Emerging markets (EMs) have more to offer investors beyond China. They are the location of much of the world’s manufacturing and their financial markets are likely to be beneficiaries of easing global interest rates.

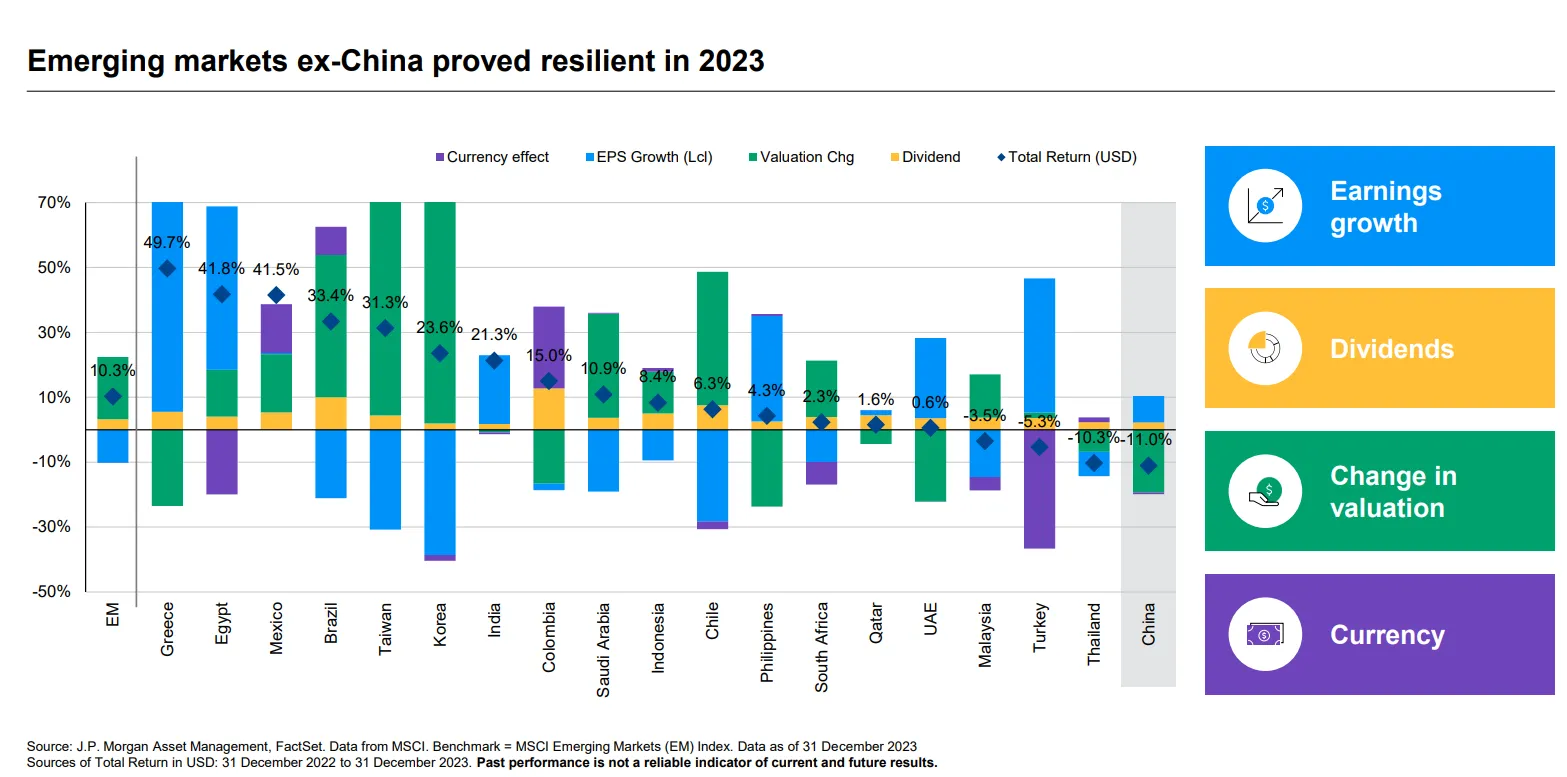

In fact, the 18 emerging markets ex-China proved resilient in 2023, with a total return of 10.3%, including factors of change in valuations, currency effect, dividends and EPS growth.

“Yet, EM are under-owned and are too large and important to ignore,” Emily Whiting, executive director, emerging markets and Asia Pacific equities team, JP Morgan Asset Management (JPMAM), told FSA at the JPMAM’s International Media Summit, in London last week.

Stock-picking strong, flexible companies

The type of stocks JPMAM favours include companies with strong balance sheets and low leverage. They should also have business adaptability, so they can shift focus to benefit from new trends.

“Corporate management skill is very important and hence their ability to build up and sustain trust,” Whiting (pictured) said. “This means having on the ground presence in countries we cover; we can’t outsource decision making. Stock liquidity is also essential.”

JPMAM does not hedge foreign exchange risk – instead it is a factor when stock picking.

At JPMAM, emerging markets portfolios, as with most of its strategies, are constructed from bottom-up sock picking analysis. Nevertheless, Whiting has regional preferences for North Asia (Korea and Taiwan) for technology stocks, and India and Asean (including Indonesia, Singapore and Thailand) for manufacturing and supply chain stocks.

JPMAM is overweight long-term growth and short-term momentum markets, such as Korea, and although underweight the widely bought India market, she believes it still offers value stocks and the structural case is strong.

Strategically bound to China amid constraints

JPMAM is committed to China through its onshore presence and its belief in its long-term prospects as a solid investment location. “However, although there is a lot of value among consumer, technology and renewables stocks – especially components – the market is volatile,” Whiting said.

Chinese consumer confidence remains weak, so any recovery is likely to be protracted. Consumer confidence needs to recover from a very low level, with Chinese households having accumulated added surplus savings.

Indeed, there has been a net increase of Rmb9.9trn ($1.4trn) in 2021, Rmb17.8trn in 2022, and Rmb11.2trn in the first eight months of 2023. In contrast, there was a net increase in household debt of just Rmb7.9trn, Rmb3.8trn, and Rmb3trn, respectively, according to JPMAM data.

“The Chinese government is managing tail risks in property but failing to restore confidence: prices and sales volumes have plunged during the past four years,” said Whiting.

Nevertheless, China comprises about 25% of the MSCI EM index and JPMAM maintains a neutral allocation. On the other hand, a lot of the bad news is already priced in the stock market. MSCI China price-to-book is just over 1 and drawdowns have peaked at -60%, she noted.

Elsewhere in developed Asia, Japan is going from “strength to strength”. “The biggest reason to invest in Japan is improving corporate governance,” according to Whiting. On a structural basis, “Japan is a bottom-up story”, while tactically, investors will closely monitor the impact of the Bank of Japan’s rate hikes to contain inflation and wages on the yen.

Basically “Japan is still under-invested, under-owned and under-valued,” she said.

Of course, EM equities are made up of many more countries and regions than Asia. Brazil, Mexico and Chile, for example, are firmly on JPMAM’s radar.

Latin America buoyed by interest cuts

“Latin America is interesting because, as the Fed cuts rates, so Latin American central banks will follow suit, which will prompt a boost in credit growth and spending,” said Whiting.

“Latin America will be a key beneficiary of US interest rate cuts,” said Whiting. Inflation has fallen from a peak of 10% in 2022 to 5% in November 2023 and nominal policy rates have been deflated by 12-month inflation expectations in Brazil, Chile and Mexico.

The greatest risk to EMs is if the US Federal Reserve leaves it too late to cut rates or if it is forced to respond quickly to recessionary pressures,” said Whiting.