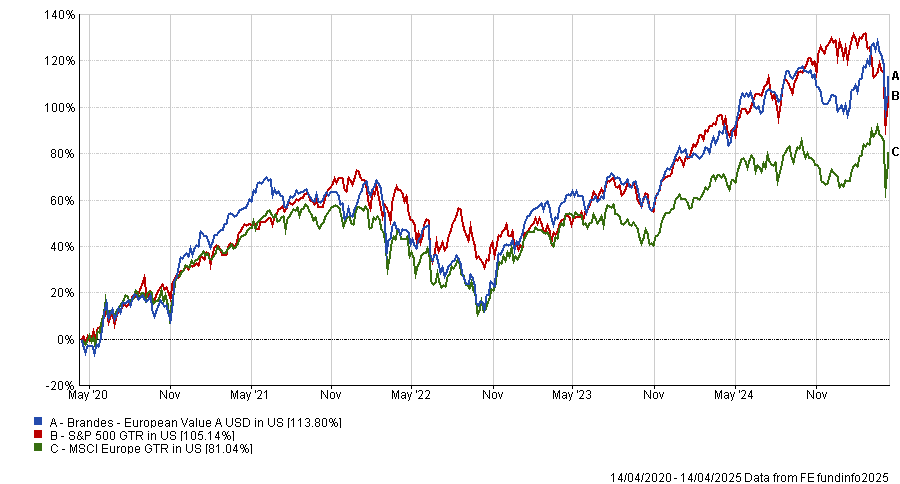

The Brandes European Value fund has been on a multi-year winning streak, outpacing virtually all of its European equity fund peers during the past five years, according to data from FE fundinfo.

The fund has even managed to beat the returns of the S&P 500 index over the same period – where most active US funds have failed to do so.

The performance boils down to a massive emphasis on price and making sure companies are cheap before buying, according to co-fund manager Jeffrey Germain.

“We really pay a lot of attention to price,” he told FSA in an interview. “We truly believe that if you buy below – not equal to – but below fair valuation, you guard yourself against things that may not go your way.”

“I think that is something that a lot of market participants do not focus on,” he said.

This process has worked well in recent years, helping the strategy to consistently outperform both its benchmark and peers despite not owning any of the US-listed mega-cap stocks that have been big drivers of the broader market.

Germain, a director at Brandes Investment Partners, suggested that many investors focus too much on the qualitative aspects of what makes a good business, such as the growth profile or the moat, without properly considering the price.

“We spend a ton of time focused on fundamentals because it helps us derive a good price to buy that business,” he said.

“Others in the market accept price as it is or they use comparative or relative valuations as a main driver – and valuation itself becomes secondary.”

Relative valuations are useful for benchmark-aware fund managers who are often forced to fill a bucket of exposure towards a sector or geography.

But Germain explained that his fund takes a benchmark agnostic approach, instead valuing stocks as business owners, and then allocating capital based on the opportunity set with the largest margin of safety.

“We do have mandatory diversification requirements, but we can really tilt the portfolio to areas where we think there’s a lot of value, and go zero in certain areas,” he said.

A focus on absolute value

Germain said the research function at Brandes is almost entirely focused on company fundamentals, with over two dozen analysts who are sector “domain experts” with coverage across market cap and geographies.

“Their job is to find [absolute] value within those sectors, not relative,” he said. “We don’t care if they know what the cheapest machinery company is – it has to be absolutely inexpensive for them to work on it.”

He added: “The stories and themes that some investors get really excited about tend to not be areas where we hunt for ideas; instead, they tend to be areas where we are selling.”

Since 2022, Germain said the opportunity set for what the firm deems as “absolute value” ideas has started to broaden out.

And while value as factor has outperformed in Europe during the past few years, Germain said the spread between value and growth is still wide – which bodes well for the approach in general.

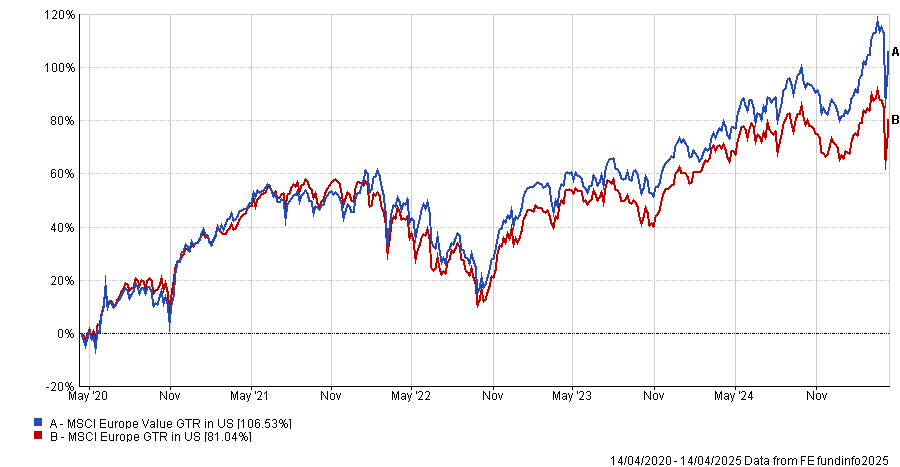

Even though a simple MSCI Value index could be “somewhat helpful” and a good starting point for investors, Germain flagged the risk of buying into value traps.

“If you’re just in the value index, you end up owning by default a large amount of financials and maybe even commodities that are trading at low multiples – but I’d argue that the earnings are high still.”

“Lower multiple businesses in general are a starting point for us, not necessarily the end point,” he said. “We’re not just looking for low P/E stocks; it’s got to be low that’s not deservingly so.”

Yet determining whether a low P/E is justified is not always obvious. What most of the fund’s winning stocks have had in common is a degree of uncertainty and a lack of positive sentiment, he said.

For example, one of the fund’s best investments was UK-listed engine manufacturer Rolls-Royce, which has surged more than 10-fold in price from its 2022 lows.

Describing the sentiment at the time of the fund’s investment into Rolls Royce, Germain said: “There was just an under-appreciation of the future and an under-appreciation of the company’s position at that moment, versus what it should have been given what the company had done from a restructuring and repositioning standpoint.”