Tai Hui, JP Morgan Asset Management

The US should experience a strong economic recovery and re-opening later in 2021 as a result of strong fiscal stimulus by the government and the progress in vaccination rollout which will reduce lockdown measures.

The flipside is the prospect of higher inflation, as the surge in US Treasury yields this year indicates, as investors factor in future interest rates hikes to contain price pressures.

“However, in this case, rising yields are an indication of a strengthening economic picture,” Tai Hui, Asia chief market strategist at JPMAM, told a media briefing on Thursday.

“Historically, if we look at past inflation cycles, typically we see that equities, corporate credit and emerging market debt tend to perform best in this environment,” said Hui.

“Our core view on asset allocation remains therefore that we prefer equities over fixed income, we like emerging market debt and also favour high yield corporate credit over government bonds,” he said.

However, the US and global economies are a long way from over-heating, so the outlook for equities is positive.

“Rising yields in the short-term don’t have to threaten equities,” said Hui.

“In fact, when bond yields are rising from low levels, equity market performance tends to be positive. That’s reflective of the negative correlation between equities and government bonds,” he said.

Indeed, as inflation has started to pick up, corporate pricing power is improving, which tends to help earnings per share, according to Hui.

“That’s particularly important right, now given equity valuations are above average, so we can’t rely on valuation re-ratings to deliver performance. Instead, we need actual earnings growth,” he said.

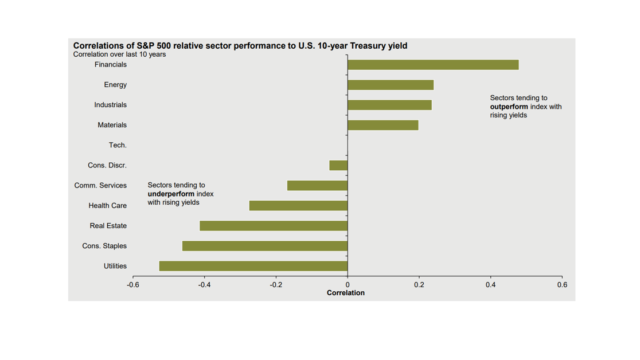

Hui noted that financials, energy and industrials sectors tend to outperform in rising rate environments: banks benefit from rising net interest margins, for example.

“So, when we talk about equities, it’s no longer just the high growth tech sector, but the rotation to more cyclical sectors that will be a major theme as the value rally continues in 2021,” said Hui.

In terms of countries, US and China are JPMAM’s core strategic allocation priorities, but investors will need to diversify portfolios as the economic recovery progresses in other regions, including Europe.

AVOID GOVERNMENT BONDS

Although he expects strong short-term headline inflation figures in coming months, Hui thinks it is unlikely that a spike in consumer prices is sustainable beyond next year, which underpins the US Federal Reserve’s commitment to low interest rates until 2023.

Year-on-year base effects for inflation data, a pullback in commodity prices after the recent surge, a lag before an improved employment outlook induces wage rises, and continued (albeit on smaller scale) asset purchases by the Federal Reserve will likely combine to pull back headline inflation from any transient spikes, argued Hui.

But, rising bond yields will continue to create challenges for fixed income investors and have significant asset allocation implications.

The challenge for fixed income is that yields are still low and don’t compensate for the risks of extending duration, according to Hui.

An increase of 50 basis points in the real yield of the 10-year US Treasury would equate to approximately a 4% reduction in bond prices.

“It’s hard to justify holding government bonds today, so we think investors should reduce duration and focus on higher yielding corporate credit, where the income component will offset the duration risk,” said Hui.