Asia ex Japan equity markets have been underpinned by strong performances by India equities, as well as regional stocks linked to the AI supply chain, notably in Taiwan and Southeast Asia.

However, relative performance to US and global indices had been undermined by the 30% weighting to China in the benchmark Asia ex Japan index. But, a breakout rally in Chinese stocks in September helped Asia ex Japan funds outpace global market indices for the first time in several years.

The surge in Chinese stocks last month in the wake of stimulus measures announced by Beijing boosted the broader region’s equity markets. Generally, however investors remain unconvinced that the official fiscal and monetary policy measures will be sufficient to sustain a long-term rally.

Instead, according to a recent survey of institutional investors by Nomura International, investors appear to be in a “wait-and-watch” mood, awaiting the size and composition China’s fiscal stimulus and the results of the US elections.

Against this backdrop, FSA asked Samuel Lo, associate director, manager research at Morningstar to compare and contrast the abrdn SICAV I – Asia Pacific Sustainable Equity Fund A Acc USD and the Schroder International Selection Fund Asian Opportunities A Accumulation USD.

| abrdn | Schroder | |

| Size | $1.675bn | $5.66bn |

| Inception | 1988 | 2000 |

| Managers | Flavia Cheong and team | Toby Hudson |

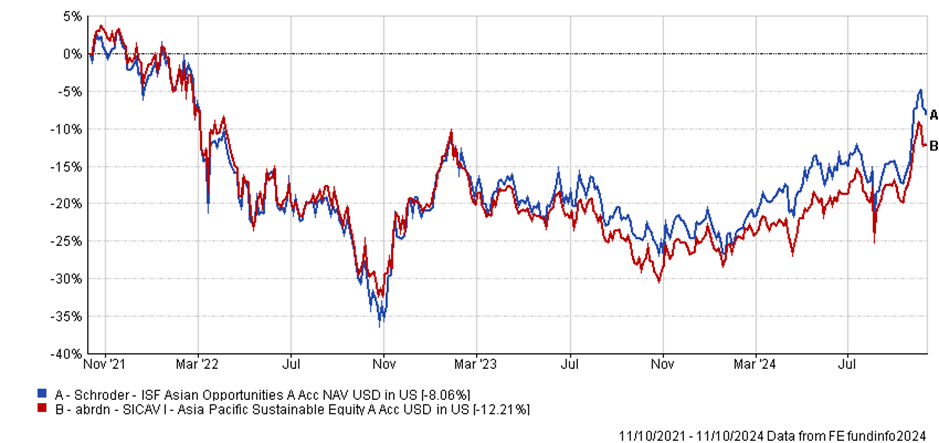

| Three-year cumulative return | -8.06% | -12.21% |

| Three-year annualised return | -4.88% | -3.18% |

| Three-year annualised alpha | -2.45 | -0.35 |

| Three-year annualised volatility | 17.10% | 18.66% |

| Three-year information ratio | -0.65 | -0.20 |

| FE Crown fund rating | ** | *** |

| Morningstar rating | ** | **** |

| Morningstar medal rating | Neutral | Silver |

| OCF (retail share class) | 1.95% | 1.85% |

Investment approach

Both strategies have a bottom-up, quality growth approach, although the abrdn fund has greater tilt towards growth and tends to buy stocks trading on relatively high price-earnings ratios, according to Lo.

The abrdn team uses a well-established research framework to evaluate a company’s quality, which includes factors such as franchise power, management quality, balance-sheet strength, and corporate governance.

“This quality focus has consistently been reflected in the portfolio’s higher return on equity and lower financial leverage compared with the benchmark,” said Lo.

The portfolio holds 50-70 stocks, and annual portfolio turnover averaged about 25% over the past five years, in line with the team’s long investment horizon.

“The abrdn fund managers have adjusted their process since 2019, because stock selections had induced some unintended country risk,” said Lo. The fund was underweight China between 2016 and 2018, so performance suffered. It rectified the imbalance, but of course the timing was wrong, and its performance was hurt again.

Abrdn’s emphasis on consumer and technology growth stocks when value stocks have driven Asian markets has also damaged performance, according to Lo.

“Yet, the shift enables the strategy to better leverage the team’s ample analytical resources and brings greater awareness of country and sector risks to the process,” he added.

The strategy’s quality focus orientates the portfolio toward companies with strong competitive advantages and high return on equity. Favoured sectors include technology stocks, such as Taiwan Semiconductor Manufacturing and Samsung Electronics.

Financials has been another significant sector in the portfolio over the years, especially banks in Southeast Asia and India because they enjoy greater edge in their respective markets and have higher growth potential.

On the other hand, the portfolio has had limited exposure to energy, utilities and real estate over the years, because they generally present few companies that meet the team’s quality requirements.

The Schroder strategy led by Toby Hudson, adopts a disciplined stock-selection framework that seeks to identify quality growth companies.

“The analysts look at the durability of competitive advantages and execution capability when evaluating a company and considers its industry’s barriers to entry and threat of substitution,” said Lo.

Stocks are classified into four categories according to their growth prospects, and the team favours those that can generate higher returns on investment capital than their weighted average cost of capital, or those with ROIC currently below WACC but trending upward.

The Schroder fund typically holds around 45 stocks, with the top 10 holdings comprising 50% of the portfolio.

A formal environmental, social, and governance analysis framework guides the analysts to grade each company on a five-point scale from “Very Weak” to “Very Strong,” with the most weight placed on governance.

“The firm employs a robust, multilayered risk-management framework,” said Lo. A significant enhancement to this system was the adoption of BlackRock’s Aladdin platform in 2017, which effectively integrated various components of the framework.

Hudson has scaled back the portfolio’s exposure to consumer discretionary stocks over the past year, and the July 2024 portfolio’s 13% stake was roughly in line with that of the MSCI Asia ex Japan Index.

The portfolio’s 29% stake in information technology represented a roughly 1% overweighting against the index.

Schroder has more exposure to financial stocks and to Hong Kong-listed companies than abrdn, but Hudson has been more selective on Chinese consumer names, acknowledging the country’s low consumer confidence since post-covid reopening.

Fund characteristics

Sector allocation:

| abrdn* | allocation | Schroder# | allocation |

| IT | 32.1% | IT | 25.7% |

| Financials | 17.8% | Financials | 22.3% |

| Communication services | 12.7% | Consumer discretionary | 15.0% |

| Consumer discretionary | 8.5% | Others | 10.0% |

| Healthcare | 8.1% | Industrials | 8.0% |

| Real estate | 4.6% | Communication services | 7.4% |

| Industrials | 4.5% | Energy | 3.1% |

| Materials | 4.3% | Healthcare | 3.0% |

| Others | 4.8% | Real estate | 2.6% |

| Cash | 2.6% | Materials | 1.5% |

| Consumer staples | 0.9% | ||

| Liquid assets | 0.4% |

Country allocation:

| abrdn* | allocation | Schroder# | allocation |

| India | 20.1% | China | 26.9% |

| China | 19.5% | India | 18.6% |

| Taiwan | 16.0% | Hong Kong | 16.5% |

| South Korea | 11.0% | Taiwan | 15.4% |

| Australia | 9.2% | South Korea | 8.3% |

| Netherlands | 4.8% | Others | 4.9% |

| Hong Kong | 3.9% | Singapore | 2.8% |

| Indonesia | 3.3% | Thailand | 2.6% |

| Others | 9.6% | Indonesia | 2.3% |

| 2.6% | Philippines | 1.3% |

Top 10 holdings:

| abrdn | allocation | Schroder | allocation |

| Taiwan Semiconductor | 9.9% | Taiwan Semiconductor | 9.8% |

| Tencent | 7.4% | Samsung Electronics | 6.7% |

| Samsung Electronics | 7.1% | Tencent | 6.6% |

| AIA | 4.0% | Schroder ISF Indian Opportunities | 5.4% |

| DBS | 3.3% | Schroder ISF Asian Smaller Companies | 4.7% |

| ICICI | 3.1% | ICICI | 3.6% |

| CSL | 2.9% | HDFC | 3.5% |

| ASML | 2.8% | Mediatek | 3.3% |

| SBI Life Insurance | 2.5% | Appollo Hospitals | 3.2% |

| Bank Central Asia | 2.4% | AIA | 3.0% |

Performance

The abrdn fund has generated -12.21% cumulative return during the past three years compared with -8.06% by the Schroder fund, according to FE fundinfo data. Over the same period, the Schroder strategy has a been more volatile, with an annualised standard deviation of 18.66% versus 17.10%.

The Schroder fund is up 16.13% year-to-date, outperforming the abrdn strategy which risen a below-peer average of 14.12%.

“The abrdn strategy’s performance struggles in recent years have dented its long-term track record,” said Lo.

It trailed the Morningstar Asia Pacific ex Japan Target Market Exposure Index and ended in the bottom quartile among peers over the trailing decade ended June 30, 2024. The strategy’s volatility (as measured by standard deviation of returns) has broadly been in line with the index over this period.

Its quality-growth focus has suffered stylistic headwinds in recent years, according to Lo.

“It lagged the index by a significant margin in 2022 and 2023, as the market was mostly driven by value stocks that did not meet the strategy’s quality criteria,” he said. Stock-picking issues in China also compounded the challenges, particularly in 2023.

In the first half of 2024, the strategy continued to lag behind the index and peers. The underperformance was driven by negative stock selection, notably within China and Hong Kong, according to Lo.

“The abrdn strategy’s performance struggles in recent years have dented its long-term track record,” said Lo.

It trailed the Morningstar Asia Pacific ex Japan Target Market Exposure Index and ended in the bottom quartile among peers over the trailing decade ended June 30, 2024. The strategy’s volatility (as measured by standard deviation of returns) has broadly been in line with the index over this period.

Its quality-growth focus has suffered stylistic headwinds in recent years.

“It lagged the index by a significant margin in 2022 and 2023, as the market was mostly driven by value stocks that did not meet the strategy’s quality criteria,” he said. Stock-picking issues in China also compounded the challenges, particularly in 2023.

In the first half of 2024, the strategy continued to lag behind the index and peers. The underperformance was driven by negative stock selection, notably within China and Hong Kong, according to Lo.

In contrast, “the Schroder strategy has delivered stellar results for investors over the years,” said Lo.

Despite “middling” near-term results, its 10-year performance as of end August 2024 comfortably beat both the Morningstar Asia ex Japan Target Market Exposure Index Morningstar Category benchmark and median peer.

The manager’s quality focus has helped the strategy to better weather bear markets such as 2015, 2018, and 2022.

Results have been relatively consistent, with 2013 the only calendar year that the share class lagged both indexes and its median peer, and Hudson has continued to deliver over his tenure as lead manager, according to Lo.

Nevertheless, the strategy has struggled during the past year ending July 2024. The recent market rally was mainly driven by artificial intelligence-related technology names, as well as energy and utilities stocks, the latter of which Hudson has historically been light on given their limited growth prospects.

Discrete calendar year performance

| Fund | YTD* | 2023 | 2022 | 2021 | 2020 | 2019 |

| abrdn | 14.12% | -3.91% | -19.29% | -4.12% | 28.63% | 18.67% |

| Schroder | 16.13% | 0.72% | -19.86% | -4.40% | 26.27% | 22.79% |

| Sector | 14.46% | 3.63% | -19.04% | 0.11% | 21.83% | 18.21% |

Manager review

The abrdn strategy is collegially managed by a portfolio construction “pod” that consists of pod leader Pruksa Iamthongthong, head of equities Asia Pacific Flavia Cheong, James Thom, and Jerry Goh. While the pod has historically been stable, it recently saw the departure of Christina Woon, who left in January 2024 and has yet to be replaced.

The strategy is supported by an Asia Pacific ex Japan equities team of around 30 members. But abrdn has been afflicted with high staff turnover, not only among Asia equities but the departures of several veterans throughout the firm, including 17 out of 30 product specialists.

“There has been lots of disruption which challenges the rigour of investment processes and inevitably dents morale,” he added.

“While the team replaced the other departures and its large size provides some buffer, we would like to see more stability within the team,’ said Lo.

In fact, one the most significant difference between the Schroders and abrdn funds is the stability of their respective investment teams.

Lead manager Toby Hudson is a Schroder veteran who has dedicated his entire investment career to the firm since he joined in 1992. He officially took the helm of this strategy on 1 January 2018 after having been involved for over a decade.

“He is an expert investor, having led all his Asian equity strategies to great success. His in-depth investment knowledge, thoughtful portfolio construction, and great passion for investing underpins our confidence,” said Lo.

Hudson gets close support from Wei Wei Chua, who joined the team in April 2021 as a regional portfolio manager, and he is backed 36 Asia ex Japan analysts. The research team is experienced and has been relatively stable since 2021, with annual departures in the low single digits.

The teamwide, quality growth-focused investment process is structured, and it benefits from a clearly defined stock-selection framework, where analysts assess a company’s growth prospects by comparing its return on invested capital and weighted average cost of capital.

“Hudson has been consistent with his application, with an emphasis on management quality and corporate governance,” said Lo.

Morningstar consider Hudson “is a best-of-breed Asian equity manager”.

Fees

The ongoing charges figure for the Schroder fund is 1.85% and is 1.95% for the abrdn fund.

Lo says both fees are “satisfactory”.

But he believes that the share class of the Schroder fund will be able to deliver positive alpha relative to the category benchmark index, explaining its Morningstar Medalist Rating of Silver.

On the other hand, he doesn’t think the share class of the abrdn fund will be able to deliver positive alpha relative to the category benchmark index, hence the Morningstar Medalist Rating of Neutral.

Conclusion

The abrdn strategy’s quality-focused investment approach is time-tested and continues to be a strength, although concerns around the investment team’s stability have weighed on Morningstar’s conviction.

“The strategy had seen better days in the past, indicating the process’ potential to add value, but its performance struggles in recent years have dented its long-term track record,” said Lo.

Despite the disruption caused by people leaving, which has led to downgrades of other abrdn funds too, Lo retains his faith in the abrdn investment process. However, it cannot be immune from that disruption.

But, ultimately, “the abrdn fund doesn’t bring anything to the table that the Schroder fund already does better,” said Lo.

“The Schroder fund is superior and must be the first choice between two strategies with similar growth-oriented styles.”