Even after a recent sharp rally, Daniel Fitzgerald, portfolio manager for real assets at Martin Currie Australia, an affiliate of Franklin Templeton, still reckons that the opportunities in listed real estate look more compelling than private markets.

“There’s probably three things I’d call out,” he said. “One is liquidity. For listed products, you can get your money out in two days. Unlisted can be gated and it can take you months, if not years, to get your money out.”

“The second is daily pricing. So obviously you have full transparency of what your assets are worth, whereas for unlisted, you’re relying on quarterly or half-yearly valuation reports to come through.”

“And finally, is diversification. A lot of REITs, for example, have hundreds or thousands of assets. That’s quite different to what you’d get in an unlisted product, where you might have five or 10.”

Listed real estate has endured a torrid couple of years triggered by higher interest rates. According to research from Morningstar published earlier this month, during the trailing one-year period, the Morningstar US Real Estate Index has returned -1.14% compared with a 24.28% return for the Morningstar US Market Index.

As a result, asset allocators have been arguing that listed property now looks attractively priced on a range of metrics including price-to-book, historical yield and implied cap rates, especially when compared with unlisted.

Data on unlisted real estate is harder to come by, although anecdotally, valuations for some direct and private market funds have actually risen since the Fed began its aggressive interest rate hike cycling.

Explanations for the discrepancy include the slower-moving price discovery among private market funds as well as the fact that listed real estate tends to be more highly leveraged, making the sector more sensitive to interest rate shifts.

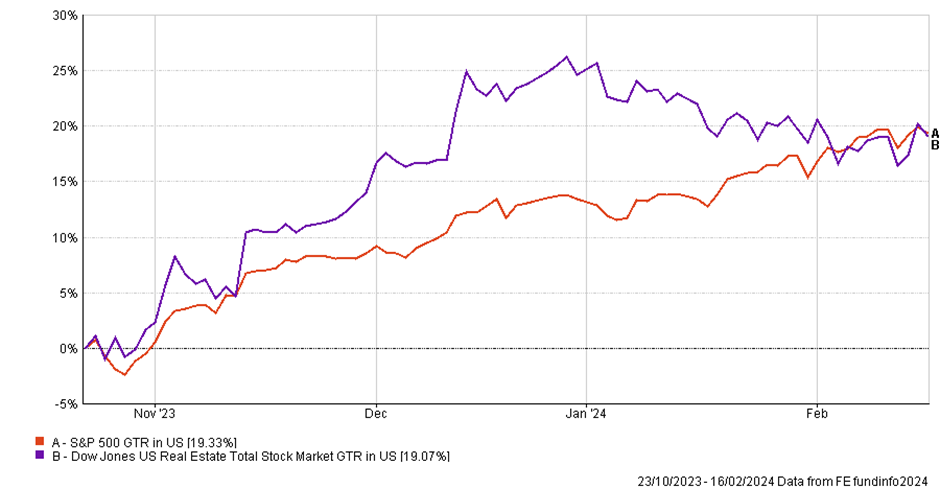

The last few months have suggested that this strategy of allocating to listed real estate rather than private markets might be starting to bear fruit. The Dow Jones US Real Estate Index has rallied almost as much as the S&P 500 since the US 10-year Treasury yield hit 5% on 23 October.

In fact, the Dow Jones US Real Estate index had outstripped even the S&P 500 until earlier this month when expectations for rate cuts shifted following a stronger-than-expected US inflation print (see chart).

Fitzgerald (pictured) thinks that this rally has further to run.

“What you’ve tended to see historically is that when performance troughs for listed versus unlisted, listed outperforms for the next four quarters so we think there’s more to go given that performance trough and the outlook for REITs,” he said.

Fitzgerald is co-portfolio manager for the Asia Pacific Urban Trends Income strategy as well as lead portfolio manager for the Global Real Income strategy.

Both strategies do not just hold property but also infrastructure and utilities too, meaning that there is less concentration risk and less bond beta in the portfolio.

Still, Fitzgerald holds some punchy views when it comes to listed real estate too. When it comes to commercial real estate, Fitzgerald is selective, favouring some markets such as India, and eschewing others, such as Singapore.

Overall, he makes the point that office property has shrunk meaningfully as a sector over the past decade or so, meaning that it less significant to the wider sector than how it is portrayed in the media.

“If you look at the US market for example, office is now less than 5% of the overall REIT market, which I think is quite surprising for a lot of people because it captures so much attention,” he said.

“Will there be more difficulties in the sector? Yes, I think absolutely. But I think it’s going to be not in all markets, just in some markets and probably more in those markets where you see more of those work-from-home issues. So, markets like Australia, the US, the UK, for example.”

Both strategies invest across a number of key megatrends, the most important of which is urbanisation, although this yields some surprising results.

Both strategies are invested in China despite the demographic headwinds there, with Fitzgerald pointing out that despite the forecast drop in population across the country, tier one cities like Shanghai, Shenzhen and Guangzhou are still experiencing rapid growth.

In contrast, both strategies eschew Japan altogether for the same reason as the population of its major cities is declining or stagnating. This is despite the fact that investors are starting to pay attention to the country again as the outlook for interest rates and inflation is at an inflection point.

In terms of sectors, Fitzgerald favours discretionary retail, particularly suburban mall assets because the demand tends to be quite steady.

He also favours industrials, pointing out that even though valuations are quite stretched, there are attractive supply-demand dynamics.