Index trackers are comfortably beating actively-managed vehicles in the race to attract new capital, according to order flows monitored by Calastone, a funds network that connects financial institutions.

“Index tracking funds are steadily taking over the fund management industry,” argues Edward Glyn, managing director, head of markets at Calastone.

Across its global network, they garnered inflows of $10bn in 2019 and $13.5bn in 2020. The value of buy orders was almost 20% higher than sell orders over the two-year period, indicating strong, consistent buying.

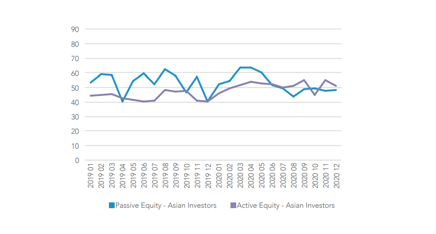

Across every major territory, including Asia-Pacific and in all equity fund categories, Calastone’s indices of passive funds have outpaced their active equivalents.

In contrast, active funds saw net outflows of $11.4bn in 2019 and would have shed cash again in 2020 were it not a sudden turnaround in the final quarter. Only by the middle of November had active equity funds recouped all the earlier 2020 outflows and, by the end of the year, investors added a net $6bn to their holdings.

“The combination of lower trading volumes with steadier inflows for index trackers proves that investors are ‘buying and holding’. Index funds are now firmly cemented into savings plans, with automatic buy orders placed every month,” noted the report.

Flows in mainland China were not included in the study, although Vanguard, the world’s largest provider of passive funds, earlier this week said that it was delaying its application for a fund management company licence in China, partly because of “strong investor preference for actively managed funds”.

However, investors in Hong Kong withdrew capital from active funds in each of the last two years, while adding to index trackers. Taiwanese investors were net sellers of both active and passive funds over both years, but the outflows from active funds were fifty times larger, Calastone’s analysis found.

Nevertheless, 72% of funds in Hong Kong are still actively managed and in Singapore, active funds represent almost the entire open-ended fund market.

Calastone Fund Flow Index of investor behaviour in Asia

CONSISTENT BUYING

Flows into index funds are relatively stable and buying has consistently outgunned selling, reflecting a simple ‘buy and hold’ strategy that accumulates savings over time. Net inflows are large compared with total trading volumes.

Conversely, investors trade their active funds much more often, picking favoured funds, adding money opportunistically in response to news-flow, and re-allocating their assets around by switching between funds with a particular regional focus or favoured strategy, according to Calastone’s findings.

Calastone analysed hundreds of millions of buy and sell orders from 2019 and 2020, tracking monies from IFAs, platforms and institutions as they flow into and out of investment funds. A single order is usually the aggregated value of a number of trades from underlying investors passed for example from a platform via Calastone to the fund manager.

Its Fund Flow Index compares net fund flows to total trading activity so that a small value of buying does not score highly in a big, actively traded fund category, but is rated as significant in a smaller one. A neutral score of 50 means the value of orders equals the value of sell orders. A reading of 75, for example, means the value of buy orders is three times greater than the value of sell orders.

“For active funds, total trading activity is very large and the resulting net inflow or outflow is extremely small by comparison to overall volumes,” the firm noted.

High trading volumes in active funds reflect frequent decision making rather than popularity; active funds shed $5.4bn of capital over two years.

The value of inflows in passive funds depends on the extent to which index trackers have become embedded in the local savings culture. In Singapore, for example, index funds are scoring higher, indicating steadier buying, but the overall value of capital flowing into active funds is significantly greater.

Index funds account for less than a fifth of equity fund turnover on Calastone’s network, less than their share of AUM (active funds made up the rest).

But, “this is because investors are steadily buying,” concluded Calastone.