The environment needs more help than investors are currently providing. From ecosystem degradation to the climate emergency, mounting evidence shows the world has reached a tipping point in terms of global warming, losses of species and changes in rainfall distribution, among many other issues.

Yet despite efforts to channel investments to companies that can seemingly make a meaningful positive green impact, more often than not, it isn’t possible to assess the real contribution of this capital.

As a result, generating strong long-term returns through investing in this popular theme is no longer enough. More measured steps are needed.

The starting point is to redefine and quantify “impact”. This requires investors to be aware of the actual financial contribution that gets made to the green transition and to efforts to protect against ecosystem destruction.

A simple but effective way to achieve this is via a revenue sharing arrangement with environmental charities that help to tackle the twin problems of climate change and biodiversity loss.

“By giving one-third of all our management fees from the TT Environmental Solutions strategy to carefully selected environmental charities, we aim to solve the issue of how to effectively and measurably create impact,” said Harry Thomas, the strategy’s co-portfolio manager.

If adopted by the wider industry, the approach would result in tens of millions more dollars becoming available to relevant charities to help fund projects that otherwise may simply not happen. At a minimum, Thomas added, certain projects would be accelerated.

“It is our sincere hope that other investment managers will follow suit, with this ultimately becoming the standard approach for environmental funds and impact investing more broadly,” he explained.

Direct and deliberate

Rather than just lowering fees so investors can make donations with their spare cash, fostering holistic and meaningful relationships between charities and investment managers leads to greater commitment to a longer-term partnership.

This approach reflects the importance of the role that the financial sector plays in supporting the green transition. For example, expertise can be shared in the form of advice that might help improve the capital structure and financial framework of a particular charity. Furthermore, regular dialogue can lead to new connections to influential individuals who can make a difference to the charity’s work.

A share of revenue will also ensure that a large and disparate group of investors can more directly contribute to the charities that have been thoroughly researched for their environmental impact.

“As much as we’d hope that all clients who invested in a discounted product would give all the savings to charity, it may not always be the case. This arrangement ensures that a set proportion of management fees is always donated to relevant charitable causes,” said Thomas.

Channelling capital to where it’s needed

In addition to making direct contributions to environmental charities, the investment industry can also play its part by channelling capital towards companies that are creating solutions to environmental problems. For maximum impact, investment strategies should have a pure environmental focus.

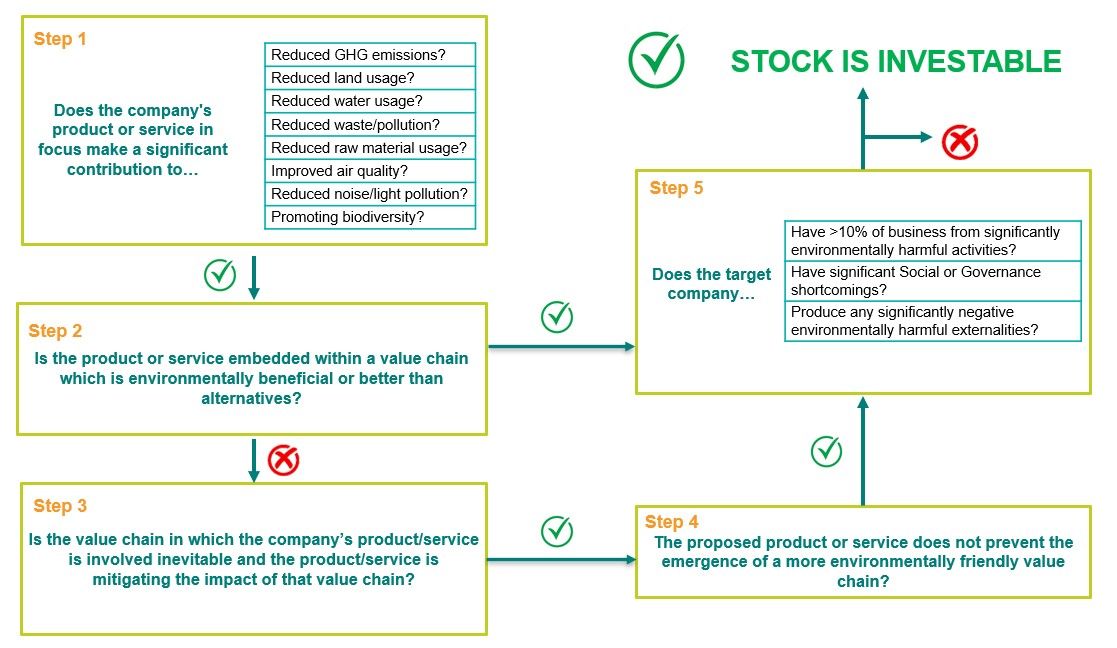

In TT’s case, the strategy aims to have at least 80% of invested capital in companies where the majority of revenues or profits stem from tackling a specific environmental problem, and all holdings must be making significant contributions to environmental solutions. This is the starting point for a stringent internal screen, which also includes analysis of the value chain these companies sit within:

TT Environmental Solutions – ‘suitability’ screen

Importantly, the investment universe is not limited to any particular geography or sector, meaning that capital can flow to the most promising areas. For this reason, there is a strong emphasis on emerging markets (EMs), where TT has significant expertise.

“Companies in these markets are attractive given that many of them are at the forefront of environmental technology,” said Thomas.

China, for example, is using its latest Five Year Plan to drive significant innovation in these types of solutions, including in the automotive and renewables sectors. Korea, meanwhile, houses some of the world’s leading battery cell tech companies. And across Latin America, such as in Chile, Brazil and Colombia, there are far-reaching commitments to developing hydro and wind resources.

“Our approach is genuinely global,” explained Thomas. “This means that even in periods where certain sectors within developed markets may get quite stretched from a valuation perspective, we are often able to find pockets of attractive relative value within environmental companies in emerging markets.”

While there is no immunity from geopolitical risks, or from frauds at companies with lower governance standards, having a historical perspective on a company’s activities, treatment of minority shareholders and general reputation acts as a buffer in the due diligence and security selection process.

Shared expertise

Wherever in the world investors look, the environment clearly represents a long-term structural story that is still in the early phase.

There is wide-ranging proof of this. For example, electric vehicles made up just 2% of auto sales globally in 2020; the International Energy Agency sees the global carbon capture and storage market growing from 40mt to 750mt in 2030 and 2,400mt by 2040[1]; and the number of solar rooftop systems on homes is set to more than double to around 100 million by 2024[2].

With such a wide range of opportunities, identifying where to invest, and how to select charities with whom to share revenue, is easier said than done.

“To help identify the most promising themes and technologies, we created a Research Advisory Board with four environmental experts and policymakers from different backgrounds. The board also helps to validate our approach to ensure we are acting in an environmentally responsible way,” explained Thomas.

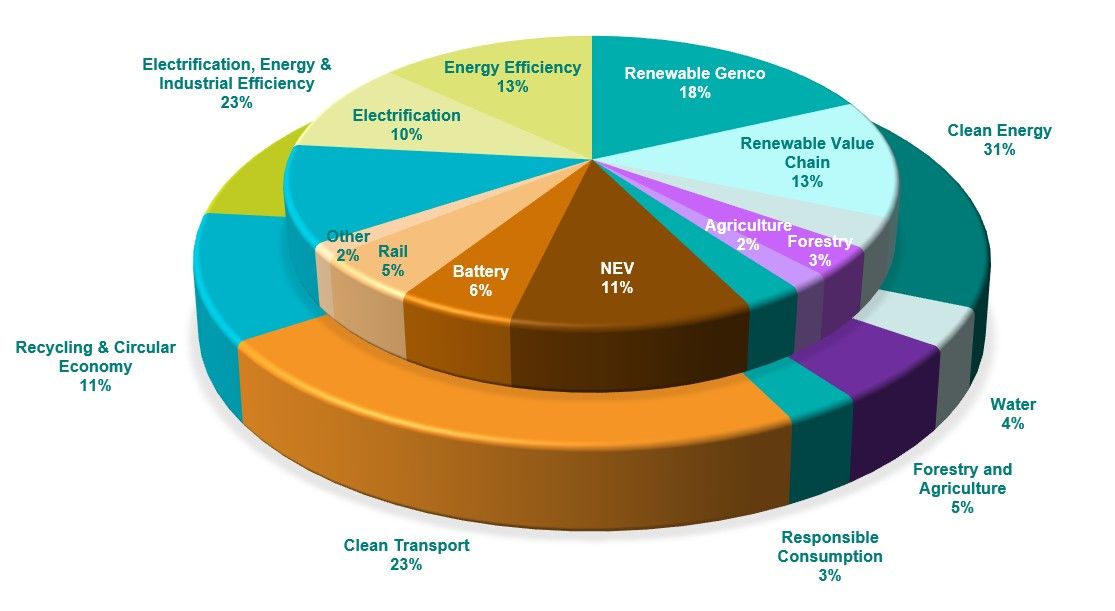

The upshot is a portfolio with exposure to seven major themes and over ten sub-themes, including forest products, the renewable value chain and energy efficiency.

“The thematic diversification ensures the portfolio is unlikely to be subject to the quantum of drawdown of more narrowly focussed environmental strategies during periods of market rotation and weaker risk appetite,” added Thomas.

TT Environmental Solutions: portfolio exposure by theme (30th April 2021)

Indeed, such diversification provided some protection to the portfolio when a recent spike in bond yields prompted a sell-off in highly-rated growth stocks, including some renewables names and electric vehicle manufacturers. By capturing the strong upward move in environmental equities in 2020, then protecting these gains through the recent correction, the TT Environmental Solutions Strategy was able to generate 117.2% in its first year since inception in May 2020. For context, the MSCI All Country World Index (MSCI ACWI) returned 45.4% over the same period[3].

Find out more about TT’s Environmental Solutions Strategy by clicking here or contacting Jason Hill (hillj@ttint.com)

[1] https://energypost.eu/carbon-capture-can-co2-eor-really-provide-carbon-negative-oil/

[2] https://www.iea.org/news/global-solar-pv-market-set-for-spectacular-growth-over-next-5-years

[3] Source: TT International, MSCI. Gross, USD terms: 12th May 2020 – 11th May 2021 (past performance is not necessarily indicative of future results and investors may not retrieve their original investment)

Important Information: This document is issued by TT International Asset Management Ltd (“TT”), authorised and regulated in the United Kingdom by the Financial Conduct Authority. This document is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. The circulation of this document is restricted to professional investors as defined in the legislation of the jurisdiction where this information is received. No representation is made as to the accuracy or completeness of any information contained herein, and the recipient accepts all risk in relying on this information for any purpose whatsoever. Without prejudice to the foregoing, any views expressed herein are the opinions of TT as of the date on which this document has been prepared and are subject to change at any time without notice. TT does not undertake to update this information. Any forward-looking statements herein are inherently subject to material business, economic and competitive risks and uncertainties, many of which are beyond TT’s control and are subject to change. The information herein does not constitute an offer of shares or units in any fund, and it is not an offer to, or solicitation of, any potential clients or investors for the provision by TT of investment management, advisory or any other comparable or related services. No statement in this document is or should be construed as investment, legal, or tax advice, nor is any statement an offer to sell, or a solicitation of an offer to buy, any security or other instrument, or an offer to arrange any transaction, or to enter into legal relations. This document expresses no views as to the suitability of the investments described herein to the individual circumstances of any recipient. Any person considering any investment should consult the offering documentation if and when is made available. Investments carries with it a high degree of risk. Past performance is not necessarily indicative of future results and investors may not retrieve their original investment.