The transformation in societies, economies and technologies over the last 18 months has heralded an important turning point for companies and investors alike.

This has put a spotlight on sustainability. The rise of the “conscious consumer”, for example, is increasingly holding corporations and governments to account through buying behaviour, election choices and shareholder activism. At the same time, regulators are implementing new directives across borders to address environmental, social and governance (ESG) issues.

In turn, these trends have created a new wave of high-quality opportunities as investors strive to make an impact with their capital.

To tap into these amid the disruption and long-term transitions reshaping various sectors, investors need to look beyond traditional industry boundaries to identify future winners in today’s value chains. Yet, this doesn’t require portfolios to compromise investment performance for the sake of good citizenship.

In short, contrary to what some investors might think, companies that capitalise on change and make sustainability central to their business models can also offer compelling investment opportunities and attractive risk-adjusted returns.

Three features of tomorrow’s winners

The common denominators are three-fold: they have a durable competitive position in their markets; their goods or services do little, if any, harm to the environment or society; and they can adapt quickly and effectively to change.

Looking for companies that…

Durable Competitive Position: Having a good business model doesn’t justify a durable competitive position, since another company might be able to replicate the product or service – possibly better or at a lower price. In fact, two key indicators of durability are cash flow return on investment (CFROI) and asset growth. Companies with high CFROI and structural asset growth are highly profitable and able to compound those profits by reinvesting internally generated cash flows into their core business and attractive opportunities.

Do Little to No Harm: Further, many companies overlook their social or environmental responsibilities, fail to build on the potential for positive impact, or simply don’t respect investors’ preferences. This mindset will often manifest itself in the form of lost customers, reputational scandals, or civil or regulatory penalties. By contrast, good ESG practices can be aligned with a company’s broader financial performance when they are materially relevant to the specific business and its future strategy.

Adapt to Change: Adaptability is also not automatic within companies. Those firms at the forefront of their sectors must also be able to pivot with shifts in regulations, social attitudes and consumer preferences. In an age of disruption, offering solutions to emerging themes suggests a company can lead change in these value chains.

| Case study: a closer look at what makes a transition winner In the early 1990s, Microsoft was a ‘transition winner’ in the personal computing revolution, building a durable competitive position in PC-based operating systems and software. By the mid-2000s, however, that position was beginning to be disrupted by the commercialisation of cloud computing by the likes of Amazon, Google, IBM and Salesforce. In response, Microsoft had the managerial flexibility and cash flow to adapt to change with new investments in cloud-enabled productivity solutions. Moreover, Microsoft differentiates itself in this value chain with a clear objective to help its customers do little-to-no-harm environmentally. It believes cloud computing can make businesses up to 93% more energy efficient, and in 2020 showed it was possible to power its Azure cloud infrastructure with zero-carbon hydrogen fuel cells. Today, Azure is one of the three largest cloud service providers worldwide, alongside Amazon Web Services and Google Cloud Platform, and one of the fastest-growing, especially in enterprise Software as a Service (SaaS). References to any securities in the document are for illustrative purposes only and do not constitute a recommendation to investors |

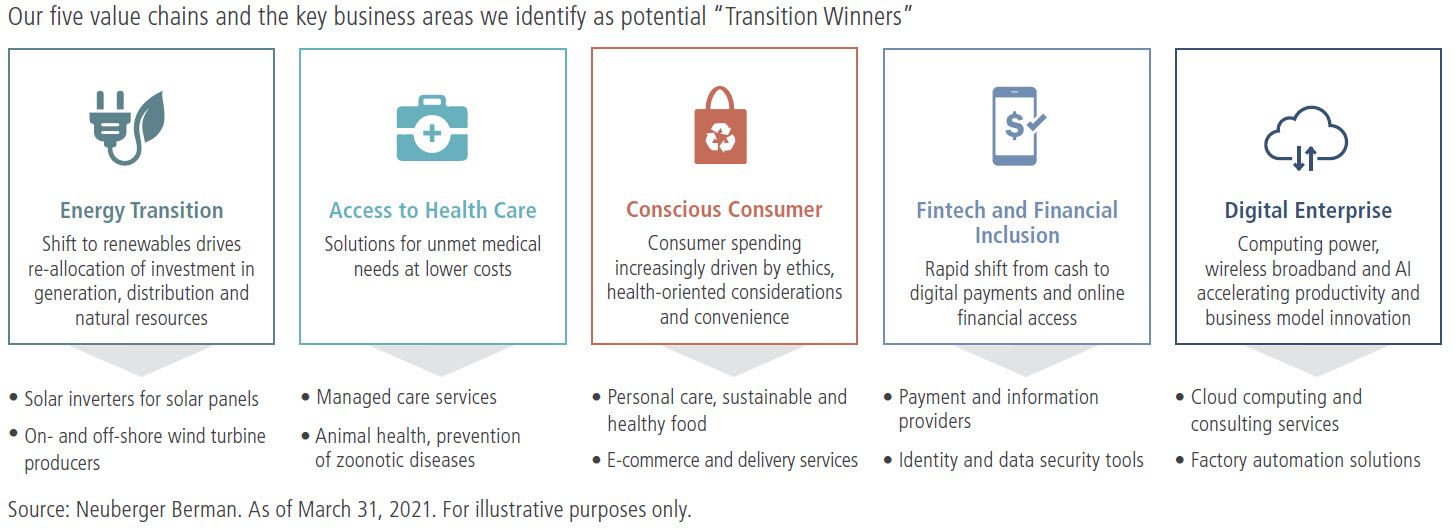

Value chain lens looks beyond traditional sector

With these features of durability, sustainability and adaptability in mind, certain value chains offer a more realistic view of what’s going on in today’s economy – and, therefore, create greater potential for alpha.

These are represented by five themes: the demand for renewable energy; access to healthcare through lower-cost solutions for unmet or high-cost medical needs; conscious consumption in line with the ever-sharper focus on ethics; fintech solutions to facilitate the shift to digital payments and online access to finance; and digital enterprise amid advances in computing power, 5G and artificial intelligence accelerating productivity and business innovation.

From traditional industries to a broader value-chain lens

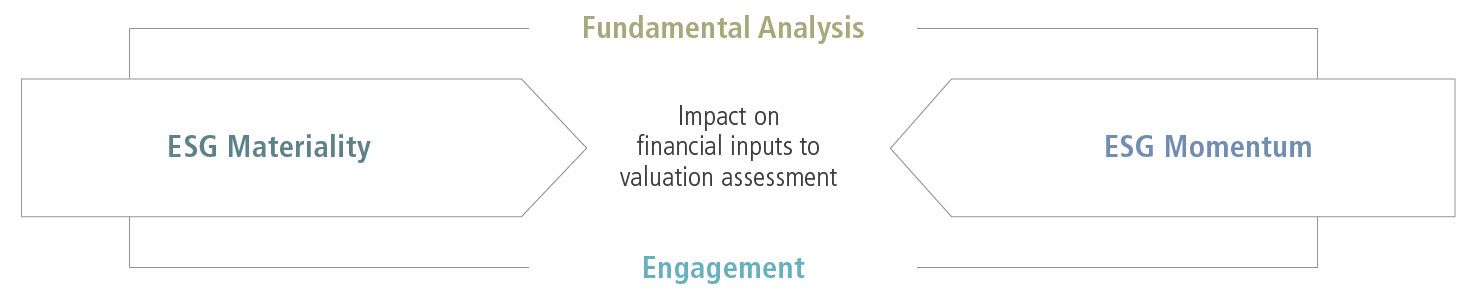

Identifying transition winners demands more than a top-down allocation based on a sector or style-based approach. This is a less important driver of excess return than in the past. Instead, the key to unlocking alpha are fundamental insights gleaned from analysis of the value chain via bottom-up research and company engagement.

ESG integration drives alpha

A lot of ESG investing remains top-down and quantitative. These screens are useful for weeding out the very riskiest businesses, but, in our view, they are much less useful for differentiating between businesses that pose similar levels of risk or identifying attractive opportunities. There are two reasons for that: top-down screens do not differentiate the true materiality of certain factors to specific companies; and they are backward-looking.

Furthermore, the historical data that feeds into quantitative ESG scores does not fit well with our focus, as active investors, on businesses that are making marginal ESG improvements that are yet to be priced into securities. They offer no insight into a company’s sustainability action plans. Most of all, they say nothing about opportunities to help companies improve their ESG performance through active shareholder engagement.

For us, low current ESG risk is a plus, but we see the most attractive alpha opportunities in active efforts both to manage and to change ESG exposures.

In summary, when ESG-related factors are materially relevant to a specific business, and we ask forward-looking questions rather than looking only at historical data, we believe that good performance and planning around those factors can have a direct relationship with a company’s broader financial performance.

At a Glance – Neuberger Berman Global Sustainable Equity Fund

- Seeks to invest in quality companies where sustainability reinforces competitive advantage

- Global, best ideas portfolio of typically 40 – 60 quality holdings

- Diversified across non-correlated high-quality business models and value chains

- Long-term bottom-up research outlook (typical two to four years holding period)

- Active share >75%

- Sustainability, value chain lens and engagement key to approach

- The fund classified as an E.U. Article 9 SFDR fund

- The fund returned 24.8% (net) since inception on 24 February 2021, outperforming its benchmark MSCI World Index (Total Return, Net of Tax, USD) by 1031 basis points (Source: Neuberger Berman, as of end October 2021. Fund performance is representative of the Neuberger Berman Global Sustainable Equity Fund USD I Accumulating Class.)

To learn more about Neuberger Berman Global Sustainable Equity Strategy:

For Hong Kong audience, please click here.

For Singapore audience, please click here.

Why Neuberger Berman?

- Dedicated team of seven experienced, industry-leading professionals; lead-PM has 30+ years of investment experience, over half of which has been on this strategy. Strategy ranked seventh percentile among peers over five years1

- Supported by 45-person global equity research department, including 38 senior research analysts averaging 18 years of experience, and a dedicated nine-person ESG investing team

- ESG leadership – Neuberger Berman is awarded A+ scores by UN-supported PRI and a member of PRI 2020 Leaders’ Group, a designation awarded to fewer than 1% of PRI investment manager signatories

1 Source: eVestment as of September 30, 2020. The portfolio managers were the lead decision makers of this strategy at their previous firm, NN Investment Partners, until September 27, 2020. Peer statistics are reflective of performance against the respective vehicle peer group (Global Large Cap Core).

This material is intended as a broad overview of the portfolio managers’ current style, philosophy and process and is subject to change without notice. Portfolio managers’ views may differ from those of other portfolio managers as well as the views of Neuberger Berman. Investing entails risks, including possible loss of principal. Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss.

Neuberger Berman Investment Funds plc (the “Fund”) is authorised by the Central Bank of Ireland (the “Central Bank”) as an Undertaking for Collective Investment in Transferable Securities under the European Communities (“UCITS”) Regulations 2011 (S.I. 352 of 2011) of Ireland, as amended. Neuberger Berman Asset Management Ireland Limited may decide to terminate the arrangements made for the marketing of its funds in all or a particular country. The Fund mentioned in this document may not be eligible for sale in some countries and it may not be suitable for all types of investor. Shares in the fund may not be offered or sold directly or indirectly into the United States or to U.S. Persons; for further information see the current prospectus.

We do not represent that this information, including any third party information, is accurate or complete and it should not be relied upon as such. Opinions expressed herein reflect the opinion of Neuberger Berman Group and its affiliates (“Neuberger Berman”) and are subject to change without notice.

This document is for information purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy the securities or other instruments mentioned herein. No part of this document may be reproduced in any manner without the written permission of Neuberger Berman.

Past performance is not indicative of future results. The value of investments may go down as well as up and investors may not get back any of the amount invested. The performance data does not take account of the commissions and costs incurred by investors when subscribing for or redeeming shares. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. Investors may not get back the full amount invested. For further details of the investment risks, please refer to the current prospectus. Please note that any dividends/interest which the Fund may receive may be subject to withholding tax. The benchmark does not take into account the effects of tax and the deduction is therefore not reflected in the benchmark return illustrated herein. The investment objective and performance benchmark is a target only and not a guarantee of the Fund performance. The index is unmanaged and cannot be invested in directly. Index returns assume reinvestment of dividends and capital gains and unlike fund returns do not reflect fees or expenses. Adverse movements in currency exchange rates can result in a decrease in return and a loss of capital. Investments of each portfolio may be fully hedged into its base currency potentially reducing currency risks but may expose the portfolio to other risks such as a default of a counterparty.

This document has been issued for use by the following Neuberger Berman entities: in Hong Kong by Neuberger Berman Asia Limited [“NBAL”], which is licensed and regulated by the Hong Kong Securities and Futures Commission to carry on Types 1, 4 and 9 regulated activities, as defined under the Securities and Futures Ordinance of Hong Kong (Cap.571) (the “SFO”); in Singapore by Neuberger Berman Singapore Pte. Limited (NBS), which currently carries out the regulated activity of fund management under the Securities and Futures Act (Chapter 289) (“SFA”) and operates as an Exempt Financial Adviser under section 23(1)(d) of the Financial Advisers Act (Chapter 110) (“FAA”) of Singapore. Under the FAA, NBS is exempted from Sections 25, 27 and 36 of the FAA, where its financial advisory service is provided to an accredited or expert investor (as defined in Section 4A of the SFA).

This document is being provided by NBAL and NBS on a confidential basis to an “accredited investor”, “institutional investor”, “professional investor”, “QPI”, “sophisticated investor”, “wholesale investor” and/or other such qualified person, in each case as defined under the laws of the relevant jurisdiction listed below, and all of which together are generically referred to as a “Sophisticated Investor”, on a “one-on-one” basis for informational and discussion purposes only. This document is intended only for the Sophisticated Investor to which it has been provided, is strictly confidential and may not be reproduced or redistributed in whole or in part nor may its contents be disclosed to any other person (other than such Sophisticated Investor’s agents or advisers) under any circumstances.

Important information for Sophisticated Investors in:

Hong Kong: The contents of this document have not been reviewed by any regulatory authority in Hong Kong. Please note that (i) Securities may not be offered or sold in Hong Kong by means of this document or any other document other than to “professional investors” as defined in Part I of Schedule 1 to the SFO.

Singapore: Any offer or invitation which is the subject of this document is only allowed to certain persons and institutions and not to the retail public. Moreover, this document or any written materials issued in connection with the offer is not a prospectus as defined in the Securities and Futures Act, Chapter 289 of Singapore (the “SFA”). Accordingly, statutory liability under the SFA in relation to the contents of prospectuses would not apply. The Offeree to whom this document is provided should consider carefully whether the investment, if any, is suitable for it.

This document and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of any Security may not be circulated or distributed, nor may any Security be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore other than (i) “institutional investors” pursuant to Section 304 of the Act, (ii) “relevant persons” pursuant to section 305(1) of the Act, (iii) any person pursuant to Section 305(2) of the Act, or (iv) otherwise pursuant to, and in accordance with the conditions of, other applicable provisions of the Act.

The Portfolios are restricted schemes under the Sixth Schedule to the Securities and Futures (Offers of Investments) (Collective Investment Schemes) Regulations. The offer, holding and subsequent transfer of Shares are subject to restrictions and conditions under the Act.

You should consider carefully whether you are permitted (under the Act and any laws or regulations applicable to you) to make an investment in the Shares and whether any such investment is suitable for you and you should consult your legal or professional advisor if in doubt.

Neuberger Berman is a registered trademark.

© 2021 Neuberger Berman