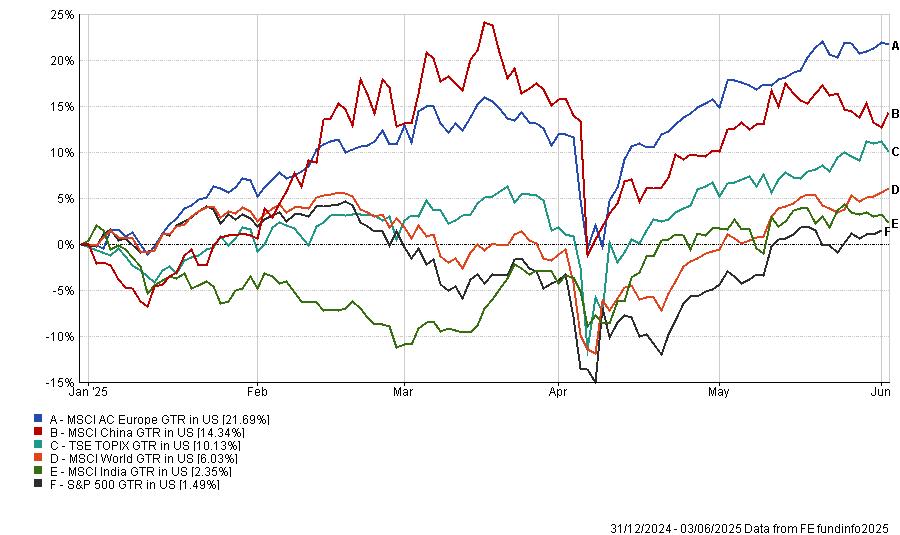

After several years of US stocks outperforming, other major equity markets are outpacing the S&P 500 index year-to-date.

Global stocks more broadly, as measured by the MSCI World index, have outperformed US stocks by almost 5% so far this year.

Although the index has a 71% weighting to US companies, other developed markets such as Europe and Japan have lifted its relative performance.

The US dollar, as measured by the US Dollar Index (DXY), has declined some 10% from its peak in January.

This has provided an added boost to other equity markets denominated in their strengthening currencies.

European equities have been one of the best performers so far this year, followed by China equities, Japan equities and India equities.

European stocks are up 21.7% year-to-date in US dollar terms. This strong performance is followed closely by Chinese and Japanese stocks at 14.3% and 10.1% respectively.

India, once a popular allocation among investors looking to benefit from a fast growing economy, has endured a correction but is still outperforming US markets year-to-date.

Below, FSA highlights the top-performing fund from each of the different major equity markets that are outpacing the S&P 500 index year-to-date*.

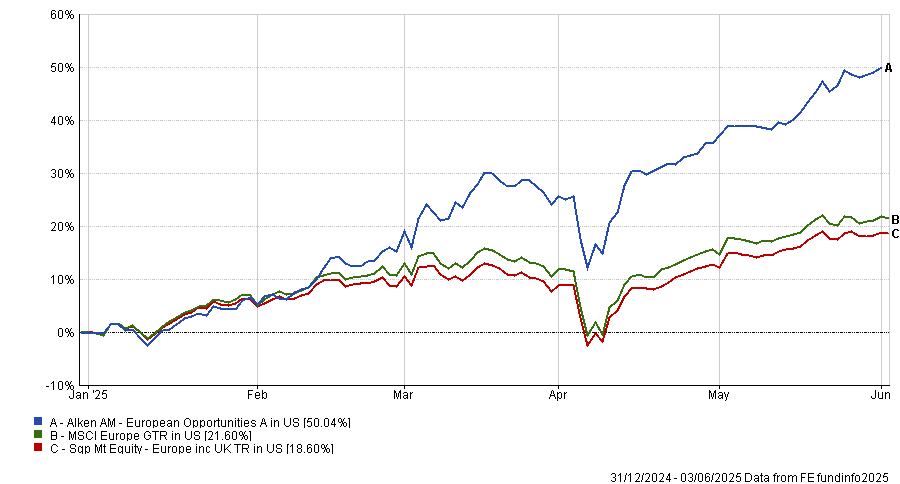

Alken AM European Opportunities

The Alken AM European Opportunities fund is up 50% year-to-date in US dollar terms. This $644m fund is managed by the firm’s chief investment officer Nicolas Walewski.

The strategy has a fairly concentrated approach, with 62 holdings. Some of the firm’s industrials stocks have been key contributors to its performance in recent months.

It has a large overweight to the industrials sector as a whole, with 28.6% invested compared with the benchmark’s 17.5%, according to its latest factsheet.

Algebris Financial Equity

Algebris Financial Equity is up 25.2% year-to-date in US dollar terms. This $957m fund is managed by Mark Conrad.

Benchmarked against the MSCI ACWI Financials Index, this financials-focused fund benefited from its large positions in European banks Barclays, Santander and BNP Paribas.

The fund manager expressed conviction in its latest factsheet, describing UK and European banks as the “clear standout active and absolute bet”.

Fullgoal China Small-Mid Cap Growth

The Fullgoal China Small-Mid Cap Growth fund is up 39.4% year-to-date in US dollar terms. This $407m fund is managed by Ning Jun and Zhang Feng.

It invests across China A-shares, Hong Kong-listed stocks and US-listed Chinese stocks.

Its top three holdings are in China Overseas Property, PDD and Morimatsu International, according to its latest factsheet.

Franklin Templeton Japan

The Franklin Templeton Japan is up 20.5% year-to-date in US dollar terms. The $194m fund is managed by Ferdinand Cheuk and Chen Hsung Khoo, out of Hong Kong and Singapore.

It invests primarily in large-cap stocks listed in Japan, and relative to its benchmark has an overweight to financials and underweight to information technology, according to its latest factsheet.

Its largest three positions are in Mizuho Financial Group, IHI Corp and Ryohin Keikaku.

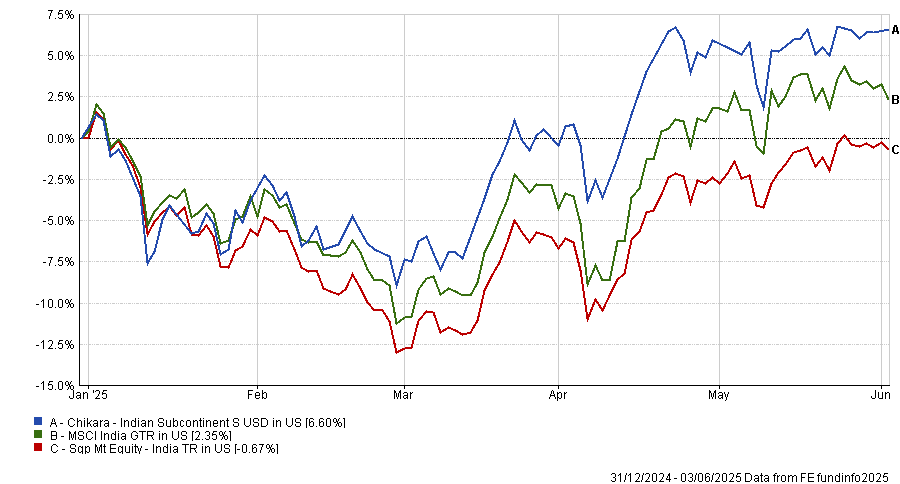

Chikara Indian Subcontinent

Chikara Indian Subcontinent is up 6.6% year-to-date in US dollar terms. This $125m fund is managed by Abhinav Mehra and Andrew Draycott.

They run a concentrated portfolio of between 25 and 40 stocks, and focus on companies they believe will benefit from the economic transformation of India.

Its top holdings are in Kotak Mahindra Bank (8.6%), HDFC Bank (7.1%) and Delhivery (6.6%).

* The data is based on year-to-date trailing performance ending 3/6/2025. Only funds over $100m in assets under management and fall under the relevant Hong Kong SFC Authorised Mutual or Singapore Mutual sectors as classified by FE fundinfo were considered.