For much of the past year, efforts by biopharma companies to rein in Covid-19 have dominated healthcare sector news. The industry’s response – developing vaccines and treatments for the novel coronavirus in less than a year – is one for the record books.

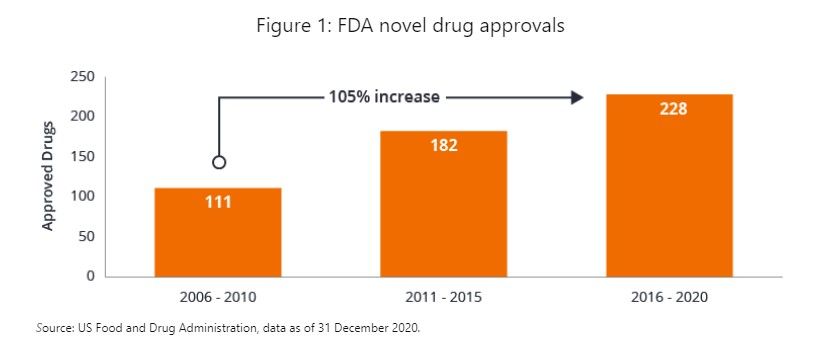

But as the end of the pandemic comes into sight, we believe healthcare’s achievements are only getting started. Last year, the US Food and Drug Administration (FDA) approved 52 novel drugs, excluding medicines for Covid-19. That sum is not far from the 2018 record of 59 and occurred despite lockdown measures that closed labs and slowed drug-manufacturing site inspections1.

Looking ahead, we believe this momentum – rooted in accelerating innovation and supported by financial markets – could fuel growth in the sector for years to come.

Healthcare innovation ramps up

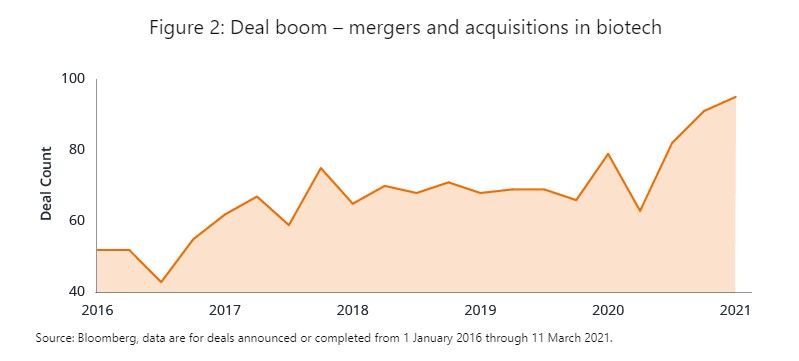

In 2020, ultra-low interest rates and Covid-related research helped see $51bn in venture capital invested in healthcare.2 In biotech specifically, 84 firms made initial public offerings (IPOs), an increase of 65% from 2019. These companies raised more than $15bn – about three times as much as the prior year – and saw their stocks climb by an average of 89% year to date.3 IPOs have continued at a swift pace so far in 2021, and the funding boom is expected to spur further innovation. Even large-cap pharmaceutical companies have been ramping up their investments in novel therapeutics. Flush with cash but facing patent expirations, big pharma has been rapidly buying innovation through the acquisition of small- and mid-size biotechs, as highlighted in Figure 2.

Research also shows that R&D productivity within the pharmaceutical industry has been improving. During preclinical research, companies now increasingly validate drug targets genetically and use biomarkers to identify appropriate patient pools, both of which have helped to reduce attrition rates in later-stage studies.

Advances and breakthroughs

Advances are being made across a multitude of disease categories, with cancer screening among the most exciting. Early detection of cancer can drastically improve survival rates for patients. Blood-based tests in clinical trials aim to look for fragments of DNA and RNA released by tumours into the bloodstream, even before cancer symptoms are present. Preliminary data have been promising – so much so that two multibillion-dollar acquisitions of companies at the forefront of this science were announced in 2020.

Innovation leads to sales growth

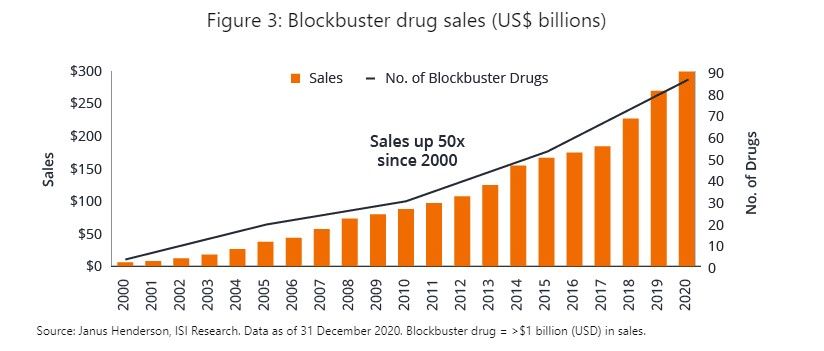

The surge in medical innovation is having a commensurate impact on biopharma revenues. Last year, sales of biotech blockbuster drugs neared $300bn, about 50 times the amount from two decades ago as shown in Figure 3. Rising global demand for healthcare is helping drive the growth. At the same time, more drugs are now targeting patients with high, unmet medical needs.

Other launches have experienced Covid-related disruptions, which could set these products up for a recovery in 2021.

The next chapter: the internet of healthcare

Innovation is taking place throughout the healthcare sector. In medical devices, we are witnessing an unprecedented convergence of scientific and technological advances that could have life-changing potential for patients. In late 2019, pharmaceutical giant Eli Lilly announced it was partnering with Dexcom, a maker of continuous glucose monitors (CGMs)- small sensors worn by diabetics that continuously measure blood sugar levels. Connected to an insulin pump, the CGM can automatically deliver insulin to patients when needed (no finger stick tests required). It also sends data to a wireless device, such as a smartphone.

We expect this type of “connected” healthcare to gain momentum. As healthcare providers increasingly understand the potential long-term benefits of such technologies, we believe reimbursement rates will improve and usage could soar.

Balancing risk with opportunity

Enthusiasm for the rollout of Covid-19 vaccines and medical breakthroughs have sent stocks of some healthcare companies soaring, particularly those of preclinical or early-phase small-cap biotech firms. We believe caution is warranted in many cases where the science is still unproven and revenues are nonexistent. Industry research shows that 90% of drug candidates fail to move beyond clinical trials. In our experience, Wall Street analysts also tend to under- or over-estimate a new drug’s commercial potential 90% of the time. With that in mind, we believe investors need to be selective, balancing valuation with downside risks.

However, we also see a burgeoning opportunity set. Relative to the broad equity market, the healthcare sector trades at a discount, with a forward price-to-earnings (P/E) ratio of 16.3 compared with 22.9 for the S&P 500® Index5. Stocks of profitable biotech companies are even cheaper, with an average forward P/E of 11.1.6 In 2020, 100 companies were added to the Nasdaq Biotechnology Index, which requires firms to have a minimum market capitalisation of $200m. In short, the industry is expanding rapidly and, in our view, could still have significant room to grow in the months and years ahead.

Disruption and innovation are accelerating. Let Janus Henderson help you harness the power of change and stay on the right side of disruption. Find out more for Hong Kong and Singapore.

1US Food and Drug Administration, data as of 31 December 2020.

2“Health Care Investments and Exits,” Annual Report 2021, Silicon Valley Bank.

3Jefferies, as of 5 January 2021.

4“The Biotech IPO Boom,” BDO Biotech Brief Winter 2021, February 2021.

5Bloomberg, data are based on forward, 12-month estimated earnings for the S&P 500 Health Care sector and the S&P 500 Index as of 15 March 2021. The S&P 500 Health Care sector comprises those companies included in the S&P 500 that are classified as members of the GICS® health care sector.

6Bloomberg, data are for GICS-classified biotechnology stocks as of 15 March 2021.

Important information

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organisation. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. In preparing this document, Janus Henderson Investors has reasonable belief to rely upon the accuracy and completeness of all information available from public sources. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency.

Issued in (a) Singapore by Janus Henderson Investors (Singapore) Limited (Co. registration no. 199700782N) licensed and regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. (b) Hong Kong by Janus Henderson Investors Hong Kong Limited, licensed and regulated by the Securities and Futures Commission. This document has not been reviewed by the Securities and Futures Commission of Hong Kong. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

The value of an investment and the income from it can fall as well as rise and investors may not get back the amount originally invested. There is no assurance stated objective(s) will be met. There is no assurance that the investment process discussed includes an effort to monitor and manage risk which should not be confused with and does not imply low risk or the ability to control certain risk factors. Various account minimums or other eligibility qualifications apply depending on the investment strategy, vehicle of investor jurisdiction.

Investors are advised to consult your intermediary who will give you advice on the product suitability and help you determine how your investment would be consistent with your own investment objectives. The investment decisions are yours and an investment in the Fund may not be suitable for everyone. If in doubt, please contact your intermediary for clarification.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Janus Henderson is a trademark of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.