovation Fund posted returns of 33% and 23.9% in 2021 and 2022 respectively (before fees), mostly thanks to its short book. By comparison, the SPDR S&P Biotech index was down 20.5% and 25.9% in 2021 and 2022.

These figures have contributed to the fund’s impressive longer-term track record. As of the end of Q3 2023, the fund has returned 315% net of fees since launch, versus a 23% loss from the SPDR S&P Biotech index.

Still reason for caution in biotech

But despite an extended bear market, Mohedas said the hedge fund remains more tilted towards short positions than usual, running close to a 60% net long allocation (it typically operates between 60% and 80% net long).

He said the reason for this positioning is due to the headwinds that still exist for the sector, namely the rising interest rate environment and potential for a recession next year in the US.

“Those tend to be kind of ‘risk off’ environments for biotech so we’re still cautious,” Mohedas said.

Although he is optimistic about the biotech companies in the fund’s long portfolio which he believes are “on sale” with “great drugs” and “great launches” ahead of them, he thinks there are a large set of biotech companies out there with much bleaker outlooks.

“They maybe have products that don’t have really good clinical validation, or products that are not competitive or too late to market – where the companies are burning too much capital relative to the market cap, or where they just have drugs that we think are going to fail during their clinical development, or that the FDA is not going to approve,” he said.

“We look for all those risk factors and we create a short portfolio of individual securities… and we use that short portfolio to help hedge our long book in cases of when the market sells off.”

“Because our short portfolio tends to be these lower quality companies, our short portfolio during market downturns really outperforms and helps insulate our long portfolio and provides us cash to buy more of our favourite long ideas.”

According to Janus Henderson’s Dan Lyons, one of the portfolio managers on the team, some biotech companies have been resilient in the wake of central bank rate hikes and a slowdown in funding, thanks to coming out with “truly innovative data”, making them able to able to “control their own destiny”.

Even amid a rising interest rate environment these biotech firms have been able to raise the necessary money and go forward with their programmes alone – setting them up to negotiate well in the event of a future M&A deal, Lyons explained.

“On the flipside, we’ve seen the have-nots with either disappointing data, or poor balance sheets, or too much opex [operating expenses] really struggling in this environment,” he added.

“And there are a lot of companies in the index that need to be cleaned up. We call them zombie companies that maybe they have some cash left, but not much else.”