Daniel Nicholas

Client Portfolio Manager, Harris l Oakmark (an affiliate of Natixis Investment Managers)

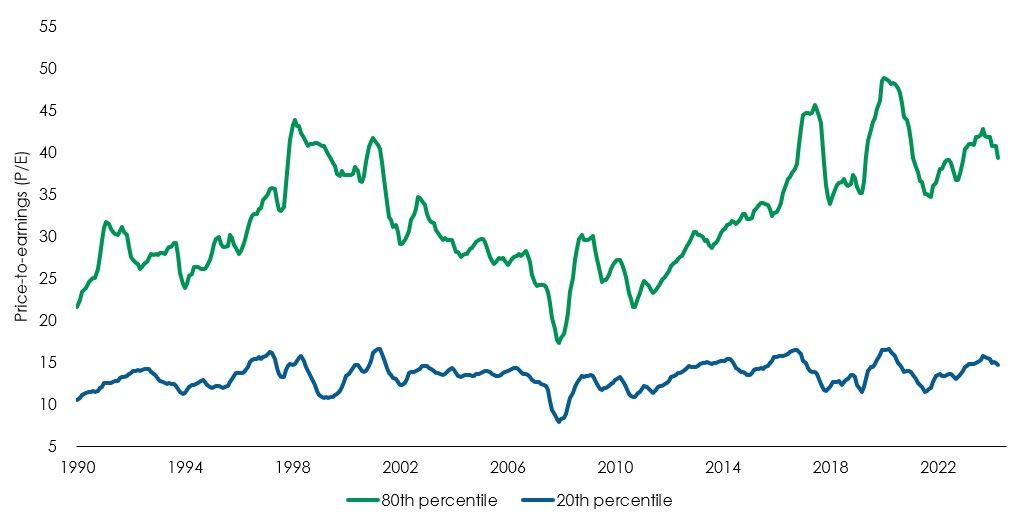

Equity valuations are still elevated, so are equity opportunities

While US stocks have fallen so far this year, US large cap indices are still trading at valuations well above their long-term averages. And due to the narrowness of the rally in recent years, the number of stocks to pick from with strong fundamentals priced at very low relative price to earnings (P/E) ratios is higher than normal. The graph below shows that while valuations of the S&P 500’s most expensive stocks have risen considerably over the previous 15 years, the lowest valued stocks have barely risen at all.

S&P 500 P/E ratios by decile

Today’s S&P 500 is riskier than you think

If you add up the five largest holdings in the S&P 500 today, they make up about 27% of the index. While this concentration is well known, it’s not so well known that you need to go back to 1957 to find a similar level of concentration. As the graph below shows, in the 40 years after 1957 these five companies were consistently outperformed by other businesses and could not hold onto their weightings in the index.

Top five S&P 500 holdings’ share of market capitalization

At the same time as the S&P 500 is increasingly concentrated in fewer stocks it is also more concentrated from an industry perspective. In 1957, the top companies were diversified across industries including automotive, industrial, oil, communications and chemicals. Today, the concentration is almost all in one industry, Information Technology, which accounts for 30% of the S&P 500i.

While US and global large cap indices have become much more expensive in recent years, the average valuation within our strategies continues to decrease: The S&P 500 today sells at a P/E multiple which is nearly twice as high as the P/E level in our large cap strategiesii.

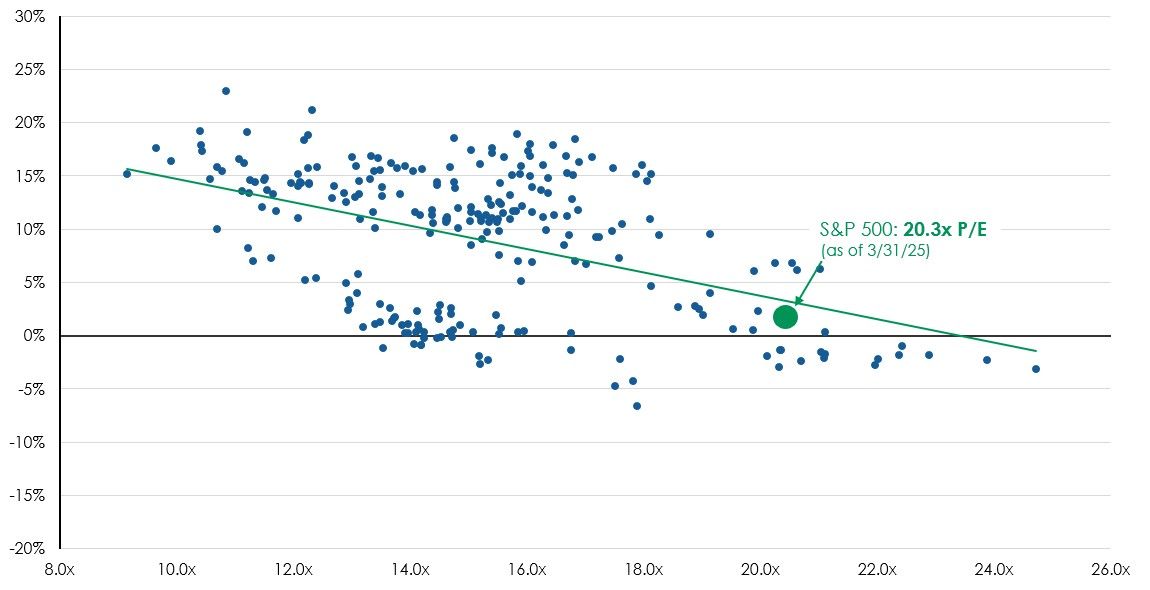

The lower the price, the higher the potential reward

While nobody can accurately predict where the stock market will go from here, we can draw conclusions and estimate probabilities, by looking at historical performance. As the chart below illustrates, history is clearly telling us that when markets are at these kinds of highs, then it is likely that future returns will be below average.

S&P 500 forward price-to-earnings (P/E) and subsequent five-year annualised returns

Past performance is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. All returns reflect the reinvestment of dividends and capital gains and the deduction of transaction costs.

Are valuations starting to matter to investors again?

Amid this intense volatility there are signs that investors are starting to return to fundamentals; starting to care, again, about the price they pay for stocks. The Russell 1000 Value Index outperformed the Russell 1000 Growth Index for the first three months of 2025 by more than 10%iii. Yet despite this outperformance, US equities remain an attractive hunting ground for us, as highlighted recently by our CIO-US, Bill Nygren:

“For the investor that’s focused on excess return without taking excess risk, there’s a lot of opportunity away from those handful of stocks that have become so popular. The return on the average Magnificent Seven stock has been negative since early July 2024 and is down 20% since its December peak. That’s the pattern in investing: Once everyone is talking about how great an investment is, it is usually no longer that great.”

i Spglobal.com, as of 31 March, 2025

ii Source: Harris l Oakmark, as of 31 March, 2025 the Harris Large Value Strategy had a P/E of 11.6 vs 20.3 in the S&P 500

iii FTSE Russell Index Calculator. From 1 Jan. 2025 to 31 March, 2025

For readers in Hong Kong, click here to learn more.

For readers in Singapore, click here to learn more.

Disclaimers:

In Singapore: This document is provided by Natixis Investment Managers Singapore Limited having office at 5 Shenton Way, #22-05/06, UIC Building, Singapore 068808 (Company Registration No. 199801044D). Mirova Division (Business Name Registration No.: 53431077W) and Ostrum Division (Business Name Registration No.: 53463468X) are part of NIM Singapore and are not separate legal entities. The content of this document is strictly confidential and has been prepared for informational purposes only and for the exclusive use of institutional and accredited/professional clients or prospects. Under no circumstance may a copy be shown, copied, transmitted or otherwise distributed to any person or entity other than the authorised recipient without the advance written consent of Natixis Investment Managers Singapore Limited. Investment involves risk. The information contained herein does not constitute an offer to sell or deal in any securities or financial products. The content herein may contain unsolicited, general information without regard to an investor’s individual needs, objectives, risk parameters or financial condition. Therefore, please refer to the relevant offering documents for details including the risk factors and seek your own legal counsel, accountants or other professional advisors as to the financial, legal and tax issues concerning such investments, if necessary, before making investment decisions in any fund mentioned in this document. Past performance and any economic and market trends or forecast are not necessarily indicative of the future or likely performance. Certain information included in this document is based on information obtained from other sources considered reliable. However, Natixis Investment Managers Singapore Limited does not guarantee the accuracy of such information. Natixis Investment Managers Singapore Limited is a business development unit of Natixis Investment Managers, the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. The investment management subsidiaries of Natixis Investment Managers conduct any regulated activities only in and from the jurisdictions in which they are licensed or authorised. Their services and the products they manage are not available to all investors in all jurisdictions. It is the responsibility of each investment service provider to ensure that the offering or sale of fund shares or third-party investment services to its clients complies with the relevant national law. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

In Hong Kong: The content of this document is strictly confidential and has been prepared for informational purposes only and for the exclusive use of professional investors. Under no circumstance may a copy be shown, copied, transmitted or otherwise distributed to any person or entity other than the authorised recipient without the advance written consent of Natixis Investment Managers Hong Kong Limited. Investment involves risk. The information contained herein does not constitute an offer to sell or deal in any securities or financial products. The content herein may contain unsolicited, general information without regard to an investor’s individual needs, objectives, risk parameters or financial condition. Therefore, please refer to the relevant offering documents for details including the risk factors and seek your own legal counsel, accountants or other professional advisors as to the financial, legal and tax issues concerning such investments if necessary, before making any investment decisions in the fund(s) mentioned in this document. Past performance information presented is not indicative of future performance. If investment returns are not denominated in HKD/USD, USD-/HKD-based investors are exposed to exchange rate fluctuations. Natixis Investment Managers Hong Kong Limited is a business development unit of Natixis Investment Managers, a subsidiary of Natixis that is the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. Certain information included in this material is based on information obtained from other sources considered reliable. However, Natixis Investment Managers Hong Kong Limited does not guarantee the accuracy of such information. Issued by Natixis Investment Managers Hong Kong Limited.