2022 has been a volatile year for most asset class, especially for European bonds given the acute economic stress facing the region as a result of the growing energy crisis and uncertain outcome of the Russia-Ukraine war.

With no signs of inflation ebbing, European bond investors are becoming more defensive as they brace for volatility to continue through the coming months.

Speaking to FSA in a prior interview, Xueming Song, currency strategist at DWS recommended investors reallocate from European bonds to US bonds.

However, despite the high volatility, European company earnings have remained strong.

In the third quarter this year, earnings are expected to increase 31.3% year-over-year, according to a Reuters report.

More than 55% of the companies that had reported earnings beat analysts’ profit estimates, as per Refinitiv IBES data.

The rally is expected to continue into 2023 but at a slower pace, with an estimated earnings growth of 18.6% in the fourth quarter and 3% in the first quarter of 2023.

Against this backdrop, FSA asked Florence Savage, investment analyst at Oreana Financial Services, to select two European fixed income funds for comparison. She chose the BlackRock Euro Corporate Bond Fund and the Morgan Stanley Euro Corporate Bond Fund.

| BlackRock | Morgan Stanley | |

| Size | $2.68bn | $2.43bn |

| Inception | 2003 | 2001 |

| Managers | Tom Mondelaers, Georgie Merson | Leon Grenyer, Richard Ford, Dipen Patel |

| Three-year cumulative return | -9.26% | -8.77% |

| Three-year annualised return | -6.65% | -6.10% |

| Three-year annualised alpha | 0.18 | 0.43 |

| Three-year annualised volatility | 12.90% | 12.25% |

| Three-year information ratio | -0.30 | -0.11 |

| Morningstar star rating | *** | **** |

| Morningstar analyst rating | Bronze | Neutral |

| FE Crown fund rating | ** | *** |

| OCF (retail share class) | 1.02% | 1.04% |

Investment approach

The BlackRock and Morgan Stanley funds were launched in 2003 and 2001 respectively.

Both funds start with top-down analysis in order to identify key themes based on the macro environment as well as market and credit trends.

In Morgan Stanley’s case, it looks at key macro themes to determine the credit risk and duration and then analysts conduct deep credit research to identify the appropriate securities.

“It doesn’t deviate too far from the Bloomberg Euro Aggregate Corporate Bond Index benchmark, resulting in financials typically representing over 40% in the portfolio,” said Savage.

The fund also has a value bias with over 60% of its holdings rated triple-B.

Morningstar analysts also noted that at the issuer level, the credit analysts consider the company’s financial and business risk, valuation and the bonds’ position within the capital structure, covenants and maturity.

The fund also has a 5% internal limit on high-yield bonds, primarily for downgrades rather than purchases, and its currency exposure is largely hedged back to the euro.

“It doesn’t deviate too far from the Bloomberg Euro Aggregate Corporate Bond Index benchmark, resulting in financials typically representing over 40% in the portfolio.”

Florence Savage, investment analyst, Oreana Financial Services

In contrast, BlackRock has a quality tilt in its portfolio and underweights highly cyclical sectors.

Over 42% of its portfolio is invested in bonds rated triple-A to A, compared with 34% for the Morgan Stanley fund.

“BlackRock focuses on security selection and sector allocation, combining traditional fixed income exposures with security, sector, country and yield curve relative value strategies. They typically implement 40-60 active bets out of the 350 or so holdings,” said Savage.

Morningstar analysts wrote in their report that the BlackRock managers seek to construct a diversified portfolio so that no single factor dominates the risk profile.

While the sector specialist teams provide top-down sector and bottom-up issue-specific analysis, the managers retain final discretion over all positions and their sizing, the report noted.

The fund usually allocates about 10% of its net asset value to government bonds and can also own up to 10% in high yield bonds and 10% non-euro currency exposure.

Sector allocation

| BlackRock | Morgan Stanley | ||

| Financial Institutions | 43.68% | Corporates financial institutions | 49.02% |

| Industrial | 33.83% | Corporates industrial | 30.42% |

| Utility | 10.19% | Government related | 10.14% |

| Cash and/or derivatives | 4.83% | Corporates utility | 9.92% |

| Agency | 3.80% | Cash and equivalents | 0.85% |

| Local authority | 1.57% | Interest rate swaps | -0.35% |

| ETFs | 1.09% | ||

| Covered | 0.61% | ||

| ABS | 0.29% | ||

| Government | 0.10% | ||

| CMBS | 0.01% |

Geographical allocation

| BlackRock | Morgan Stanley | ||

| United States | 14.68% | United States | 15.12% |

| France | 14.49% | France | 12.81% |

| Germany | 12.57% | Germany | 9.67% |

| United Kingdom | 12.14% | United Kingdom | 8.32% |

| Italy | 7.35% | Australia | 7.07% |

| Switzerland | 7.15% | Spain | 6.88% |

| Cash and/or derivatives | 4.83% | Netherlands | 6.53% |

| Netherlands | 4.50% | Italy | 6.09% |

| Spain | 4.01% | Luxembourg | 4.45% |

| Ireland | 2.91% | Other | 21.27% |

| Cash | 1.78% |

Credit ratings

| BlackRock | Morgan Stanley | ||

| AAA | 0.72% | AA | 4.13% |

| AA | 6.04% | A | 30.35% |

| A | 36.07% | BBB | 60.03% |

| BBB | 45.50% | BB | 2.13% |

| BB | 3.62% | CCC | 0.09% |

| Not rated | 2.13% | Not rated | 1.48% |

| Other | 1.09% | Cash | 1.78% |

| Cash | 4.83% |

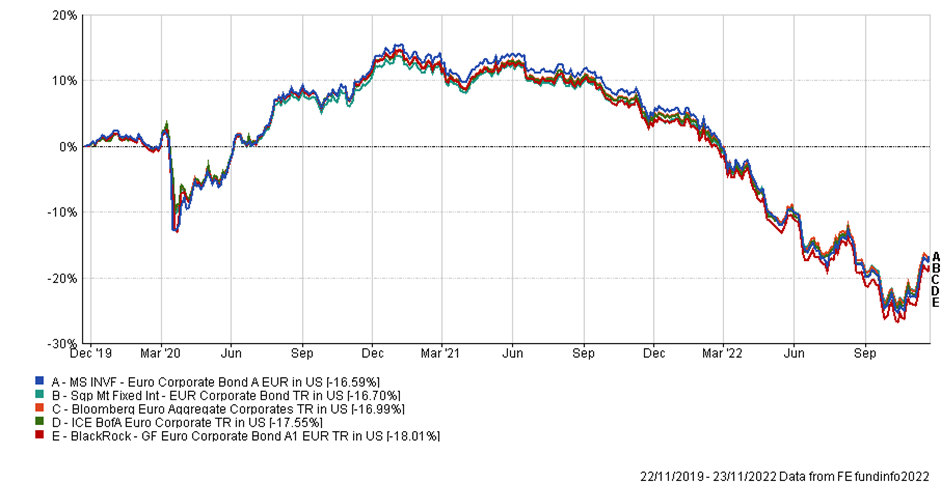

Performance

Both funds have generally performed well under the current managers, with the BlackRock fund generating an 11.79% return in 2020, while the Morgan Stanley fund generated 12.17%, both higher than the benchmark return of 11.08%

“They both weathered Covid well but have struggled to perform in the challenging macro environment since,” said Savage.

“The performance of the funds has averaged out quite similarly, with this year’s drawdowns pushing the historical averages into negative territory both on an absolute basis and marginally below the benchmark.”

In 2021, the two funds diverged as Morgan Stanley’s credit selection contributed alpha, and a specific short position detracted for BlackRock, Savage noted.

The two funds have suffered greatly this year, with the BlackRock fund posting a -22.16% return year to date, while the Morgan Stanley fund generated a -22.10% return over the same period.

“Morgan Stanley’s overweight in financials has been a key detractor this year, although the theme has started to add value in recent months. BlackRock also suffered in the first half of the year as corporate credit banks, consumer sectors, corporate hybrids in utilities and covered bonds detracted,” noted Savage.

With rapidly rising inflation, tighter market liquidity and war between Russia and Ukraine, she also noted that it has been challenging for managers to navigate through the European fixed income space.

Discrete calendar year performance

| Fund/Sector | YTD* | 2021 | 2020 | 2019 | 2018 | 2017 |

| BlackRock | -22.16% | -8.77% | 11.79% | 4.79% | -6.38% | 16.76% |

| Morgan Stanley | -22.10% | -7.80% | 12.17% | 6.13% | -8.31% | 18.45% |

| Mixed assets – international | -20.47% | -7.97% | 11.08% | 3.66% | -7.31% | 15.64% |

Manager review

Both funds benefit from their large parent groups and the research capabilities that come with it.

The BlackRock fund is co-managed by Tom Mondelaers and Georgie Merson, who have been managing the fund since 2009 and 2021 respectively.

“BlackRock has a huge range of investment resources that support the portfolio managers. Its team is made up of 17 investment professionals including 10 portfolio managers,” said Savage.

“The managers are able to leverage BlackRock’s fixed income platform, BlackRock Investment Institute and BlackRock solutions, as well as the company’s world-class Aladdin software for risk and portfolio management.”

Merson was only appointed co-manager a year ago after Jozef Prokes, who was the co-manager since January 2015, left the firm in June 2021.

Nonetheless, Morningstar believes that did not have an impact on the fund’s strategy as Mondelaers remains in place as ultimate decision-maker and the strategy is managed through a team-oriented process.

“BlackRock has a huge range of investment resources that support the portfolio managers. Its team is made up of 17 investment professionals including 10 portfolio managers,”

Florence Savage, investment analyst, Oreana Financial Services

The Morgan Stanley fund is managed by Richard Ford, head of global investment grade credit at the firm. Ford joined the group in 1991 and took over the lead manager role of the fund in 2008. He is backed by Leon Grenyer, who has worked with Ford for over 20 years at MSIM, and Dipen Patel, who was added as co-manager in 2019.

The managers are supported by around 50 analysts across sectors and credit qualities.

“While Morgan Stanley Investment Management also provides world-class investment resources, it still remains to be seen how much value the acquisition of Eaton Vance in 2021 can add to the investment process,” said Savage.

“The merger increases the companies’ combined reach and assets, but there are concerns over duplication of mandates, where funds have not yet been integrated. This could also be a concern in terms of research capabilities, where teams may not yet be entirely efficiently blended.”

Fees

The ongoing charge for the BlackRock fund is 1.02%, while the fees for the Morgan Stanley fund are 1.04%.

Savage noted that both funds are ranked in Morningstar’s most expensive quintile.

“This is appropriate given the stature of the fund houses but may make it challenging to retain alpha in the current uncertain macroenvironment,” she said.

After taking into account the funds’ people, process and parent pillars, Morningstar believes the BlackRock fund will be able to deliver positive alpha relative to the category’s benchmark index, while the Morgan Stanley fund is less likely to do so.

Conclusion

Morningstar has awarded the BlackRock product three stars based on historical returns and a forward-looking analyst rating of silver as it noted that the fund’s fees are above average compared with similar share classes.

Meanwhile, it assigns four stars to the Morgan Stanley fund with a analyst rating of neutral due to the experience of its management team, the disciplined investment process and the depth and quality of the available group-wide resources.

FE Fundinfo, which bases its assessment on a fund’s three-year history of delivering alpha, minimising relative volatility and producing consistent returns, awards the BlackRock fund two crowns, but three crowns to the Morgan Stanley fund.

When being asked which fund is better, Savage slightly favoured the BlackRock fund due to its focus on high-quality bonds.

“We expect market volatility to continue into 2023. Europe is particularly vulnerable to recession given pre-existing structural concerns of the EU and eurozone and the more recent environment,” she said.

“That leaves [the BlackRock fund] less vulnerable to downgrades in an economic downturn, while also being able to access decent yields compared to recent history.”