It has been difficult for anyone who had dubbed this to be the “year of the bond”.

Having endured its worst year on record last year after the US Federal Reserve hiked interest rates seven times in a bid to stave off inflation, US Treasuries continued their downward trend.

The last month has been a particularly painful period for US Treasuries as fears began to crystalise that the Fed would keep interest rates higher for longer, sending yields surging to their highest level in 16 years.

There have been signs that things may be starting to stabilise following more dovish statements from the Fed and weaker-than-expected jobs data, although investors have repeatedly got burned this year from buying bonds, particularly long-dated Treasuries, on expectation of a slowdown.

In addition to the relatively robust outlook for the US economy, various other factors have conspired to keep Treasury yields elevated, which may be harder to budge.

For one thing, there is a growing expectation we are about to experience a deluge of supply as budget deficits in most Western economies are now running at record levels.

At the same time, central banks have pulled back from their pivotal role since the global financial crisis in being the buyers of last resort.

Given the fact that neither of these factors are likely to change anytime soon, it would take a brave investor to make the call that now is the time to pile into long-dated US Treasuries.

Against this backdrop, Mara Dobrescu, Morningstar’s director of fixed income ratings and global manager research, chose the Fidelity Global Bond fund and the Franklin Templeton Brandywine’s Global Opportunistic Fixed Income fund for this week’s head-to-head article.

| Fidelity | Brandywine | |

| Size | $1.41bn | $196m |

| Inception | 2006 | 2011 |

| Managers | Rick Patel, Ario Emami Nejad, Daniel Ushakov | David Hoffman, Jack McIntyre, Anujeet Sareen, Brian Kloss, Tracy Chen |

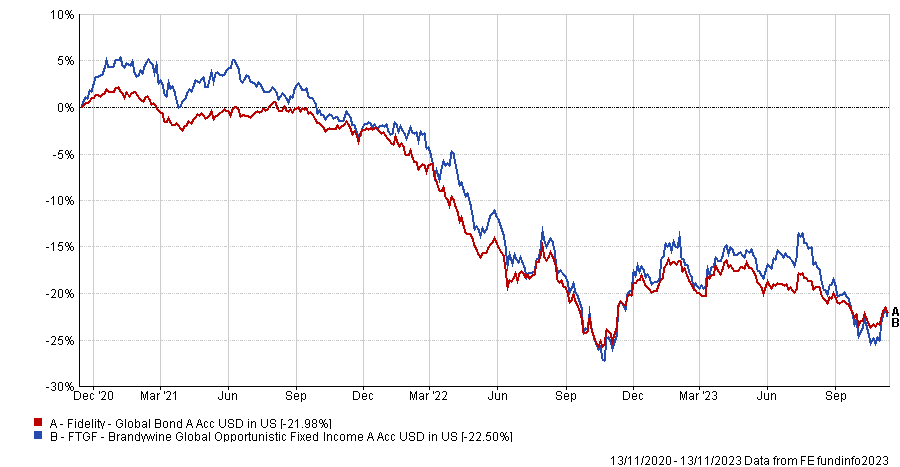

| Three-year cumulative return | -8.16% | -8.13% |

| Three-year annualised return | -7.96% | -8.14% |

| Three-year annualised alpha | -3.25 | -1.71 |

| Three-year annualised volatility | 7.11 | 10.08 |

| Three-year information ratio | -1.25 | -0.75 |

| FE Crown fund rating | * | * |

| OCF (retail share class) | 1.05% | 1.41% |

Investment approach

Dobrescu notes that both funds employ distinct philosophies. The Fidelity fund is very much focused on the benchmark, with a penchant for liquidity and high-quality holdings. Its target returns are 100bp above the Bloomberg Global Aggregate USD index, while it also aims to keep volatility to a minimum.

Dobrescu notes therefore that the strategy is “less adventurous” than its peers, with modest exposure to emerging market debt and high yield issuers, both of which account for a maximum exposure of 10 percentage points, as well as cautious currency tilts.

“The team uses US Treasury and German Bund futures to steer the portfolio’s overall duration (a measure of interest rate sensitivity), but keeps it within 1.5 years of the benchmark. While well-structured, the process hasn’t really stood out from the competition, earning it an average process pillar rating,” said Dobrescu.

Meanwhile, the Brandywine fund employs a much more active approach and has an above average process pillar rating from Morningstar.

“While well-structured, the process hasn’t really stood out from the competition, earning it an average process pillar rating.”

Mara Dobrescu, director, fixed income ratings, global manager research, morningstar

“This fund’s managers argue that issuance-weighted global-bond indexes, which emphasise developed-markets countries with the heaviest debt burdens, are inherently flawed,” said Dobrescu.

“Instead, they employ macroeconomic and valuation analysis to identify countries with attractive real yields (which should suppress inflation), find advantageous spots along markets’ maturity spectra and pinpoint undervalued currencies that can benefit from supportive economic trends.”

As a result, the strategy has generally eschewed Japanese government bonds, even though they make up around a quarter to a third of the FTSE World Global Bond Index, whereas it has significant exposure to emerging market debt.

Dobrescu also notes that the strategy has higher exposure to corporate debt and securitised sectors compared with the benchmark, while duration management is also more flexible.

Fund characteristics

Country allocation:

| Fidelity | Brandywine | ||

| USA | 42.32% | USA | 49.05% |

| UK | 12.62% | UK | 2.86% |

| Germany & Austria | 10.64% | Mexico | 2.81% |

| Asia ex-Japan, ex-Australia | 8.91% | Colombia | 6.05% |

| Australia & New Zealand | 4.34% | South Africa | 4.86% |

| France | 3.19% | Brazil | 4.21% |

| Benelux | 1.98% | Germany | 3.11% |

| Mediterranean | 1.92% | Australia | 3.08% |

| Canada | 1.71% | Norway | 3.06% |

| Scandinavia | 1.71% | New Zealand | 0.76% |

| Latin America | 1.66% | ||

| Japan | 1.22% | ||

| CIS/Eastern Europe | 0.93% | ||

| Middle East & North Africa | 0.76% | ||

| Switzerland | 0.55% | ||

| Multinational | 0.36% | ||

| Cash | 5.42% |

Sector allocation:

| Fidelity | Brandywine | ||

| Treasuries | 64.14% | Treasuries | 39.4% |

| Banks & Brokers | 15.75% | Agency Mortgage-Backed | 6.9% |

| Consumer Non-Cyclical | 3.71% | Corporate Bonds | 0.5% |

| Consumer Cyclical | 2.02% | Cash | 0.8% |

| Insurance | 1.53% | ||

| Other Financials | 1.39% | ||

| Communications | 1.22% | ||

| Sovereign/Supra/Agency | 0.97% | ||

| Utility | 0.93% | ||

| Technology | 0.87% | ||

| Property | 0.65% | ||

| Energy | 0.61% | ||

| Capital Goods | 0.56% | ||

| Basic Industry | 0.49% | ||

| Cash | 5.42% |

Top five holdings:

| Fidelity | Brandywine | ||

| US Treasuries | 31.37% | US Treasuries | 42.17% |

| People’s Republic of China | 6.99% | Government of Japan | 24.01% |

| Germany Government 2.3% | 6% | EU | 13.84% |

| United Kingdom | 5.69% | US Treasury Notes 3.5% | 12.79% |

| Germany Government | 2.55% | United Kingdom | 6.95% |

Performance

Unsurprisingly, given its conservative nature, the Fidelity fund tends to fare better during risk-off periods, although the downside is that it misses out on some of the upside during credit rallies.

Dobrescu notes that the fund emerged from the coronavirus crisis sell-off in March 2020 largely intact, given around two-thirds of the fund was invested in triple-A bonds and cash, although it has been caught out recently by the interest rate hiking cycle as the fund keeps duration close to the benchmark.

“As a result, the strategy underperformed in 2022. Overall, though, the fund’s long-term risk -adjusted record is sound: it has outpaced 65% of its competitors over five years through October 2023, while keeping volatility in check,” said Dobrescu.

Meanwhile, the Brandywine fund’s performance is in stark contrast, although Dobrescu notes that the managers’ contrarian calls and willingness to hold beaten-down bonds and currencies are not for the faint-hearted.

“For example, the strategy’s focus on emerging-markets debt and currencies coupled with light exposure to the US dollar hampered its performance during 2020’s first-quarter coronavirus sell-off as investors ran away from riskier debt,” said Dobrescu.

“However, the portfolio’s significant addition to beaten-down investment-grade corporate credit and heavier position in emerging-markets debt in the ensuing months helped the strategy bounce back and end 2020 ahead of 80% of its peers.”

This year has been a bit more of a struggle for the fund due to its bet on duration along with its overweight towards the Japanese yen, albeit this was partially offset by its investment in emerging market sovereigns as well as various Latin American currencies.

“This feast-or-famine return profile is a reminder that this strategy is best suited for long-term investors who have a higher risk appetite for volatility,” said Dobrescu.

Discrete calendar year performance

| Fund | YTD* | 2022 | 2021 | 2020 | 2019 |

| Fidelity | -2.84% | -17.51% | -4.71% | 12.02% | 7.15% |

| Brandywine | -4.58% | -17.3% | -6.67% | 10.19% | 7.95% |

Manager review

The Fidelity fund is led by Rick Patel alongside co-portfolio managers Ario Emami Nejad and Daniel Ushakov. Patel is a Fidelity veteran having been with the investment manager since 2000 and he began managing this strategy in 2016.

Dobrescu notes that the trio are supported by a strong bench of research analysts, comprising 42 credit analysts with six years of tenure at the firm and 15 years of industry experience.

The strategy also draws on additional insights from the macro and trading teams, five quantitative research analysts and the three portfolio managers on the core investment-grade bench.

Meanwhile, Dobrescu singles out the Brandywine strategy for its “seasoned leadership, careful succession planning and a strong supporting cohort”.

David Hoffman, who has overseen Brandywine’s global fixed-income strategies since the 1990s, has managed this strategy since its 2006 launch.

“Given Smith’s and Hoffman’s decades of experience, they built a solid succession plan for their eventual retirements.”

Mara Dobrescu, director, fixed income ratings, global manager research, morningstar

Jack McIntyre, who has also been with the firm since the late 1990s, became co-manager in 2012, while Steve Smith, who Dobrescu describes as the architect behind the strategy, transitioned into an advisory role at the end of 2020.

“Given Smith’s and Hoffman’s decades of experience, they built a solid succession plan for their eventual retirements,” said Dobrescu.

In May 2016, they brought on board Anujeet Sareen from Wellington, while in 2021, Brian Kloss and Tracy Chen, who have both been at the firm for more than 10 years, were appointed co-managers.

The firm also draws on the talents of a group of dedicated research analysts, averaging 16 years of experience, as well as a securitised analyst and a group of traders and portfolio implementation specialists.

Conclusion

When asked which fund she prefers, Dobrescu suggests that the Brandywine strategy has a slight edge because of its superior investment process.

“While both strategies boast experienced skippers and strong supporting resources (as reflected by their above average people pillar ratings), the Brandywine strategy offers, in our opinion, a superior investment process (rated above average) to Fidelity’s (rated average),” she said.