Investor confidence in Japanese equities hasn’t been swayed by the Bank of Japan’s decision to raise interest rates for the first time in 17 years.

On Tuesday the BoJ increased its key interest rate from -0.1% to a range of 0%-0.1% after seeing evidence of strong wage growth following a long-awaited increase in consumer price inflation.

Although many economists said the dovish hike from the Japanese central bank occurred earlier than expected, some investors believe the policy shift signals a “new horizon” for Japanese equities.

“The BoJ’s policy shift is part of a careful and considered normalisation of monetary policy and not a knee-jerk leap into monetary tightening, in our view,” said Ben Powell, Chief Apac strategist at the BlackRock Investment Institute.

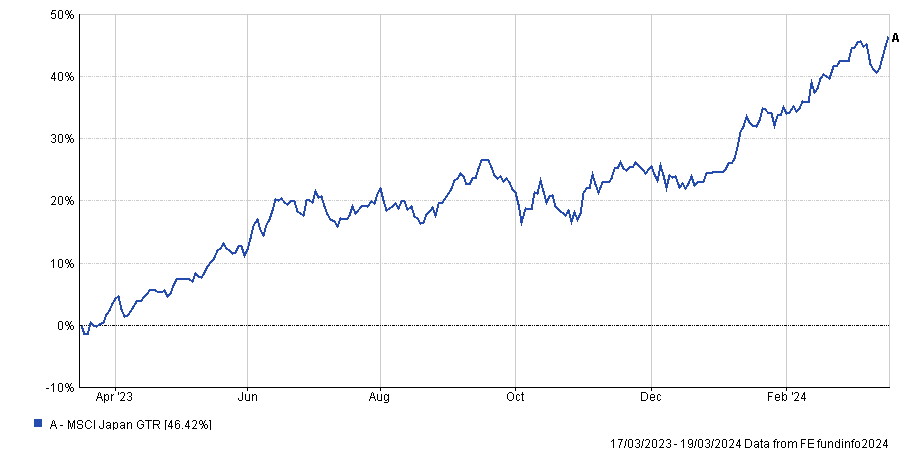

It ushers in a conducive economic backdrop for risk-assets, according to BlackRock’s strategists, who remain overweight Japanese equities even after the year-long rally.

“We see the outlook for equities buoyed by healthy earnings momentum, accelerating shareholder-friendly reforms unfolding across Japan Inc and valuation support from negative real interest rates,” Powell said.

“The sun is not setting on Japanese equities, in our view; it is merely rising on a new horizon.”

Aninda Mitra, head of Asia macro and investment strategy at BNY Mellon Investment Management, also does not see the recent hike as the start of a prolonged hiking cycle, as was the case when other central banks began hiking rates.

In fact, he believes the interest on excess reserve balances will end the year at 0.1%, far lower than 0.27% priced by the swap market.

“The end of explicit and large-scale policy accommodation is also a new regime for equities, but we still believe that the combination of strengthening nominal GDP and corporate reforms (including debt-buybacks and dividend payouts) warrants an overweight allocation in global portfolios,” he said.

Mansoor Mohi-uddin, chief economist at the Bank of Singapore, noted that the BoJ indicated it would have a swift response to any rapid rise in long-term interest rates and that financial conditions will remain accommodative.

“The BoJ’s dovish rate hike thus appears unlikely to stop this year’s strong rally in Japan’s equities,” he said.

Indeed, the BoJ’s decision to gradually normalise its monetary policy is a “positive development”, according to David Chao, global market strategist for Asia Pacific (ex-Japan) at Invesco.

He said: “While Japanese equities have experienced a strong rally in the past year, their valuations are still attractive relative to other major indices.”

A key figure to watch is if inflation in Japan settles at roughly 2% and if wage increases are enough to ensure growth in real wages and therefore consumer spending.

“The recovery in consumer spending is positive for both the Japanese economy and the stock market,” said Fidelity International’s head of Japan investments Miyuki Kashima.