Although the initial fund selection process is important at Union Bancaire Privée (UBP), how those funds are then monitored after onboarding is just as important, if not more.

That is the view of Yan Ting (YT) Kum, UBP’s head of funds, North Asia, who likens fund selection to marriage.

“Some people view marriage as a one-time event, but in reality, once you’re married, you have to keep working on the relationship to keep it strong and happy,” he told FSA in an exclusive interview.

After initially selecting a fund, he believes the fund monitoring process is critical in ensuring the UBP’s fund product shelf remains robust.

“As a fund selector, my main focus is ensuring we have a strong mix of high-quality funds to build well-diversified portfolios for our clients,” he said.

To ensure that the ‘marriage’ is going smoothly, Hong Kong-based YT Kum (pictured) has regular meetings with the bank’s global committee to monitor fund performance.

If a fund has been underperforming for three to six months, they will get their correspondent analysts to explain what’s going on, and if necessary, engage with the fund manager.

This is where he emphasised that having a good relationship with the fund manager is important, so that they can have frank conversations about their portfolios, their thinking, and what their plans are.

But no matter how much work is put into the relationship, like marriages, not all funds selected for the shelf are destined to last.

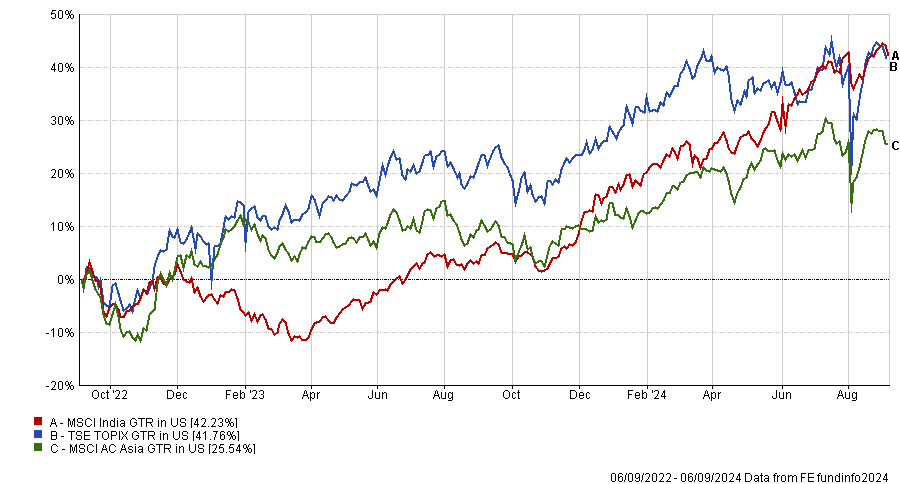

Swiss-headquartered UBP has recently reshuffled some of its Japanese equity funds on its platform amidst a sustained rally from the once shunned equity market.

It has also made some change to its fund managers in the Indian equity space earlier in the year.

Japan and India have been standout performers within Asian equity markets over the past two years, but some funds have delivered better alpha than others.

In US dollar terms, the TSE TOPIX is up 41.8% over the past two years, and the MSCI India index is up 42.2% over the same period, compared with 25.5% from the broader MSCI Asia index.

Equity market regime changes

YT Kum is also focused on regime changes in financial markets and their implications for fund selection.

He highlighted the Chinese equity market as an example where such changes influence the fund selection and monitoring process.

The equity market has been in a sustained downturn for the past several years, made worse by the country’s real estate woes.

“Many China equity portfolio managers are finding it challenging to outperform their benchmarks,” YT Kum said. “The market landscape has shifted, and it looks very different from what it was before the real estate downturn.”

But it’s not just real estate that has gone through difficulties in recent years, electric vehicles, gaming, technology all have endured major changes – altering the winning playbook for investors.

As such, when thinking about the fund selection process, YT Kum is looking for fund managers that are adapting with new approaches to investing in China.

He said: “We ask fund managers how they are responding to these changes, and whether they plan to adjust their investment approaches for the future.”

“Our research is important because the old methods of delivering alpha may no longer apply in the future.”

A fixed income regime change

On the fixed income side, one area of focus that has come up more recently is how bond managers are managing their duration risk.

This is particularly important as most bond managers were caught off guard in 2022 when central banks increased interest rates and battered bond portfolios.

“Duration management has become an increasingly difficult part of a fund manager’s job,” YT Kum said. “One reason is that they’ve become somewhat accustomed to the low-rate environment.”

He said some bond managers previously didn’t have to think twice about what the Fed was going to do during their next policy meeting – rates were largely unchanged for a decade.

“As a result, many portfolio managers have been focusing on credit selection, and duration was not really an area where they could add much value,” he said.

Now, he laments that quite a number of fixed income managers have been wrong most of the time in predicting the actions of the Fed, and unable to effectively manage the duration of their portfolios.

“Over the past two years, global fixed income managers have worked hard to add value through duration management,” he said. “But the investment landscape has clearly shifted, and they are now finding ways to generate alpha in this new environment. For example, some have become more active in less mainstream asset classes such as CLOs and corporate hybrids.”

Bond fund managers he meets now face some tough questions, particularly around whether they have a new investment framework, or new insights into how they plan to navigate the new interest rate market.

Looking beyond the shortlist

Like most fund selection teams at the major banks and wealth management firms, UBP has a quantitative screen to generate a shortlist of funds. But these are often backward looking and can exclude some high quality products.

This is why, in addition to the candidates shortlisted by the quantitative screen, YT Kum may also consider fund candidates that were excluded from the initial screen.

“We use a quantitative screen for shortlisting, but it is far from mechanical,” he said. “Numbers are important and help to build solid investment case. However, if a fund was excluded due to one year of underperformance but has since improved, we might reconsider it for further discussion.”

“Of course, this doesn’t mean we will necessarily onboard the fund, but we prefer not to exclude a fund just because of one year underperformance.”

After that, the fund selection team delves into the investment process and ensures that the performance isn’t driven by luck.

This is where performance attribution analysis is his preferred method for assessing the “personality” of a strategy.

“Many people focus on the qualitative descriptions of an investment process, which are important. However, especially with funds that have a track record, I look closely at their attribution analysis to see where the alpha has come from in the past,” he said.

“Attribution analysis provides valuable insights into the personalities of a portfolio manager or an investment team. This is where I invest much of my time.”