The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

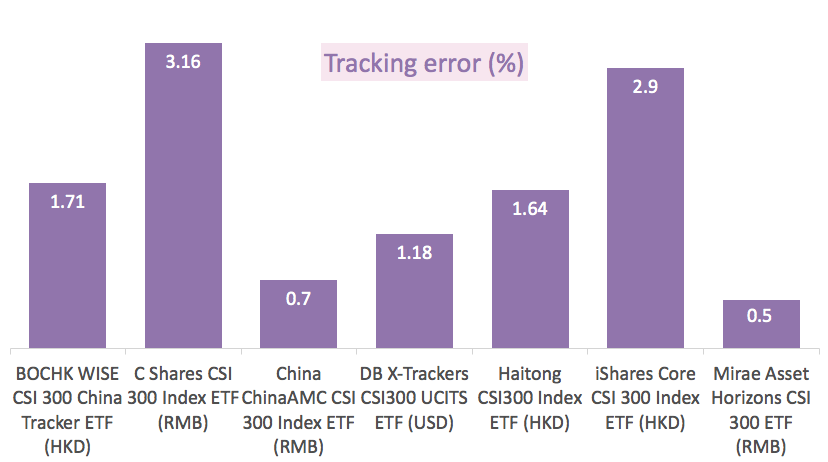

Data: FE, 30 November 2017.

While the tracking error is a commonly accepted way to measure how well an ETF tracks the underlying index, it is important to understand what it means. In particular, it is important to differentiate it from the tracking difference.

Tracking difference measures daily deviations in returns between the ETF and the index.

Tracking error, in turn, is calculated as the standard deviation (volatility) of these daily tracking differences.

“If the fund underperforms the index by exactly the same percentage every day, there would be no tracking error,” Choy said.

In order to better judge the ETF’s performance, both the tracking error and the tracking difference should be taken into account.

While the tracking difference values for the seven ETFs are not available in FE, they can be estimated by comparing the fund’s returns with those of the index, after taking into account the fees.

Tap into Japan’s post-pandemic growth trends

Tap into Japan’s post-pandemic growth trends

Turning environmental hopes into investment reality

Turning environmental hopes into investment reality

Taking a thematic approach to harness disruption

Taking a thematic approach to harness disruption

Your Questions Answered by Federated Hermes Impact Opportunities

Your Questions Answered by Federated Hermes Impact Opportunities

Accessing India’s tech future

Accessing India’s tech future

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Market volatility is creating enticing opportunities for value investors

Market volatility is creating enticing opportunities for value investors

The future of mobility

The future of mobility

Tech WELLcovered | Work reimagined

Tech WELLcovered | Work reimagined

Impact opportunities: investing to limit biodiversity loss

Impact opportunities: investing to limit biodiversity loss

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.