As some investors rush out of India’s equity markets following an almost 20% correction, Allianz Global Investors’ India equity head Anand Gupta is looking to lean into risk.

In his view, the recent sell-off in the once best performing country has made valuations very attractive relative to its own history and the broader MSCI World index.

“We are letting stocks come our way; this is a godsend opportunity where you can get the stock you like at your price,” Gupta told FSA an interview.

“Momentum and growth investors are throwing in the towel,” he said. “We are GARP [growth at a reasonable price] investors. We have patience on our side. So we will let them dump and enter at [cheaper] valuations.”

“When valuations are in your favour, it is not time to be worried,” he said. “It’s time to take one step forward, be on the front foot, and express some risk in a well-thought-out way. That is what is top of mind for me.”

Gupta (pictured) believes that the recent correction may also be prompting institutional investors to enter the market.

“I’ve seen large institutional investors coming into India on a timing like this 5 or 10 years ago,” he said. “Their entry costs have been history in their own books of accounts.”

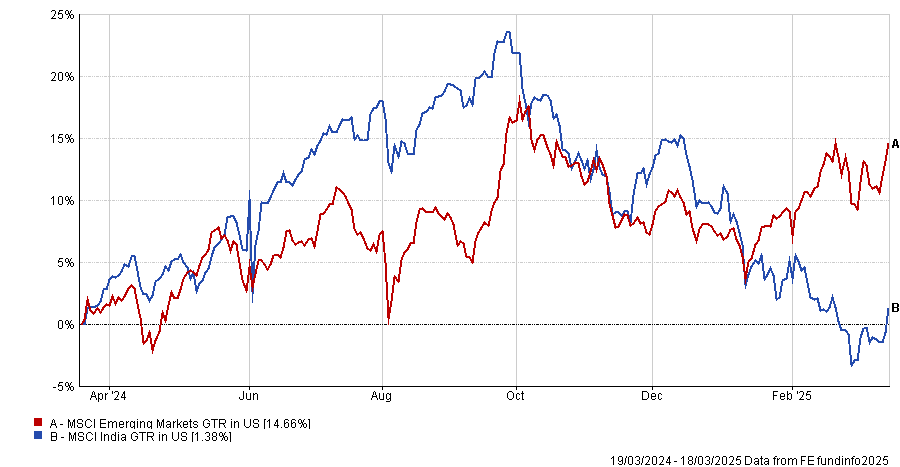

Despite the recent sell off, the MSCI India index still trades at higher price-to-earnings (P/E) multiple than the wider MSCI Emerging Markets index.

But Gupta argues that relative to the broader MSCI World index, valuations look reasonable. He notes that India’s price-to-book ratio has fallen to a two standard deviation low relative to the rest of the world.

He doesn’t think India’s stock market will ever reach valuations that will satisfy investors looking for a low P/E ratio entry point due to its market composition.

He said: “As long as India is still democratic, has a high return on equity, and a mixture of many high quality sectors, it will never trade at a low P/E because it would be like going against mathematics.”

He also expressed criticism of generalist investors and wealth managers who tend to be overly worried about valuations during a bull market in India and overly cautious during a bear market.

“When things are good, they have this view that the valuations are expensive,” he said. “But when things become cheap, meaning valuations are very attractive, then they want certainty, high visibility or growth. Both never happen.”

Just looking at a P/E ratio is not enough credible analysis for investors when assessing India, Gupta explained.

“One needs to look at return ratios and return on equity [RoE],” he said. “India has had the highest RoE within emerging markets for the last 20 years.”

He said some of this can be attributed to the fact that Indian companies tend to be more frugal with their capital allocation, and that the Indian equity market has more private companies versus state-owned enterprises (SOE’s) when compared to other emerging markets.

Additionally, Gupta argued that India has a much more diverse and higher quality mix of quality sectors, which under a democratic setup, bodes well for investors looking for RoE.

“You have to look at PEG [price/earnings-to-growth] ratios, longer term return ratios and the macro setup,” he said. The PEG ratio accounts for the trade-off between stock valuations relative to expected earnings growth.

This is one reason why he believes the current sell off is a “very good opportunity” for investors looking at India but have remained on the sidelines.

“We think within the next two quarters, you will see liquidity, economic momentum and corporate earnings all improving,” he said.

In terms of where he is seeing opportunities, Gupta pointed to consumer-led enterprises which have embraced digitisation in the longer-term phase of investing, which are finally coming towards normalised earnings.

“You will have very big earnings moves and these are becoming very interesting because they have also fallen along with this correction,” he said.

Gupta is also constructive on the outlook for industrial stocks such as renewables, because despite being sold-off, he believes they have a long runway of earnings.