Abrdn is planning on launching an Asian version of its Global Dynamic Dividend fund by mid-year as the UK-headquartered asset manager makes income one of its three main areas of focus, the firm’s Asia Pacific head of wholesale, David Hanzl (pictured), told FSA during a recent interview.

Abrdn has endured a rocky few years, characterised by cutbacks, share price underperformance and PR issues, which culminated in the departure of CEO Stephen Bird last week (The interview with Hanzl took place the day before the announcement was made).

Hanzl singled out income along with ESG and emerging markets as the main areas of focus that would allow Abrdn to stand out from its peers and also help address some of the problems, notably outflows, that have afflicted it in every year since the merger.

“The industry has changed quite a bit over the past couple of years. On the one hand, you have more of a focus on passives. And on the other side of the spectrum, you have the growth of private markets,” he said.

“For any asset manager that is more traditional, it is absolutely critical that you find your way in this new world. It is clear to us that we want to be perceived on the outside by a couple of specialties. We are mid-sized so we are not a supermarket. We cannot be everything to everyone but we can be a lot of things to a lot of people.”

“We focus on income because I think that’s a theme that’s here to stay. We focus on where our heritage is in Asia and emerging markets, particularly China. Sustainability is another angle that we want to be known for.”

Income focus

It is clear that income in particular is front and centre of what Abrdn is trying to achieve in Asia. Indeed, Hanzl, who played football at a reasonable level (“the fourth tier of Swiss football, but nothing professional”), posted a video a few months ago on LinkedIn showing off his skills in front of an advertisement in Hong Kong’s Central MTR station featuring Abrdn’s various income products.

Only last month, Abrdn also launched an emerging markets equity income strategy, which mirrors the strategy of a UK domiciled vehicle, while in February last year, it launched its Asian high-yield sustainable bond fund.

When queried about why the reason for the focus on income, Hanzl is nonplussed, stating that he could “probably list 10 reasons”, although he singles out reforms to pension systems, which has left investors more in need for regular income streams, as the primary reason, along with the “psychological” appeal of income to Asian investors.

Based on his reading of the tea leaves, launching an Asian version of the Global Dynamic Dividend fund is a no-brainer, helped by the fact that the fund has been a relatively strong performer ever since its launch in October 2020.

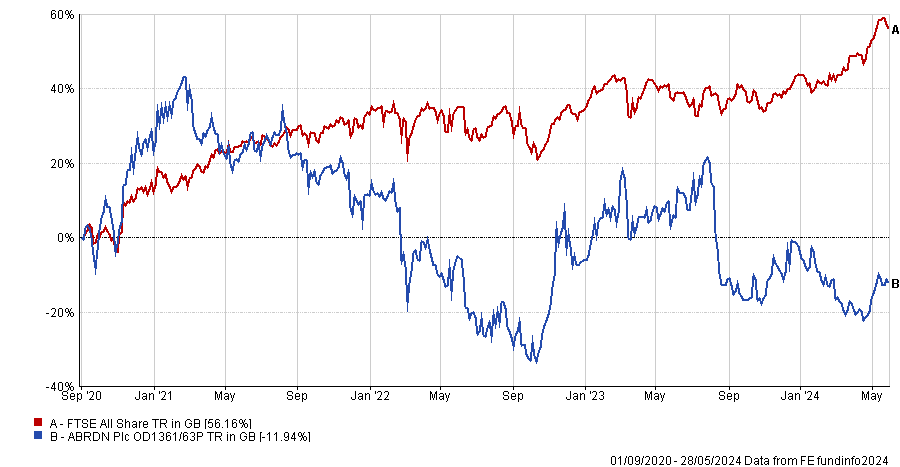

The fund, which invests 95% of the portfolio in traditional buy-and-hold stocks and the remaining 5% in a dividend capture sleeve, which is used to tactically rotate into dividend events to generate extra yield, has been a second quartile fund since its launch, according to FE fundinfo data (see chart).

“We basically said look, we are specialists in Asia. We feel that Asia has been a bit neglected, the same as emerging markets, by investors. So we take the same strategy, which has been successful, but apply it to the Asian market,” said Hanzl.

More controversial

If the decision to focus on income is relatively straightforward, especially during a period when interest rates are likely to begin falling, the focus on ESG and emerging markets is more controversial given the lack of appeal of both recently to investors.

According to Morningstar, global sustainable funds saw their first ever quarter of outflows in the last three months of 2023 after a difficult year in which they missed out on some of the upside from the rally in the Magnificent Seven due to the exclusion of a number of the stocks following ESG controversies.

Anecdotally, ESG funds are much less in vogue among investors than they were in 2020 and 2021, having initially lost their appeal in 2022 during the sell-off in growth stocks and when they failed to capture the upside from the oil price rally that year.

Equally, emerging markets stocks, which are heavily skewed towards China, have hardly been flavour of the month lately either even with the recent rally in China, although there are bright spots, notably in India, Taiwan and Korea.

Hanzl is unperturbed, pointing to long-term megatrends that are supportive for both sustainability and emerging market growth, although he concedes that at least in relation to ESG, more needs to be done to convince investors.

“As an industry in Asia in particular, we probably need to do more on education. I think for many it has been perceived as a nice to have, but we see it internally as an added value and source of alpha,” he said.

“What we have seen maybe a year ago or a year and a half ago is a lot of banks tried to build their shelves with sustainability products, but this was more driven out of their headquarters, rather than bottom-up clients.”

“But we are a client-led organisation and in Europe specifically, the demand is there for that. And very often you see a couple of years later, these trends will pick up in other parts of the world.”

Recent travails

The backdrop for Abrdn’s Asia strategy is of course the wider difficulties in the group. Analysts argue that the turnaround under outgoing CEO Stephen Bird, who was brought in following the difficulties experienced after the merger between Standard Life and Aberdeen Asset Management, has floundered with its share price down significantly during his tenure (see chart).

For any of the criticisms that may be levelled at Bird, nobody can accuse him of a lack of endeavour as he has overseen several rounds of cost cutting, more than 250 fund closures or mergers and a rebranding, which saw Abrdn shed the vowels from its name, albeit one that has been widely ridiculed.

The most recent round of cuts was announced in January, which will see the firm slash £150m ($191.3m) of costs by the end of 2025. Hanzl was quick to point out that these cost savings initiatives only impacted Asia “marginally” and why they were part of a right-sizing that was necessary across the industry.

“These cost saving programmes are fairly standard in the industry and a lot of our competitors have announced these cost programmes on a different scale. I think it’s a healthy thing to do because for the last two years the entire asset management industry has gone through a bit of a rough patch with AUMs declining, which normally means less fees for the asset managers,” he said.

The concern though is it is not just a high cost base that is plaguing Abrdn (and Bird has consistently failed to hit his cost-to-income target of 70%), but also underperformance of most of its funds. The firm disclosed that 42% of its AUM failed to beat its benchmark over the past three years, which in turn impacts flows.

Hanzl attributes this to the firm’s overweight to China and the fact that last year’s reopening rally fizzled out, although he noted that given the discrepancy in valuations between emerging markets and the US, there is a chance this can be reversed.

He also said that this was in part due to the firm’s focus on quality, which was out of favour last year. Moreover, he noted that this was a problem primarily with its equity funds as its fixed-income funds fared better.

Diversification

One of the key strengths of Abrdn under Bird has been its diversification. The former Citibank executive has consciously tried to diversify away from asset management (indeed, there were even rumours he had mooted selling the business), which has obviously been afflicted by a number of secular headwinds such as the rise of passive investment and higher regulatory costs.

The group is split into three different businesses, or vectors, namely investments, essentially its asset management business, its adviser business, and interactive investor, its direct-to-consumer business, which it acquired in 2022 for £1.5bn in the biggest spending splurge under Bird’s watch.

Hanzl was quick to point out that this diversification helped offset some of the difficulties in its asset management business. There is evidence to support this as well as adjusted profit fell 5% last year to £249m, albeit a weaker performance in asset management was offset by increased profitability from both the adviser business and interactive investor.

But assuming there is no break-up of the group, for Abrdn’s share price to perform better, it requires its asset management business to perform better. For its asset management business to perform better, it requires, unsurprisingly, investors to be willing to give it more money.

There is no obvious secret to this as the firm is competing for the same business as many of its other mid-tier rivals, although a lot of Abrdn’s success hinges on whether its unique brand of emerging market funds come back in fashion or not, as well as to a lesser extent whether its focus on income and ESG pays off.

“Hopefully, it’s our time to shine. I think we have a lot of good things going for us. Hopefully, if the markets are focused less on the US in the coming years, we have strategies in place that would be fitting that,” said Hanzl.