In February this year, amid anxieties about the decline in the number of listings on the Singapore stock exchange (SGX), Singapore’s authorities planned to inject about $4bn to reverse the trend.

The Monetary Authority of Singapore revealed a raft of measures to encourage the Lion City’s equity markets, as de-listings continued to outnumber initial public offerings.

Proposals included a plan to invest S$5bn ($3.7bn) in funds that are focused on the local equity market, a more streamlined listing process and tax incentives for both companies and investors.

The number of companies listed on SGX, Singapore’s stock exchange, hit a two-decade low in 2024, falling to 617 from a high of 782 in 2013.

The investable universe is certainly low, but that universe already contains high quality financial institutions and corporations. It is doubtful whether these new incentives would attract similar large-cap listings, especially when alternative venues, notably New York, has access to a substantially larger and more accessible investor base.

Against this background, FSA asked Hunter Beaudoin, analyst at Morningstar to compare two Singapore funds, the Nikko AM Shenton Thrift fund and the Schroder Singapore Trust fund.

| Nikko | Schroder | |

| Size | S$429m | S$950m |

| Inception | 1987 | 1993 |

| Managers | Kenneth Tang, Yeu Huan Lai | Chuanyao Lu |

| Three-year cumulative return | 55.66% | 42.13% |

| Three-year annualised return | 15.39% | 12.07% |

| Three-year annualised alpha | 3.25 | 0.29 |

| Three-year annualised volatility | 14.77% | 14.85% |

| Three-year information ratio | 0.85 | 0.14 |

| FE Crown fund rating | ***** | **** |

| Morningstar rating | ***** (Bronze) | *** (Neutral) |

| OCF (retail share class) | 0.83% | 1.32% |

Investment Approach

The co-managers of the Nikko AM Shenton Thrift fund, Kenneth Tang and Yeu Huan Lai, have designed a “bottom-up driven investment process that has consistently added value in the concentrated and narrow Singapore equities market,” according to Hunter Beaudoin, analyst at Morningstar.

Fundamental analysis is conducted on stocks through the lens of sustainable returns and fundamental change. Each of these two pillars is composed of several subpillars, such as franchise; financials; environmental, social, and governance; and market structure for the former and company-specific and external drivers for the latter, Beaudoin explained.

Analysts assign quantitative scores to these subpillars. “While they also have discretion in setting the subpillar weightings, these are only altered when there are fundamental changes to their relative importance, and they must pass through a peer review process,” he said.

Valuation was formalized as a third pillar in mid-2023 to reflect the team’s existing valuation assessment.

“The strategy’s style- and market-cap-agnostic approach has contributed to a higher active share and a small/mid-cap bias relative to peers, which have generated alpha for investors over the long run,” noted Beaudoin.

The 25-to-45-stock portfolio may also hold a maximum of 30% in non-Singapore-listed companies, though the managers have used this flexibility in a prudent manner and the exposure averaged less than 5% over the past three years.

“This has allowed the strategy to obtain exposure in areas that are underrepresented in Singapore, such as IT and healthcare,” Beaudoin said.

Turning to the Schroder Singapore Trust fund, the Morningstar analyst warned that despite a repeatable and well-structured framework, concerns over a low level of active management persist.

Recently appointed lead manager Chuanyao Lu continues to implement the existing quality-focused investment approach. It is premised on a bottom-up research framework also utilised by other highly rated Schroders Asian equity strategies and seeks to identify companies with sound fundamentals, high earnings visibility, and a commitment to growing shareholder value over time.

After the universe is screened for size, liquidity, and sustainability factors, stocks are assessed and categorized as either superior, positive transition, negative transition, or inferior based on the level and trajectory of their return on invested capital relative to their weighted average cost of capital.

The process is rounded out with a fair value estimate and analyst grade of 1 to 4 for each stock, with 1 representing a strong conviction it will outperform.

“However, the portfolio continued to sport low levels of active share (a measure that indicates how different a portfolio is from its benchmark), raising concerns about the strategy’s ability to deliver alpha,” said Beaudoin.

The portfolio’s active share of about 20% against its FTSE Straits Times Index prospectus benchmark continues to sit at historically low levels, and its active share against the MSCI Singapore Index category benchmark has consistently been among the lowest in the peer group over the past five years, he pointed out.

While the portfolio’s activeness has rebounded slightly since Lu took over as lead manager as he’s consolidated the number of holdings to around 20-30 from a historical range of 30-40, “the strategy’s alpha potential continues to be limited by current active share levels, which lessen the competitive edge of the process,” Beaudoin added.

Fund characteristics

Sector allocation:

| Nikko | Schroder | |

| Financials | 52.4% | 57.9% |

| Industrials | 17.3% | 8.6% |

| Communication services | 6.9% | 10.5% |

| Utilities | 6.0% | 7.5% |

| Real estate | 5.8% | 11.5% |

| Technology | 4.4% | 1.4% |

| Others | 5.5% | 4.0% |

| Consumer staples | – | 1.0% |

| Consumer discretionary | – | 0.4% |

Top 10 holdings:

| Nikko | weighting | Schroder | weighting |

| DBS | 21.6% | DBS | 24.5% |

| UOB | 13.5% | OCBC | 17.6% |

| OCBC | 10.9% | Sing Telecom | 10.5% |

| Sing Technologies | 6.0% | UOB | 9.7% |

| Sembcorp | 6.0% | Singapore Exchange | 5.0% |

| Singapore Exchange | 5.3% | Capital and Ascendas Reit | 4.4% |

| Singapore Telecom | 5.3% | Keppel | 4.1% |

| Yangzjiang Shipbuilding | 4.1% | Yangzjiang Shipbuilding | 3.9% |

| First Resources | 3.6% | Sembcorp | 3.5% |

| Comfortdelgro | 2.8% | Singapore Technologies | 3.5% |

Performance

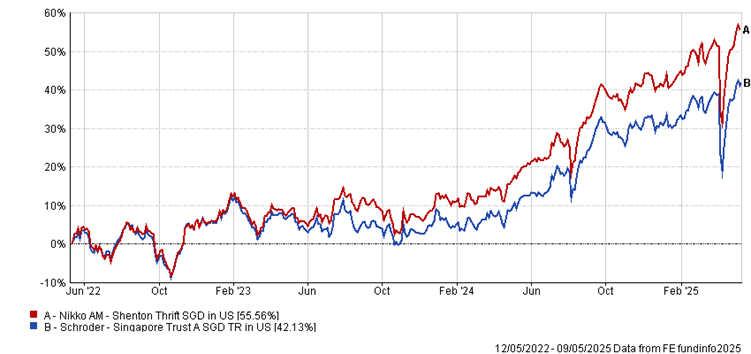

The performance of the Nikko fund managed by Kenneth Tang and Yeu Huan Lai’s “has been impressive,” said Beaudoin.

It has generated a three-year cumulative return of 55.66% in Singapore dollar terms, according to FE fundinfo data, and achieved alpha of 3.25 and an information ratio of 0.85 during the same period.

The Schroder fund has achieved a 4.13% three-year cumulative return, FE fundinfo data shows. It has earned less alpha (0.29) than the Nikko strategy and it has been slightly more volatile 14.85% versus 14.77%) during the same period.

In both cases, “stock selection drives performance,” explained Beaudoin.

The Nikko managers focus on high quality companies with strong downside resilience.

They are style agonistic – which meant the fund struggled in 2021, and their tilt towards small- and mid-cap funds dragged on performance in the following year.

“But their selections add value over time, and in 2024 the fund outperformed the benchmark by 5%,” noted Beaudoin.

Notably, an off-benchmark investment in Yangzijiang Shipbuilding contributed the most to relative returns, as the company reported strong net profit growth with an accelerating order book.

“Chuanyao Lu was appointed lead manager of the Schroder fund 1 July 2024 and has recently begun building his own track record here,” said Beaudoin.

During Seok Hooi Teoh’s tenure as lead manager from January 2005 through June 2024, the strategy’s oldest SGD A Dis share class returned 5.81% per year (in Singapore dollar terms), outperforming the MSCI Singapore Index category benchmark by 68 basis points and ranking in the 25th percentile of category peers but underperforming its FTSE Straits Times Index prospectus benchmark by 56 basis points, according to Morningstar data.

“Though Lu has yet to build a meaningful track record as lead manager, we expect performance to remain driven by stock selection and continue to provide downside protection thanks to his adoption of his predecessor’s quality-focused, bottom-up investment approach,” Beaudoin said.

Discrete calendar year performance

| Fund | YTD* | 2024 | 2023 | 2022 | 2021 | 2020 |

| Nikko | 5.32% | 28.55% | 5.31% | 3.96% | 6.92% | -1.80% |

| Schroder | 3.26% | 23.53% | 1.78% | 3.63% | 11.46% | -10.52% |

Manager Review

The Nikko fund’s co-managers Kenneth Tang and Yeu Huan Lai “are highly collaborative and continue to impress with their deep market expertise,” said Beaudoin.

Tang and Lai are seasoned investors with 28 and 26 years of investment experience, respectively, and have comanaged this strategy since December 2013.

“At our meetings, they have consistently shared astute stock insights and displayed a close working dynamic,” said Beaudoin.

They also co-manage several active Singapore and Asean equity strategies together, which carry significant overlaps with the Nikko AM Shenton Thrift portfolio and have delivered solid performances over their tenure.

However, Tang and Lai were both named on some passive strategies in November 2023, and Lai was also promoted to joint head of Nikko’s 18-member Asian equity team alongside Peter Monson in July 2023.

“The additional workload is a watchpoint, though the managers’ extensive experience and longstanding collaboration provide reassurance they can continue to successfully manage this strategy,” Beaudoin said.

Tang and Lai are supported by nine analysts with Singapore equity coverage who average 16 years of experience and sit within the Asian equity team. They provide broad coverage of the investable universe and have remained relatively stable.

Chuanyao Lu replaced Seok Hooi Teoh as the Schroder strategy’s lead manager in July 2024, ahead of Seok Hooi Teoh’s October 2024 retirement. Teoh’s boots are hard to fill.

Teoh was a Schroders veteran, having spent the past 30 of her 35 years in the industry at the firm. She managed this strategy since January 2005, achieving solid results against the MSCI Singapore Index, Morningstar category benchmark and category peers over her tenure.

“The loss of her local market knowledge and expertise accumulated from leading this strategy through multiple market cycles is a significant setback,” said Beaudoin.

Lu started his investment career in 2008 and joined the firm in 2017. He was appointed the strategy’s comanager alongside Teoh in June 2021 and previously supported it as an analyst covering telecoms, real estate, and industrials stocks in Singapore.

“Although Lu’s appointment as succeeding lead manager is sensible, we don’t have the same level of conviction in him as in Teoh. This is his first stint managing money, and it is yet to be seen how he will fare without Teoh’s mentorship,” said Beaudoin.

Yet, Lu continues to implement the existing investment process. “It is well-structured and seeks to identify companies with sound fundamentals, high earnings visibility, and a commitment to grow shareholder value over time,” Beaudoin noted.

Lu has the support of a stable bench of seven analysts (including himself) from Schroders’ Asia-Pacific ex-Japan equities team averaging around 20 years of experience and a decade of firm tenure.

“Nonetheless, this is his first stint managing money as a lead manager, and it will take time for us to gain comfort in his ability to successfully run this strategy without Teoh’s guidance,” said Beaudoin.

Fees

The Nikko fund’s ongoing charges figure (OCF) is only 0.83%, which Beaudoin confirms is cheap, and he this share class will be able to deliver positive alpha relative to the category benchmark index, explaining its Morningstar medalist rating of bronze.

Although the OCF of the Schroder fund is higher at 1.32%, “it is not expensive,” he said. Nevertheless, based on its assessment of the fund’s People, Process, and Parent Pillars in the context of these expenses, Morningstar doesn’t think this share class will be able to deliver positive alpha relative to the category benchmark index, explaining its Morningstar medalist rating of neutral.

Conclusion

“We favour the Nikko fund over the Schroder fund, which is reflected in the award of a bronze medalist rating to the strategy,” said Beaudoin.

The Schroder fund has its merits as a conservative fund with a large-cap focus, however “we remain watchful of the new lead manager’s performance and strategy because his tenure is so short. In particular, we will monitor the active share of his portfolio,” Beaudoin said.

In contrast, the Nikko fund benefits from the strong track record of two veteran managers who have successfully stewarded the strategy for many years.

“We are impressed too by the systematic structure of its investment process, the prominent degree of activism, its downside risk protection and its high conviction,” Beaudoin concluded.