Both equity and fixed-income funds recorded net inflows in Singapore during the third quarter, although this belied a mixed outlook overall with different sub-asset classes performing better than others.

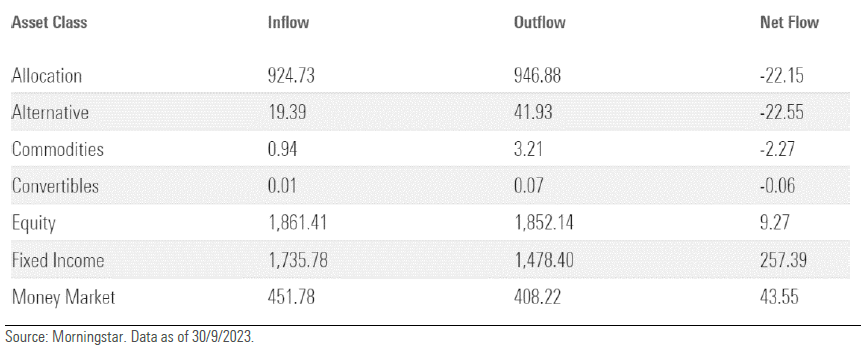

According to research from Morningstar based on the performance of all unit trusts and investment-linked insurance products included under the Central Provident Fund Investment Scheme, overall inflows into fixed income hit S$257.39m ($192.93m) for the July-September quarter.

Bryan Cheung, associate director of manager research at Morningstar, noted during a press briefing that this was unsurprising given the attractive yields fixed income have offered year-to-date, although he also noted that inflows dipped slightly compared with the first two quarters of this year.

Cheung attributed this to the fact that many fund managers started adding duration earlier this year, meaning they were hurt by the spike in long-term rates that occurred during the third quarter as a result of more hawkish noises emanating from the Fed.

Long duration bonds were also hurt during the quarter due to the pressure on Treasuries following the announcement by the US government at the end of July that it would need to sell more debt than investors had initially envisaged.

Within fixed income, investors continued to allocate to global and US fixed-income funds, with all other categories recording outflows during the third quarter. Global fixed income recorded S$539.93m in inflows, for example, while Asian fixed income had the largest redemptions at S$242.84m.

“If we look deeper into the fixed-income asset class, the trend has been pretty steady throughout this year, where global bonds with an average investment grade have continued to dominate the inflows, for example Pimco Income, which offered 6% annualised year to date,” Cheung said.

Equity net flows rise

The third quarter was a particularly tough period for equities as only a few markets, most notably the UK, recorded gains, amid concerns about the higher-for-longer environment, while Asia, notably greater China, fared particularly poorly.

Despite this backdrop, equity fund flows actually improved during the third quarter as net inflows came in at S$9.27m versus the outflows recorded during the second quarter, which was largely down to a strong performance in developed markets, notably the US and Japan.

When you scratch beneath the surface however, there were some areas which experienced weaker flows during the third quarter, Cheung noted, for example China and Asian equities, unsurprisingly.

In Japan, Cheung also noted that value-tilted equity funds fared better during the third quarter, which is not surprising given that value has outperformed growth in that market so far this year.

Meanwhile, Cheung also noted that global equity large cap saw meaningful third-quarter inflows following decent returns in the first half, although this was mainly down to a few large funds from the established fund houses such as BlackRock and JP Morgan Asset Management.

Finally, money market funds recorded net inflows of S$43.55m during the third quarter, while allocation funds, alternative funds, commodities funds and convertible bond funds all recorded net outflows at -S$22.15m, -$22.55m, -S$2.27m and -S$0.06m respectively.