HOW HAS HIGH YIELD PERFORMED THROUGH THE COVID-19 CRISIS?

High yield markets are sensitive to economic activity, so as you’d expect during the pandemic crisis, prices fell and spreads widened significantly. Since March, we’ve then seen a retracement in spreads, such that returns1 have actually ended up to be roughly neutral on the year, but spreads2 still remain wider than at the start of the year, creating an opportunity going forward.

ARE HIGH YIELD INVESTORS BEING COMPENSATES FOR DEFAULTS?

One of the reasons spreads are slightly wider than at the start of the year is because they are compensating for an increased level of defaults within the market. Now, the expectation if we went back to March for default rates was that they were going to go significantly higher. But since then, the monetary stimulus and the fiscal stimulus has really ensured that those default rates, whilst being higher this year, won’t be anything like the expectations back in March in the depths of the Covid crisis. For us as active investors, it’s about trying to pick those companies that are going to see through this period and provide those superior returns.

CAN HIGH YIELD ISSUERS SUPPORT HIGHER BORROWINGS?

High yield issuers absolutely had to take on a greater debt burden to bridge that economic shock that we had because of the pandemic. What we’re looking for now is those companies that are looking to effectively be in balance sheet repair mode; what you would typically expect in the early part of a credit cycle, as they now look to use those revenues in a slightly improving growth scenario in order to get that level of debt back down to similar levels that they had pre-crisis.

HOW IMPORTANT IS MONETARY AND FISCAL STIMULUS?

Monetary and fiscal stimulus have been so important throughout this crisis. If we just take monetary to start, it’s almost had a threefold impact on markets. The direct impact of purchases, especially within the investment grade market, but also now within the high yield market, especially from the Federal Reserve. We also have the case that government bond rates globally are now so low that that grab for yield is really being fueled by that monetary stimulus. And then also it’s the fact that that monetary stimulus really allowed the credit markets, the high yield market, to reopen and issue bonds, to provide financing, to bridge that economic shock. Fiscal stimulus has also been key because obviously the consumer was so badly hit3 by the lockdowns that were imposed across many countries, that that fiscal stimulus ensured that the consumer is in a much better place than it would have been relative to any other crisis we’ve had.

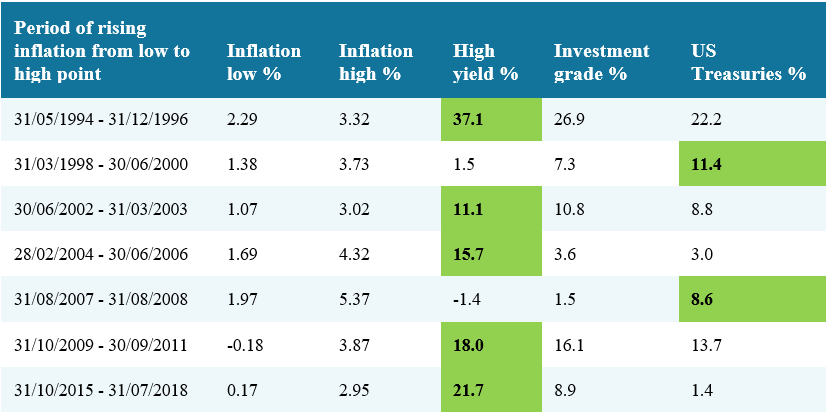

CAN HIGH YIELD TOLERATE HIGHER INFLATION?

We think high yield can tolerate higher inflation and historically tends to perform fairly well in those market environments4.

US Inflation rate and total returns of US bond indices during periods of rising inflation

Source: Refinitiv Datastream, 31 December 1993 to 30 September 2020, US All Urban Consumer Price Index annual inflation rate, total return in US dollars of ICE BofA US High Yield Index, ICE BofA US Corporate Index, ICE BofA US Treasury Index. Past performance is not a guide to future performance.

Source: Refinitiv Datastream, 31 December 1993 to 30 September 2020, US All Urban Consumer Price Index annual inflation rate, total return in US dollars of ICE BofA US High Yield Index, ICE BofA US Corporate Index, ICE BofA US Treasury Index. Past performance is not a guide to future performance.

That’s partly because of the extra spread cushion that high yield has relative to the underlying government bonds that are more sensitive to increased inflation. But also because high yield companies tend to perform fairly well in periods where prices are rising. The potential risk of higher inflation is if it is going to cause an early withdrawal from monetary and fiscal stimulus. However, if we look at the US Federal Reserve’s recent policy shift, it seems quite clear that they are willing to tolerate higher inflation and are more concerned about the Japanese experience of deflation.

Though the current landscape remains unclear, we believe investors can stay on track using a goals based income strategy. Overcome uncertainty with Janus Henderson’s income solutions designed to help you gain stability.

For Hong Kong investors, click here.

For Singapore investors, click here.

Notes

1Returns: The return on the ICE Global High Yield Bond Total Return Index was -0.3% in the first nine months of 2020. Source: Bloomberg, 31 December 2019 to 30 September 2020, in USD. Past performance is not a guide to future performance.

2Credit spread: The difference in yield of a corporate bond over a government bond of the same maturity. The spread to worst for the ICE Global High Yield Bond Total Return Index was 558 basis points at 30 September 2020, up from 382 basis points at 31 December 2019 (Source: Bloomberg, 30 September 2020). If a bond has special features, such as a call (ie, the issuer can call the bond back at a date specified in advance), the yield to worst is the lowest yield the bond can achieve provided the issuer does not default.

3Consumer confidence: For example, US consumer confidence as measured by the Conference Board Consumer Confidence Index fell to a low in 2020 of 85.7 in April 2020, this compares with a low of 25.3 in April 2009 (the low during the Global Financial Crisis). The April 2020 consumer confidence figure was higher than any of the crisis lows of the last fifty years. Source: Refinitiv Datastream, Conference Board Consumer Confidence Index, 30 September 2020.

4Inflation: Using the US as a global proxy, we can compare US high yield bonds, US investment grade corporate bonds and US Treasury bonds to show periods where inflation rose from a low point to a high point and the total returns of these three bond markets during the period. High yield performs the strongest in total and ranks first (shaded green) over the most periods.

________________________________________________