David Eiswert, T Rowe Price

T Rowe Price agrees with the Federal Reserve Board that “absurd” inflation is transitory, as demographics and technology will remain powerful structural forces that can continue to put downward pressure on long-term inflation trends. These forces have not disappeared and should return as economies normalize.

Absurd – that is, extraordinarily high – inflation is expected to fade, and economic growth is set to stabilise. Lower inflation will be seen as more workers return to jobs and tight supply conditions ease. This has the potential to evolve into a good environment for stock pickers, but one that is bad for crowded growth trades and pure speculators, according to David Eiswert, portfolio manager of T Rowe Price’s Global Focused Growth Equity Strategy.

“We are searching for solid growth assets that are out of favour currently, but where we see potentially higher growth in 2022 and beyond,” Eistert told FSA.

“These include some travel‑related names. We also believe it is worth exploring China’s regulatory changes and the opportunities that it may create—albeit with prudence,” he added.

During times of market transition, Eiswert prefers companies that are able to improve or accelerate returns in the future, while trying not to pay too high a price.

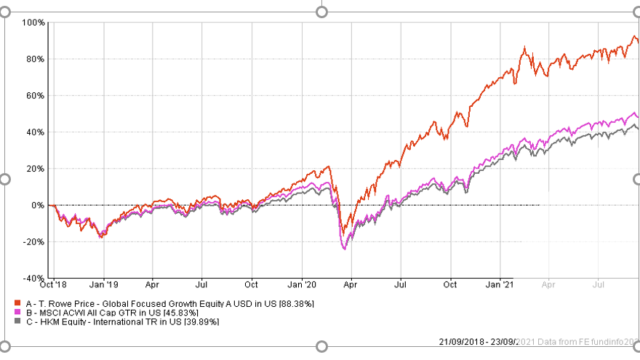

The $5.56bn Global Focused Growth Equity Fund has posted a 88.38% three-year cumulative return in US dollar terms, outperforming its MSCI ACWI All Cap Index benchmark (45.83%) and the sector average (39.89%).

Its top five holdings are Facebook, London Stock Exchange, Unitedhealth Group, Schwab (Charles), Alphabet, according to its 30 June 2021 factsheet.

Geographically, the fund’s top five allocations are to the US (56.8%), UK(9.6%), Japan(6.6%), China(4%) and India(3.5%).Its main sector exposure is to information technology, consumer discretionary, financials, industrials & business services, and communication services.

Identifying the winners

In the current market environment, the fund is careful not to overly skew the portfolio in any one direction, according to Eiswert. Ultimately, it tilts towards companies with “idiosyncratic drivers that are on the right side of change”.

Now is the time to distinguish between the “chasm crossers”—those companies that will succeed and thrive—and the “imposters”—those companies that have experienced temporary benefits that will likely not prove durable, Eiswert said.

This approach often requires the ability to distinguish good companies from good stocks. “Experience has shown that making difficult decisions by adhering to the fund’s investment framework with the support of its global research platform ultimately can add value for clients,” he said.

However, Eiswert warns about “careless risk‑taking” in financial markets. A rapid increase in interest rates that causes a crisis, and leads to a flattening, or even an inverted yield curve would mean that the price of virtually all assets would fall, he said.

T Rowe Price Global Focused Growth Equity Strategy fund vs benchmark and sector average