As performance within emerging market indices diverge, BlackRock’s Investment Institute favours India, Mexico and broad EM hard currency debt for the next year.

Indian and Mexican equities now form part of their biggest tactical calls – where they have the highest conviction views on a six-to-12-month time horizon.

The strategists said that the outlook for broad EM assets looks supportive as market sentiment stays positive, but avoided making an overweight call on Chinese equities.

“China’s elevated equity volatility and policy uncertainty prompt us to take above-benchmark risk elsewhere,” they said.

Indeed, Chinese stocks have vastly underperformed other emerging market markets such as Mexico and India over the past year.

Performance of MSCI emerging markets, China, India and Mexico

As a result, the relative weight of Chinese equities within the emerging market index has declined, while Mexico and India have both climbed.

At one point during 2020, China made up almost 40% of the index, whereas as of the end of January 2024, that figure has fallen to roughly 25%.

Despite making up less than 3% of the index, BlackRock’s strategists have an overweight call on Mexican equities due to the “geopolitical fragmentation” occurring between nations (particularly the US and China) as competing geopolitical and economic blocs “harden”.

“Multi-aligned or “connector” countries like Mexico are increasingly acting as intermediate trading partners between blocs,” they explained.

“The US imported more goods from Mexico than China last year for the first time since the early 2000s, US data show.”

India is another area where the strategists are bullish, due to its favourable demographics and fast-growing economy.

They said: “Many EMs benefit from young, growing populations compared with aging populations in the US and Europe. That’s one reason India – the world’s fastest-growing economy – stands out.”

“India’s talent pool, start-up ecosystem and software firms with a global footprint also make it an up-and-coming hub for artificial intelligence software, in our view.”

They believe that digital disruption and AI will be a key driver of corporate earnings, which will support the momentum of Indian stocks despite valuations near their highest levels in two decades.

The strategists said robust US economic activity, the nearing of Fed rate cuts and falling inflation all reduce recession fears and provide a boon for emerging markets.

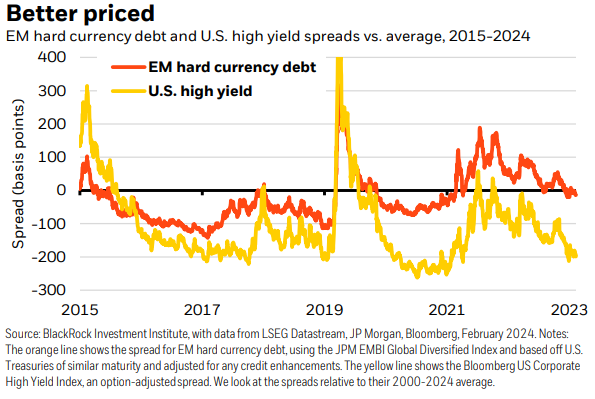

They pointed to EM hard currency debt in particular where they remain overweight due to “still attractive yields”, contrasting it with US high yield market.

The strategists noted that spreads on hard currency EM debt remain near their long-term average, whereas US high yield spreads are signalling “expensive valuations” as they remain well below their long-term average.

“We prefer EM hard currency debt and stay overweight,” they said. “Along with attractive relative value, it includes more countries with higher-quality credit ratings than riskier high yield.”

“Often issued in US dollars, hard currency EM debt is also cushioned from EM currency weakness as EM central banks cut rates,” they added.