US equities will continue to outperform in 2025, but with more market breadth than compared to the past few years.

This is one of Schroders ‘top 10 predictions’ for 2025 where the firm’s head of multi-asset investments for Asia, Keiko Kondo, has the highest conviction.

“As the US yield curve normalises and enters a policy loosening cycle, prospects for the global stock market looks favourable,” she said.

In the US, with inflation falling below 3%, and the economy experiencing a ‘soft landing’, it is paving way for a sweet spot for equities, according to Kondo, who favours broad-based exposure to US equities.

Although the upside for US equities will be smaller than the past 12 months, Kondo told a media briefing in Hong Kong that she prefers US equities over other developed markets going into 2025.

This bullish call on US equities is a continuation of the firm’s call last year where it expected US equity markets to outperform despite widespread fears of a recession.

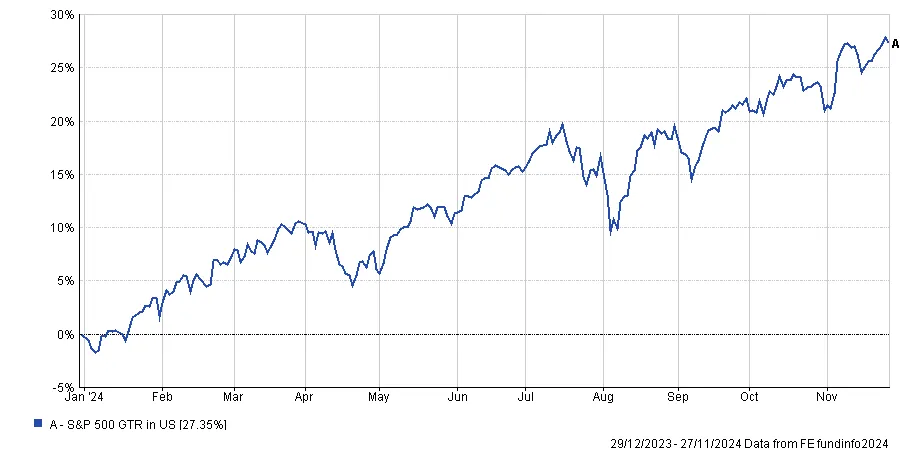

US equities are up some 27% year-to-date as rate cuts have been pushed back and the US economy seems to have avoided a widely anticipated recession.

Much of the recent performance has been driven by the continued strength of US mega-cap tech stocks such as Nvidia, Meta and Microsoft.

However next year, Kondo believes US equity performance will broaden out and favours an equal weighted S&P 500 index exposure to the asset class.

“It’s not only about the mega cap stocks, it’s more about the broader segments within US equities,” she said. “On the flip side of the mega cap growth will be something like value like banks and financials. Compared to the mega-caps you can think about the mid and small-caps.”

“US equities should continue to do well, but be supported by the broader base, rather than a narrow-led market we’ve seen.”

She added that in history, an inflation rate of between 1% and 3% has been a good environment for US equities.

Another call for 2025 where Kondo has relatively higher conviction is Asia credit.

She said: “Asian investment grade [IG] has actually done very, very well, even compared to other developed markets credits, but they are still trading at higher spreads than equivalent corporate IG for US or Europe – so it does still offer more attractive carry.”

She did not specify between Asian investment grade or high yield “because the Asia credit universe has improved in quality over the years,” she said.

A few years ago Asian credit used to be dominated by high yield issuers, particularly property related names, but Kondo argues that the investment universe is now much more dominated by investment grade names and the high yield universe itself has a much more diverse range of sectors besides property.

“I do not need to necessarily exclude high yield,” she said. “Even now some parts of high yield does offer interesting opportunities.”

“In fact, I do see my colleagues that are running Asia credit books running lower quality IG and high quality, high yield as the areas to find opportunities, regardless of the sector.”

When it comes to commodities, Kondo is bullish on gold after its stellar run in 2024.

She cited its status as a safe haven asset, as well as the trend of central banks shifting away from the US dollar as their sole source of reserves. She added that gold also provides useful diversification properties for investors.

Kondo is bearish on oil however, where she prefers to have a short exposure going into 2025 due to rising supply dynamics that she believes will start to bite.

“The outlook for oil is a bit questionable,” she said. “When we look at all these OPEC+ countries – which are likely to start producing more oil – the expected inventory level of the oil for next year compared to the historical typical pattern of recent years is gradually creeping up.”