Small and mid-cap funds tend to fare poorly during a bear market, which should in theory mean that they are set to struggle for the foreseeable future, especially as the US Federal Reserve is still forecasting a mild recession towards the back end of 2023.

The Russell 2000 small-caps index is lagging behind the S&P 500 this year, edging up about 0.3% compared with a gain of 7% for the large-cap index as a number of small-cap ETFs have bled billions of dollars, particularly following the bank collapses in March.

However, there are many that think that there are reasons to be cheerful this time around. For one thing, valuations are a lot more attractive for small and mid-cap funds than they have been for a long time.

This is particularly true in Europe, where over the past decade a lot of money has gone into large companies like L’Oreal and LVMH, leaving behind a long tail of small and mid-cap companies that look undervalued and under-researched.

In addition, for those that seek exposure to some of the secular growth themes such as digitalisation and renewable energy, the leaders in those fields are often small and mid-cap companies.

Some market observers are drawing parallels between now and the period immediately following the dotcom bubble bursting in 2000. In the seven-year period following the market peak in March 2000, small caps were up by more than 70%, whereas large caps were up by less than 10%.

Against this backdrop, Darius McDermott, managing director at Chelsea Financial Services and FundCalibre, selected two small/mid-cap funds for comparison for this week’s head-to-head. He chose the Stewart Investors Asia Pacific Sustainability fund and the Ninety One Asia Pacific Franchise fund.

| Ninety One | Stewart Investors | |

| Size | $54.1m | $825.3m |

| Inception | 2018 | 2005 |

| Managers | Charlie Dutton | David Gait, Sashi Reddy |

| Three-year cumulative return | 1.92% | 12.07% |

| Three-year annualised return | -4.71% | 5.89% |

| Three-year annualised alpha | -4.70 | 7.55 |

| Three-year annualised volatility | 19.2% | 14.81% |

| Three-year information ratio | -0.56 | 0.67 |

| Morningstar star rating | ** | ***** |

| Morningstar analyst rating | Bronze | Silver |

| FE Crown fund rating | 2.02% | ***** |

| OCF (retail share class) | 1.06% | 0.93% |

Investment approach

“The Stewart Investors team completely ignore benchmarks and peer groups when selecting investments for their portfolio – while the sustainability name indicates the managers only invest in businesses where all stakeholders (shareholders, employees and customers) are well treated,” said McDermott.

With the team prioritising corporate governance, McDermott observes that the fund’s managers will only invest in companies where the interests of minority shareholders are respected. These requirements immediately rule out a large part of the index and many state-owned enterprises – immediately creating dispersion in returns when compared to their peers.

The fund managers’ process is bottom-up and largely ignores changes in the macroeconomic environment. Investment ideas are generated from company visits, research trips and industry contacts. They largely ignore sell-side analysts and prefer to do their own research. Valuation and price are considered at the initial point of investment. While managers are happy to pay a fair price for a business, they tend to avoid paying extremely high prices, in line with their views on capital preservation. They also avoid investing in speculative companies.

Risk is managed primarily at the stock level through investing in soundly managed, financially strong and sensibly priced companies. The portfolio is concentrated, with around 60 holdings. This is an all-cap fund so the managers are not constrained by the size of the companies they choose to include in their portfolio. From a sector perspective, the fund has typically had its largest exposures in consumer products and IT. Fund performance has been consistently excellent for a very long time; it has also been less volatile than the rest of its peer group.

“The Stewart Investors team completely ignore benchmarks and peer groups when selecting investments for their portfolio – while the sustainability name indicates the managers only invest in businesses where all stakeholders (shareholders, employees and customers) are well treated.”

Darius McDermott, Chelsea Financial Services & FundCalibre

On the other hand, the Ninety One fund, which typically holds around 30 companies, is very high conviction in nature. The fund’s emphasis is on finding exceptional businesses through detailed fundamental research. It typically ignores more cyclical and lower quality parts of the market such as energy, materials and utilities. The philosophy is that the market underappreciates the ability of high-quality companies to earn excess returns for long periods of time. These rare businesses are able to deliver consistent growth in intrinsic value.

Small companies with a market capitalisation of less than $2bn are removed, as are lower quality sectors and industries. This reduces the universe to just 300 stocks. From this list, ideas are generated from screens, internal research and external sources. The team actively covers around 100 stocks with in-depth fundamental research. From this list between 25 and 40 stocks make it into the final portfolio.

To be considered a franchise and have the chance of making it into the portfolio, a company must have the following characteristics: hard-to-replicate enduring competitive advantage; dominant market position in a stable growing industry; low sensitivity to the economic cycle; healthy balance sheets and low capital intensity; and sustainable cash generation and effective capital allocation.

The portfolio is predominately large cap, although it is both benchmark agnostic and unconstrained. The quality growth nature of the fund is reflected in a consistently high exposure to telecommunications, media and technology stocks.

The fund promotes environmental and social characteristics in line with Article 8 of the EU Sustainable Finance Disclosure Regulation. Additionally, the fund will not invest in certain sectors or investments.

Fund characteristics

Sector allocation:

| NinetyOne | Stewart Investors | ||

| Information Technology | 28.1% | Information Technology | 18.8% |

| Consumer Staples | 16.0% | Consumer Staples | 18.3% |

| Communication Services | 15.3% | Health Care | 17.8% |

| Health Care | 14.2% | Industrials | 15.5% |

| Consumer Discretionary | 13.7% | Consumer Discretionary | 13.1% |

| Financials | 9.3% | Financials | 10.0% |

| Materials | 2.8% | Communication Services | 1.2% |

| Cash | 0.6% | Cash and Cash Equivalents | 5.1% |

Top 5 holdings:

| NinetyOne | Weighting | Stewart Investors | Weighting |

| Taiwan Semiconductor Manufacturing | 9.8% | Tube Investments of India | 5.7% |

| Tencent | 8.8% | Mahindra & Mahindra | 5.3% |

| Alibaba Group | 7.6% | Unicharm Corporation | 4.5% |

| Samsung Electronics | 7.4% | CSL | 4.1% |

| Kweichow Moutai | 6.2% | Voltronic Power Technology | 3.1% |

Geographical Allocation:

| NinetyOne | Weighting | Stewart Investors | Weighting |

| China | 41.6% | India | 41.1% |

| Australia | 12.5% | Taiwan | 11.6% |

| Taiwan | 9.8% | China | 10.7% |

| United States | 9.6% | Japan | 8.8% |

| South Korea | 7.4% | Australia | 6.0% |

Performance

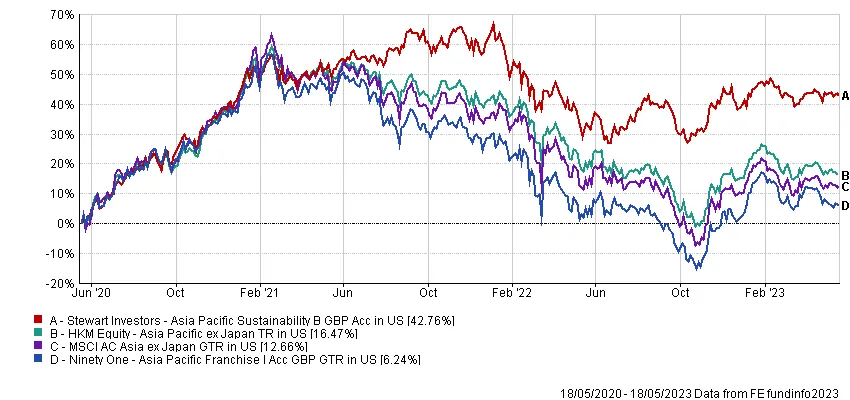

Both Stewart Investors and Ninety One are high conviction funds but operate in very different ways. Some similarities lie in the screening out of speculative, smaller businesses.

According to FE fundinfo data, the Ninety One fund generated 1.92% in terms of three-year cumulative return, while the Stewart Investors fund posted a return of 12.07% for the same period.

The Stewart Investors team is an expert in Asia and very risk averse (despite having a reasonably high conviction portfolio in terms of the number of stocks), so while the fund may not capture all the upside in a strongly rising market, it will protect on the downside. This is reflected by the fund being less volatile than its peers, notes McDermott.

Meanwhile, he points out that the Ninety One fund is arguably higher conviction in nature. Performance is also indicative of this quality growth focus, with the fund outperforming in these periods and underperforming when value is the more dominant investment style, adds McDermott.

Discrete calendar year performance

| Fund/Sector | YTD* | 2022 | 2021 | 2020 | 2019 | 2018 |

| NinetyOne | 3.61 % | -21.33% | -9.39% | 29.92% | 28.83% | – |

| Stewart Investors | 2.59% | -15.06% | 14.13% | 26.11% | 9.36% | 0.87% |

| Asia Pacific ex Japan | 1.26% | -19.04% | 0.11% | 21.83% | 18.21% | -16.05% |

Manager review

“We would have no concerns about either team. The Stewart Investors team are market leaders in Asia, with a huge team of analysts and fund managers – all of whom have demonstrated the success of their process over a number of decades,” said McDermott.

David Gait has been part of the Stewart Investors team since 1997. He has helped manage the similar Stewart Investors Asia Pacific Leaders Sustainability fund since its inception in 2015. Sashi Reddy joined Stewart Investors in 2007. He is also co-manager of the Asia Pacific Leaders Sustainability fund and the Indian Subcontinent Sustainability fund. Both have run this fund since 2019.

The Ninety One fund sits in the quality growth team, which runs a few funds at the asset manager. It is also backed by a strong team of both fund managers and research analysts.

Charlie Dutton, who runs the fund, has more than 20 years Asian equity investment experience. He began his career as an analyst with HSBC in 1997 and was subsequently head of research for Asian equities at JP Morgan. Prior to joining Ninety One, Dutton was a portfolio manager at Coupland Cardiff.

Conclusion

“I’d actually argue both can do a job in an investor’s portfolio. If you are looking for a safe pair of hands, then the Stewart Investors fund is ideal. It is quite risk averse, but the team has so much experience that it can -and will – take advantage of opportunities on the upside. The team has huge amounts of experience in navigating many different environments and has shown the investment process does stand up in any of them. This is an ideal ‘set and forget’ holding for core Asian equities exposure,” McDermott said.

Despite facing headwinds in the past couple of years, the Ninety One fund also has merit for investors, particularly if growth-style investing comes back into fashion. It is important to remember this is a quality growth fund, which dovetails nicely with the emergence of quality in Asia Pacific, in particular the healthcare, IT and consumer sectors. These are long-term trends this fund plays into so you just have to prepare for the ups and downs, cautions McDermott.