The 2011 Tōhoku earthquake taught us that significant events can change consumer behaviour, going against Japan’s conservative society norms. The longer such catastrophes continue, the more structurally embedded the new behaviour becomes.

The Covid-19 pandemic was no exception. Firstly, it accelerated the long-anticipated digital transformation at Japanese corporates; secondly, it strengthened demand for goods and services that stretch consumers’ disposable income.

Below are examples of companies in the FSSA Japan Equity strategy that have benefitted from these changing behaviours. They characterise some of the attractive long-term investment opportunities we have found in Japan.

Growth trend 1: digital transformation

Despite Japan having one of the largest annual IT expenditures globally, the pace of digital adoption has been slow. However, the pandemic has forced companies to rethink their digital strategy. According to the Information-technology Promotion Agency, 40% of Japanese companies have now established a digital transformation (DX) project[1].

We believe this will benefit internet services and Software-as-a-Service (SaaS) companies. One example is M3, a web-based marketing platform connecting doctors with pharmaceutical companies. M3 saw orders for e-detailing surge 2.5 times in 1H2020, as doctors avoided in-person meetings with medical representatives. Given online marketing expenditure is only 1-2% of pharmaceutical companies’ marketing budgets, we believe the long-term growth potential for M3 is huge.

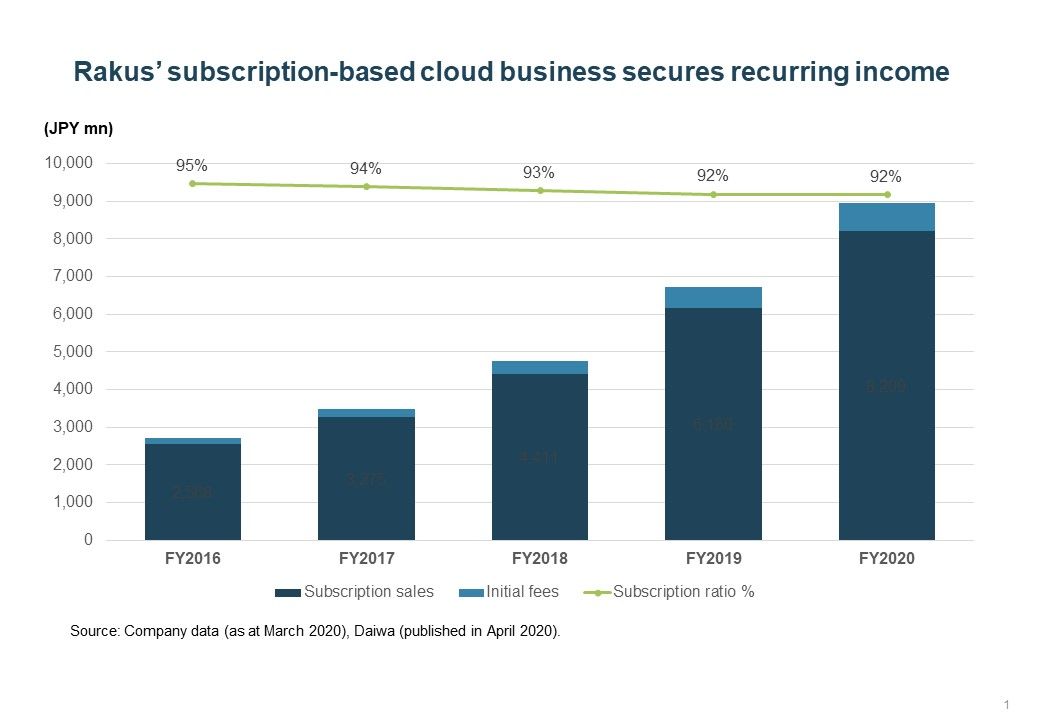

Rakus, which provides cloud-based services to small and medium-sized enterprises (SMEs), saw strong (40%+) year-on-year growth for its core expense management software. Rakus’ suite of software helps its key target market – SMEs and their employees – save significant labour and time costs. With low penetration due to limited IT literacy, we believe there should be a long runway of growth ahead.

Similarly, Bengo4.com, the largest provider of cloud-based contract software in Japan, has grown exponentially as companies adopt e-signatures in their business. Its CloudSign service has over 80% share of the Japan market, with sales up 2.6x year-on-year due to the work-from-home environment in 2020. The company estimates that less than 10% of Japanese businesses currently use e-signatures, indicating that growth could pick up significantly in the coming years.

Growth trend 2: deflationary spending

Amidst the backdrop of economic instability, demand for goods and services that stretch consumers’ real disposable income has strengthened. In Japan, “cheap” products used to be viewed with suspicion, but that perception has slowly changed as more middle-income customers visit stores like Gyomu Super and Workman.

Gyomu Super, a leading discount grocery franchise operated by Kobe Bussan, enjoyed 16% same-store sales growth in 2020, driven by stay-at-home demand and products sold cheaply in bulk. As a vertically integrated retailer, Kobe Bussan sells its private-label goods at a 30-50% discount compared to those at a traditional grocery store.

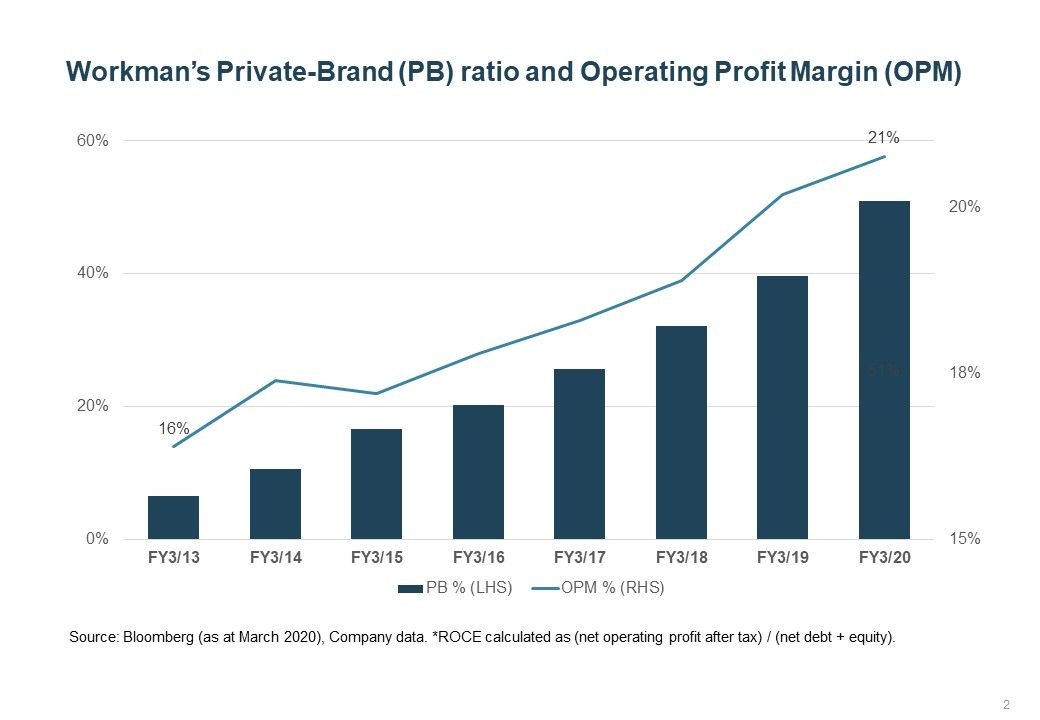

Similarly, Workman, a specialty retailer of private-label outdoors and athleisure clothing, recorded 18% sales growth in 2020, and its profit margins continue to widen. With its functional wear priced at a fraction of the big brands, demand has been so strong that its franchisees struggle to restock the shelves in a timely manner.

Customers have posted recipes made with Gyomu Super ingredients or outdoor styling with Workman clothes on their social media, leading to a cult following for these two brands. Given the performance of other discount retailers in Japan, we believe the discounting trend – particularly with Japan’s sluggish economy and muted wage growth – is here to stay.

Well positioned to reap the rewards

FSSA Investment Managers’ (FSSAIM) Japan Equity strategy is well positioned to take advantage of these long-term growth trends. At FSSAIM, we do not predict macro events, because our investment approach – as bottom-up stock selectors – seeks to identify companies that are in charge of their own destiny. While Japan consistently defies convention, we select only the companies that can thrive, regardless of the country’s economic challenges.

Learn more about FSSAIM Japan strategy –

For Hong Kong investors: click here.

For Singapore investors: click here.

Source: Company data retrieved from company annual reports or other such investor reports. As at 23 February 2021.

[1] Source: https://www.ipa.go.jp/files/000082054.pdf (Japanese language)

Important Information:

The Securities and Futures Commission has not reviewed the contents of www.firstsentierinvestors.com . The information contained within this document is generic in nature and does not contain or constitute investment or investment product advice. The information has been obtained from sources that First Sentier Investors (“FSI”) believes to be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness, accuracy, completeness or correctness of the information. No person should rely on the content and/or act on the basis of any matter contained in this document without obtaining specific professional advice. Neither FSI, nor any of its associates, nor any director, officer or employee accepts any liability whatsoever for any loss arising directly or indirectly from any use of this document. The information in this document may not be reproduced in whole or in part or circulated without the prior consent of FSI. This document shall only be used and/or received in accordance with the applicable laws in the relevant jurisdiction. Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time. In Hong Kong, this document is issued by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. In Singapore, this document is issued by First Sentier Investors (Singapore) whose company registration number is 196900420D. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors and FSSA Investment Managers are business names of First Sentier Investors (Hong Kong) Limited. First Sentier Investors (registration number 53236800B) and FSSA Investment Managers (registration number 53314080C) are business divisions of First Sentier Investors (Singapore). The FSSA Investment Managers logo is a trademark of the MUFG (as defined below) or an affiliate thereof. First Sentier Investors (Hong Kong) Limited and First Sentier Investors (Singapore) are part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. MUFG and its subsidiaries are not responsible for any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.