Many investors have been arguing that the market has priced in too many rate cuts because inflation remains above 2% and the US economy remains surprisingly resilient.

However central banks will cut rates regardless of inflation due to impending slower growth, according to Manulife’s global chief economist Frances Donald.

“We will see central banks make some uncomfortable admissions in 2024,” she told a recent media briefing. “Almost all global central banks will be cutting interest rates with inflation still above their targets. They’ll do this as growth begins to falter.”

“We also expect to see tacit admission that much of the inflation we witnessed in the past several years was indeed supply side driven and created by many transitory factors,” she added.

Inflation came down sharply in 2023 as central banks raised interest rates at the quickest pace in 40 years to levels not seen in decades.

However, inflation isn’t coming down because of central bank tightening, Donald argues – pointing to Japanese inflation as an example.

“We are seeing significant slowing of inflationary pressures in Japan, which has not embarked on a significant tightening cycle at all and yet is still benefiting from the decline and the easing of supply chain pressures,” she said.

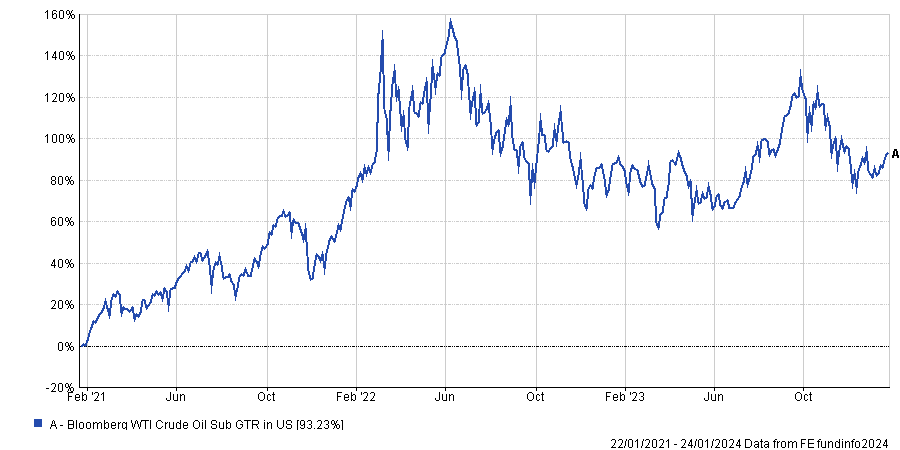

Indeed, oil prices – previously a major driver of inflaiton in 2022 – seem to have stabilised after the initial shock of the Ukraine-Russia conflict and global supply chains have also normalised after the disruption caused by the Covid-19 pandemic.

Performance of Bloomberg WTI Crude Oil Sub index over 3 years

While the market expectation is that the US Federal Reserve will cut gradually throughout the year to match a soft-landing scenario, Manulife’s chief economist said rate cuts may happen later than most expect, and at a quicker pace.

“Typically, when the Federal Reserve begins an easing cycle, it is not slow with a few cuts,” Donald (pictured) said. “Cuts are usually significantly larger.”

“Historically, when the Federal Reserve cuts, they cut by about 400 basis points – that’s double what the markets are currently expecting.”

“So, we need to keep an eye out for the possibility that the Federal Reserve start cutting later, but cut by significantly more.”

Supply-side driven inflation

Another factor investors need to bear in mind is the fact that supply-side driven factors will have an outsized impact on the economy going forward, Donald argued.

Indeed, supply-side shocks have been increasing in frequency over the last few years, more recently with the violence in the Red Sea and its impact on global shipping routes, as well as extreme weather events and the subsequent impact on commodities.

“The post-Covid global economy is being driven substantially more by supply side factors,” Donald said.

“Supply side factors have not typically been the core drivers of our economies and therefore when we rely on economic models that are focused on the demand side, they have been less useful for us.”

This will change the way that governments and central banks respond to shocks such as labour shortages, weather events and supply chain disruptions, she explained.

Donald said: “That will represent a shift in the way we model out interest rates globally.”

The economist expects to see labour shortages and weather to be “structurally inflationary” at the margin going forward, despite the rapid decline in inflation witnessed in 2023.

However, although she is predicting a global growth slowdown, Donald said it is best described as “darkest before dawn” because after every slowdown is a re-acceleration of growth.

“That re-acceleration in growth coming out of the other side of 2024 is going to represent important market opportunities for many asset classes,” she said.