The FSA Spy market buzz – 30 May 2025

Korean AI-driven investing, The wisdom of Nvidia, Goldman Sachs and active good news, The sheer size of the top ten, Ferris Bueller and Trump’s tariffs, A trillion here - a trillion there, and much more.

The performance of the Fidelity fund was mixed during the previous manager Angel Agudo’s tenure, according to Tsymbaluk.

“Agudo executed his approach with success in the earlier part of his term, but the strategy struggled after 2016,” she said.

“Although style headwinds explain some of the poor outcome over the period, there have also been stock selection issues,” she explained.

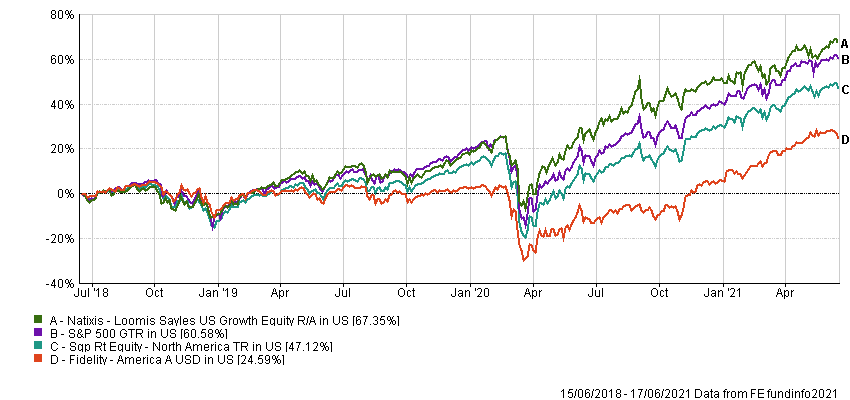

The Fidelity fund has generated a three-year cumulative return of 24.59%, underperforming both the S&P 500 (60.58%) and its North American sector peers (an average of 47.12%), according to FE Fundinfo.

In 2019, the fund lagged the Russell 1000 Value Index and peers significantly, with stock selection weak across a number of sectors, notably financials and tech. “Not holding Apple and the lack of exposure to Microsoft detracted, while TripAdvisor performed poorly amid broad-based weakness in earnings,” said Tsymbaluk.

So far this year, “the strategy is ahead of all yardsticks, benefiting from overweightings in energy and financials. Stock selection within consumer staples and tech has also been beneficial,” said Tsymbaluk.

The Fidelity fund’s volatility, as measured by standard deviation, is in line with the Russell 1000 Value index and Morningstar US Large-Cap Value Equity peers since the strategy’s inception, despite its high concentration and strong sector bets, according to Tsymbaluk.

“The Loomis Sayles fund should do well when quality growth is in favour and when wide-moat growth companies are in demand, particularly when investors are willing to pay up for the pricier ones,” said Tsymbaluk.

However, the strategy may trail in sharp up-markets – although it generally does better than its peers in downturns, she noted.

“Indeed, the strategy did hold up substantially better than all the yardsticks during the first-quarter 2020 market downturn, but didn’t participate fully in the sharp rebound,” said Tsymbaluk.

“This was in line with our expectations, given its emphasis on quality and wide moats,” she added.

The Loomis Sayles strategy ha earned a three-year cumulative return of 67.35%, beating the S&P 500 index and its category peers, according to FE Fundinfo.

Given the valuation focus here, the strategy is expected to perform well in a value, counter-cyclical environment such as the year to date and struggle in high-growth or momentum-driven market environments, such as 2019, said Tsymbaluk.

The strategy is differentiated from many other US equity offerings given its value tilt, mid-cap bias, and absence of FAANG holdings, she noted.

Moreover, despite the Loomis Sayles fund having a compact portfolio of 30-40 names, the concentration on wide-moat companies and diversification by different business drivers have kept volatility in line with the Russell 1000 Growth index and Morningstar US Large-Cap Growth Equity peers, according to Tsymbaluk

Discrete calendar year performance

| Fund/Sector |

YTD* |

2020 |

2019 |

2018 |

2017 |

2016 |

| Fidelity |

17.04% |

3.96% |

10.87% |

-6.87% |

9.44% |

9.26% |

| Loomis Sayles |

10.27% |

28.88% |

29.87% |

-3.64% |

30.90% |

– |

| Sector – North America equity |

12.30% |

16.07% |

27.84% |

-7.32% |

19.57% |

8.19% |

| S&P 500 |

13.19% |

17.75% |

30.70% |

-4.94% | 21.10% |

11.23% |

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

How can a sustainable approach also ensure you don’t compromise performance?

How can a sustainable approach also ensure you don’t compromise performance?

The year of living dangerously for income investors

The year of living dangerously for income investors

Your Questions Answered by Federated Hermes Impact Opportunities

Your Questions Answered by Federated Hermes Impact Opportunities

Impact opportunities: investing to limit biodiversity loss

Impact opportunities: investing to limit biodiversity loss

Market volatility is creating enticing opportunities for value investors

Market volatility is creating enticing opportunities for value investors

Healthcare’s innovation shifts into high gear

Healthcare’s innovation shifts into high gear

Sustainable Investing in Changing Market Conditions

Sustainable Investing in Changing Market Conditions

Federated Hermes SDG Engagement Equity: 2021 H1 Report

Federated Hermes SDG Engagement Equity: 2021 H1 Report

Riding the wave of alternative income amongst HNWIs in APAC

Riding the wave of alternative income amongst HNWIs in APAC

Korean AI-driven investing, The wisdom of Nvidia, Goldman Sachs and active good news, The sheer size of the top ten, Ferris Bueller and Trump’s tariffs, A trillion here - a trillion there, and much more.

Part of the Mark Allen Group.