The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

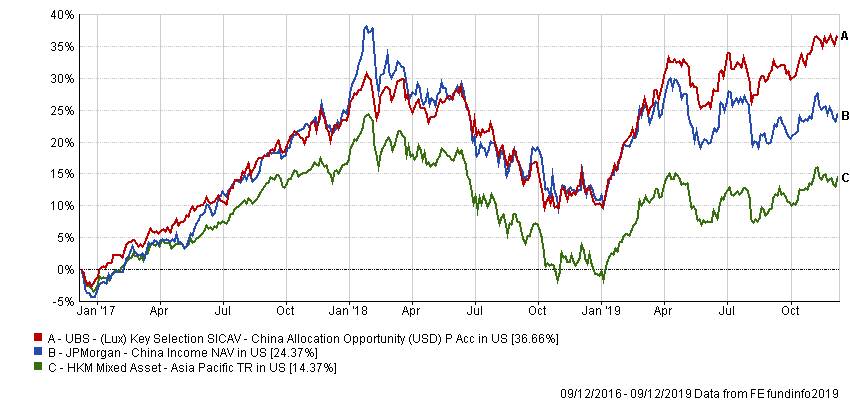

Performance

Both funds have outperformed the Asia-Pacific mixed asset category average over the past three years. The UBS product has generated a cumulative return in US dollar terms of 36.66%, the JP Morgan fund has retuned 24.37%, and the sector average just 14.37%, according to FE Fundinfo data.

“The UBS fund has been helped by an especially strong 2019, as the managers deployed its previously high cash balance into markets at the start of the year,” said Ng.

“That large cash position in 2018 also mitigated its performance during the major sell-off in risk asset markets in the second half of last year,” he added.

Consistently superior stock and bond selection has contributed to strong alpha (7.00) since 2016, well in excess of the alpha earned by the JP Morgan fund (2.62).

The JP Morgan fund’s strongest recent calendar year was 2017, “when the managers added great value with their allocation between equities and fixed income,” according to Ng.

Both funds are more volatile than the sector average of 9.91%, but that is to be expected because of their focus on China securities, rather than the wider (and less volatile) Asia-Pacific universe, he said.

Discrete annual performance % (US dollars)

|

YTD* |

2018 |

2017 |

2016 |

2015 |

2014 |

|

| JP Morgan |

11.36 |

-11.34 |

30.70 |

4.32 |

-3.56 |

34.25 |

| UBS |

23.07 |

-10.70 |

25.84 |

2.05 |

– |

– |

| Mixed Asset Apac sector |

14.65 |

-14.87 |

20.64 |

-0.50 |

-6.24 |

2.61 |

The year of living dangerously for income investors

The year of living dangerously for income investors

Driving decarbonisation: how to access new forms of alpha

Driving decarbonisation: how to access new forms of alpha

Thematic investment series: Innovative transformation cuts across “old” and “new” economy companies

Thematic investment series: Innovative transformation cuts across “old” and “new” economy companies

Impact opportunities: investing to limit biodiversity loss

Impact opportunities: investing to limit biodiversity loss

The future of mobility

The future of mobility

Exciting opportunities in AI & Robotics outside of traditional tech

Exciting opportunities in AI & Robotics outside of traditional tech

How ETFs offer an active way to drive sustainable returns

How ETFs offer an active way to drive sustainable returns

Accessing India’s tech future

Accessing India’s tech future

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.