Winnie Chwang, Matthews Asia

Matthews Asia expects positive corporate earnings growth in China this year, rising to 18% in 2021 and 16% in the 2022. However, these forecasts are for the MSCI China index made up of Hong Kong- and US-listed companies.

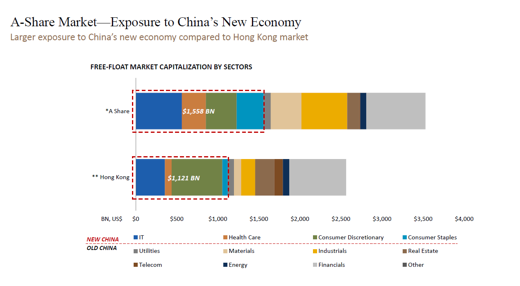

The A-share market of Shanghai- and Shenzhen-listed companies is much larger, and includes many small-cap firms that could deliver even higher earnings, according to Winnie Chwang, portfolio manager at Matthews Asia.

It also comprises many under-researched technology firms that drive the so-called “new economy”.

“China today is very different to how it was two decades ago, and the change is evident in the proliferation of small- and mid-sized companies, as well as clearly recognisable long-term trends,” said Chwang.

Chwang is a lead manager of the $317m Matthews China Small Companies Fund, which has generated a three-year cumulative return of 85.46% in US dollar terms, compared with only 9.35% by its benchmark MSCI China Small Cap index, according to FE Fundinfo.

She is also deputy-manager of the $114m Matthews China Fund, which is up 47.2% over the same period, compared with 29.58% by its benchmark MSCI China index, FE Fundinfo data shows.

Chwang identifies four major secular investment opportunities that are a consequence of urbanisation and an upgrade in consumer preferences.

First, “property management is becoming increasingly popular as personal and household wealth rises, and companies that provide this service deliver highly visible earnings and cashflow,” she said.

Second, people are buying more luxury cars; third, tourism will grow rapidly from quite a low base with only 10% of Chinese people possessing passports; and finally, “demand for education is inelastic” and both offline and online educational services is a growing segment of the economy.

Chwang also expects productivity upgrades in many sectors, powered by advances in technology and automation, and complemented by a growing talent pool of higher quality graduates entering the workforce.

EXTERNAL SENTIMENT

Robert Horrocks, CIO of Matthews Asia, has emphasised broader factors that will likely contribute to a good performance by Asian equities next year.

“US asset allocators are looking more positively towards Asia, including China. The region’s economic recovery is on track and is sustainable, and the election of Biden as US president might thaw geopolitical tensions,” he said.

“In addition, the US dollar is likely to be under pressure next year as domestic wages rise, which will encourage global investors to allocate to Asia, and although price-earnings ratios are historically quite high in the region, they remain attractive compared with US multiples,” he said.

However, although so much focus is on the opportunities in China, Horrocks has a different regional favourite: Vietnam.

“Everything is going for it: geography, young demographics, infrastructure improvements, access to external financing, rapid innovation and an entrepreneurial, hard-working population,” said Horrocks.

“Vietnam is like Guangdong in the mid-1980s,” he said.

“But, you really need to know the country well in order to identify the best stock selection opportunities, which are mostly small- and mid-caps,” he warned.