Even though today the fund management industry classifies technology-focused funds as sector strategies, they will be considered more of a core exposure with secular growth in the not-too-distant future.

This is the view of Joseph Wilson, manager of the $7.4bn JP Morgan US Technology fund, who told FSA in an interview: “While we’re defined today as a sector fund, it’s clear to me – and I think it will be clear to a lot of investors in five to ten years – that this is actually a secular fund.”

“When a company takes leadership in any industry, it will be because of their adoption and harnessing of technology or the building and development of their own proprietary technology,” he explained.

When investors consider their equity exposure, technology and other sector specific strategies typically come secondary to core equity funds which take precedence in portfolios.

However, Wilson (main picture) argues that technology is the basis for growth and leadership in today’s equity market, especially with the progression of artificial intelligence (AI).

“Tech is core,” he said. “It is core to everything that is important from a business standpoint going forward.”

Indeed, there are examples of this having already played out in certain industries. The advertising industry has rerouted nearly all advertising revenues towards a few technology firms: Alphabet and Meta.

This trend is becoming more evident even in the healthcare industry as pharmaceutical companies capitalise on AI technology to identify small molecules.

JPMorgan itself is planning to increase its spend on technology to $17bn in 2024, the largest amount of money any bank has spent on technology in a single year.

Commenting on the significance of this spend, Wilson said: “The nominal dollar and the percentage increase is something I’ve never seen before in my 10 years at JPMorgan and my 20 years of working for financial services.”

A technology platform shift

It is important to note however, that despite the growing importance of technology for all industries, the big US tech companies that dominate the industry today won’t necessarily be the winners of tomorrow, according to Wilson.

“Tech leadership continues to evolve – especially when there are major platform changes,” he said. “We have a high amount of confidence that we’re in the midst of another major platform shift to AI.”

“When we’ve gone through these major platform shifts, the leadership within technology changes.”

When companies are fast evolving due to the rapid development of a new technology, Wilson suggested that being constrained by a benchmark can be a limiting factor.

He stressed the importance of looking beyond what is defined as technology by the major benchmark index providers such as Russell, S&P or Bloomberg.

“We have the flexibility to define what is tech, and importantly the benchmark that we use is an equal weighted index which also allows for flexibility in positioning,” he said.

“As a fund manager, when you have a market cap weighted index, if you don’t like a name, you still own it. If we don’t like a company, we don’t own it.”

Indeed, one of the most common technology benchmarks: the MSCI World Information Technology Index, has almost 20% allocated to Microsoft and Apple, which puts pressure on fund managers to own these large names.

On being benchmark constrained

Wilson said: “When you have benchmarks that have 10% to 20% in a single name, because leadership evolves and because we’re constantly looking for those companies that are growing, taking share, thinking differently, we can make a lot more money putting our captive capital to work.”

“You might perform really well by being underweight a big benchmark name, but you’re also locking up 4% that could go into a company that might be a double or a 10-bagger or 100-bagger.”

Despite being a technology-focused fund, Wilson pointed out that his strategy has less of the mega-cap tech names than the broader S&P 500 index.

For example, Apple and Microsoft do not feature in JP Morgan US Technology fund’s top-10, despite accounting for over 12% of the widely tracked core equity index.

“We are thinking differently and are not constrained to having to take 10% of our portfolio and allocate that towards the companies that have already won,” Wilson explained.

“The big continuing on to getting bigger won’t endure. We’re taking big bets on small, mid-cap names and with conviction.”

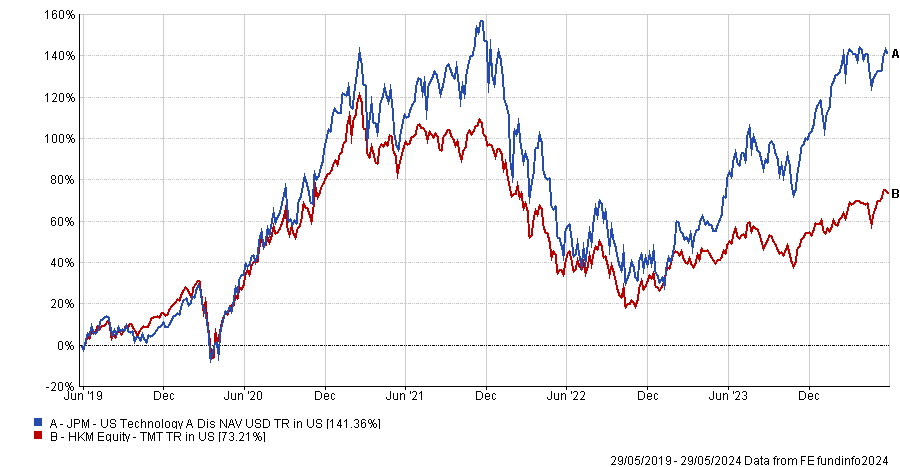

The JP Morgan US Technology fund is ranked top-quartile among its peers in Hong Kong and Singapore, with a 141.4% return over the past five years, compared with the 73% Hong Kong TMT sector average.