UBS AM: Managing the ‘disconnect between the macro and micro’

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

Listed subsidiary takeouts have been a boom for active value managers in Japan betting on the unwinding of so-called ‘parent-child’ listings.

The partnership includes prominent brand visibility, alongside access to premium hospitality.

The partnership includes prominent brand visibility, alongside access to premium hospitality.

There are no changes to the leadership of the underlying investment teams.

Sponsored by Loomis Sayles & Natixis

The Growth Equity Strategies Team at Loomis Sayles, an affiliate of Natixis Investment Managers, demonstrates that patience, discipline and conviction result in consistent, peer-leading risk-adjusted compounding over cycles.

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

The partnership includes prominent brand visibility, alongside access to premium hospitality.

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

Listed subsidiary takeouts have been a boom for active value managers in Japan betting on the unwinding of so-called ‘parent-child’ listings.

This week FSA provides a quick comparison of two US equity funds: Brandes US Value and JP Morgan US Value.

This week FSA provides a quick comparison of two US equity funds: Brandes US Value and JP Morgan US Value.

This week FSA compares the First Sentier Global Listed Infrastructure fund and M&G Global Listed Infrastructure fund.

Listed subsidiary takeouts have been a boom for active value managers in Japan betting on the unwinding of so-called ‘parent-child’ listings.

Listed subsidiary takeouts have been a boom for active value managers in Japan betting on the unwinding of so-called ‘parent-child’ listings.

Cameron Sinclair has been hired to lead the firm’s institutional distribution in Australia.

Listed subsidiary takeouts have been a boom for active value managers in Japan betting on the unwinding of so-called ‘parent-child’ listings.

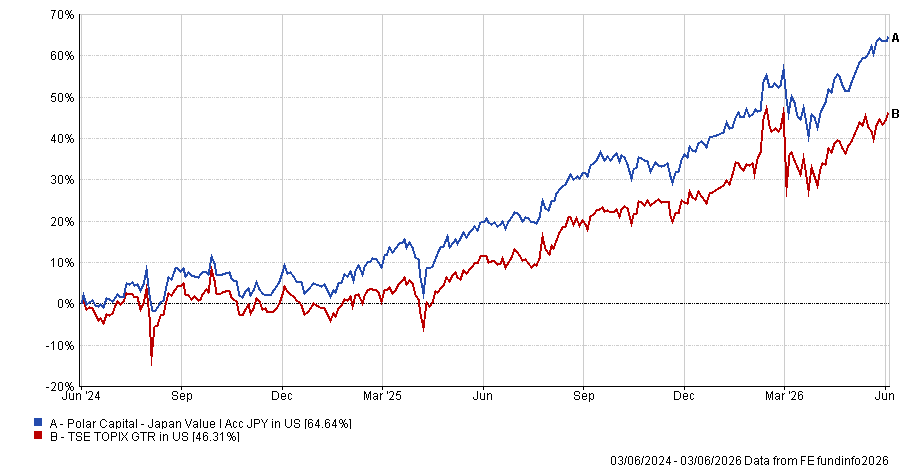

There is still value to be found in Japanese small- and mid-cap stocks as more listed subsidiaries get bought out or taken in by their parents.

This is according to Chris Smith, co-manager of the $422m Polar Capital Japan Value fund, whose strategy has been outperforming on the back of a recent acceleration of an unwinding of “parent-child listings”.

Smith said: “One of the baskets that was really successful for us was our listed subsidiary basket, and it’s a theme we’ve been playing since 2016.”

“There used to be 400 of these in Japan and they are very rare overseas because it creates a massive conflict of interest for shareholders.”

These listed subsidiaries – where more than 50% is owned by another listed company – are more common in Japan compared with the rest of the world with over 200 “parent-child listings” still remaining.

“Since 2016, Japan has been trying to get away from those structures as part of the corporate governance improvements, and that’s something we’ve been targeting,” Smith said.

In the last year alone, the fund’s portfolio has seen five listed subsidiaries taken in by their parents or sold off. There was also a failed takeover bid and two stocks driven up by the speculation of an incoming takeover bid.

“That is a huge acceleration, but not only for us,” Smith said. “We’ve been averaging around two per year prior to 2025 and then we saw five successful bids last year.”

Over the past two years, the Polar Capital Japan Value fund is up 64.4% compared with the TSE TOPIX return of 46.3%.

Smith attributes this acceleration to recent reforms which stipulated that any listed subsidiary had to have a majority independent board or an audit committee to oversee the relationship with the parent.

“We think that has served as a motivator for those parents to take them in, because effectively, if you’re going to have an independent board, you can lose control of that company,” he said.

“For a company to own 51% of another company and have it consolidated, that is an important unit for that business. So, we think the motivation is there.”

He expects there will be a further acceleration to this theme and predicts that there will only be a few of these parent-child listings left in the market in the coming years.

However, getting exposure to the listed subsidiary theme is not as simple as buying all the parent-child listings in a passive basket and waiting.

Smith said it is important investors meet with management teams to determine whether the parent genuinely views the listed subsidiary as an important part of their business and will want to retain control.

He also said the time horizon of a likely sale is important because “if you’re getting a 30% takeover bid in 10 years, you’re averaging a 3% per annum and you’re not going to outperform”.

“Whereas if this is short term opportunity over one or two years the return can be very impactful,” he added.

“When you sit down with management and discuss the synergies and why the synergies exist and the opportunity to realize more in the future, you get a really good understanding as to whether the takeover is likely.”

A more granular, thematic approach is increasingly necessary for multi-asset investing, says UBS AM’s asset allocators.

Listed subsidiary takeouts have been a boom for active value managers in Japan betting on the unwinding of so-called ‘parent-child’ listings.

This week FSA provides a quick comparison of two US equity funds: Brandes US Value and JP Morgan US Value.