Artificial intelligence (AI) will make companies such as the ‘magnificent seven’ even more dominant, says Dominic Rizzo, portfolio manager at T Rowe Price.

US equity performance year-to-date has been driven mostly by the so-called magnificent seven. These seven stocks: Apple, Microsoft, Amazon, Nvidia, Alphabet, Tesla and Meta, make up more than a quarter of the capitalization of the S&P 500.

Investors crowding into these names has been criticized by some market participants as an unhealthy market dynamic, especially since these tech companies have also been beneficiaries of the recent hype surrounding AI.

However, the optimism surrounding these companies’ potential to exploit opportunities in AI is not overdone, said Rizzo, who manages the T. Rowe Price Global Technology Equity fund.

Rizzo (main picture) told a recent media briefing that it is important for investors to acknowledge that many of the magnificent seven companies provide ‘linchpin’ technologies.

“If you think about a car, the axle and the wheel are connected; if you pull out the linchpin, the wheel will fall off the car,” he said.

In the same way, if one pulled these technology companies out of the ecosystem, he said their customers would be dramatically worse off, asserting that these ‘linchpin’ companies sell mission critical technologies to their customers.

“Those magnificent seven companies are magnificent,” he said. “They do provide the ultimate linchpin technologies. On a fundamental basis, they should all be well positioned for AI. I think it’s dangerous not to respect them.”

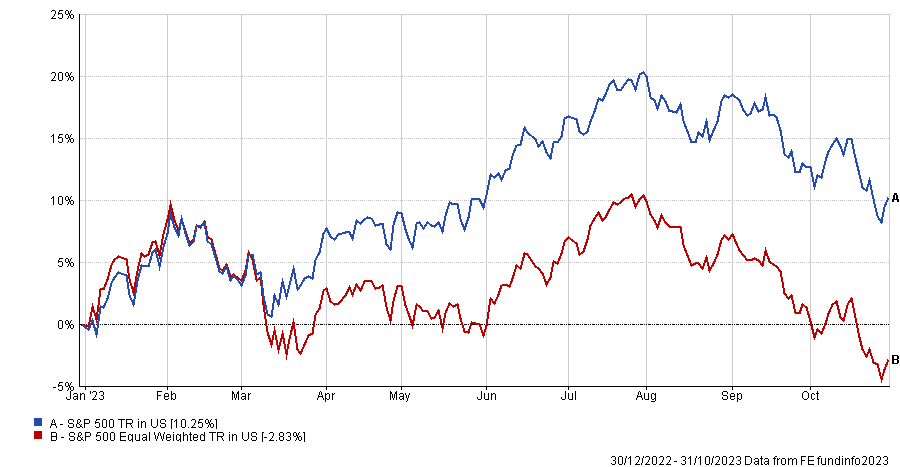

The effect that the magnificent seven companies have had on the US equity market can be seen by the divergence in returns between the S&P 500 index and the equal weighted equivalent.

In the past, whenever a new innovative technology came along, it typically disrupted incumbent companies or quite often entire industries. One recent example of this is how internet innovation paved the way for Amazon to disrupt the brick-and-mortar retail sector through ecommerce.

But this time around, Rizzo argues that AI won’t be a disruptive innovation where the technology results in new winners, but more of a ‘sustaining’ innovation where the old winners remain the same.

This is because new entrants are less likely to have the large amount of computing power, data sets, and distribution required to gain an edge with AI.

Running AI applications requires huge amounts of computing, which is becoming expensive due to the high cost of specialized chips required to train AI. Companies also need access to large data sets and a large customer base to amortise the cost of their AI investments.

AI talent is also another limiting factor for new entrants, Rizzo added. “The major companies in the US, ‘the hyperscalers’, have cornered the market on a lot of that talent,” he said. “Talent is relatively scarce.”

Investing in AI pays off

Although not necessarily part of the ‘magnificent seven’ or a ‘hyperscaler’, Adobe is a good example of how large companies with the right set of resources can get a leg-up in the race for AI, said Rizzo.

The US software company was once considered an AI “loser” by the market because of worries that people were able to create images with the large number of cheap and free generative AI tools that were becoming available.

There was a fear that this would lead to a decline in the number of creators and therefore Adobe’s customer base who pay for the company’s suite of creative products were at risk.

However, Adobe quickly reacted and invested large sums of money into AI before releasing Firefly, its own generative AI product trained on its dataset of copyrighted material that they knew would be safe for their customers to publish.

The firm then pushed their new AI product into its distribution network of existing customers.

“All of a sudden, Adobe is an AI winner”, Rizzo said. “AI is a sustaining innovation, not a disruptive innovation. The big will get bigger is my contention.”

Boost to semiconductors

Although it is still too early to see exactly how the hyperscalers, such as Microsoft, Google, and Amazon, will monetise their AI investments, Rizzo contends that there is one clear immediate beneficiary of their push towards adopting new AI technology: the digital semiconductor ecosystem.

As the US tech giants continue to invest towards building giant graphic processing unit (GPU) clusters to run AI applications, major tech companies in the semiconductor and software areas have recorded meaningful earnings growth this year, with GPU designer Nvidia at the forefront.

Chip designer AMD, which supplies all the hyperscalers, told investors it expects the AI chip market to grow from $30bn in 2023 to $150bn by 2027, which represents an almost 50% compound annual growth rate.

Commenting on this prediction, Rizzo said: “You have to keep in context that the entire global semiconductor market today is only roughly $500bn. So, this would be adding an incrementally large total addressable market on top of the global semiconductor market.”