Since the end of last year, Sino-US tensions have led to US sanctions and investment restrictions on Chinese companies. Meanwhile, domestic policy tightening has weighed on China credit, Sheldon Chan, portfolio manager at T Rowe Price told a media briefing.

The impact has been largely concentrated in the China property sector, prompting yield spread widening in some issuers, such as China Fortune Land, and most recently a significant sell-off the bonds of debt-burdened China Evergrande.

“In the middle of last year, we saw signs of geopolitical tension pointing towards US sanctioning Chinese companies. So, we started to trim a lot of China investment grade positions and diversified exposure from China and Hong Kong, towards Southeast Asian markets, including Thailand, Malaysia, and Singapore,” Chan said.

But subsequently, he has found opportunities to add back some exposure, because valuations had cheapened. As a result, his strategy’s net allocation to China hasn’t change much, he said.

Chan has managed the $60.3m T Rowe Price Asia Credit Bond Fund since last year, and the strategy is mainly focused on US dollar-denominated fixed income securities in Asia ex Japan.

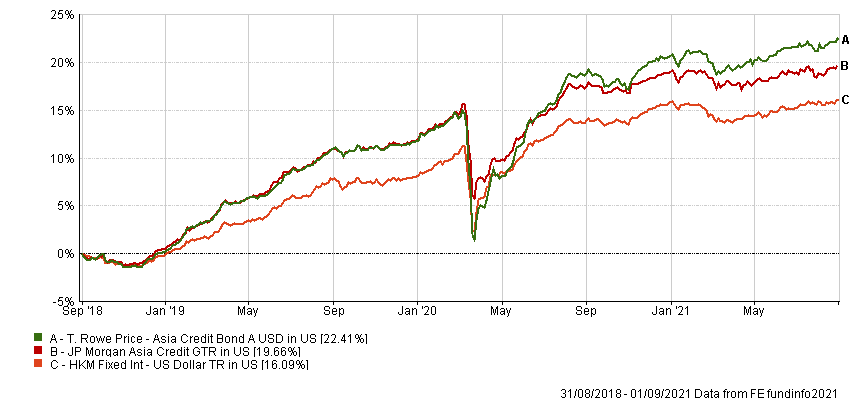

The fund has posted a three-year cumulative return of 22.41%, according to FE Fundinfo, compared with a sector average return of 16% and its benchmark return of 19.66% as at 1 September 2021.

The top five holdings are sovereign bonds issue by the Philippines and Indonesia, Pertamina Persero PT, Axiata SPV2 and Shinhan Bank; and in terms of geographic allocation, its main weighting is to China (28.9%), followed by India (13.6%), Indonesia (12.2%), Philippines (9.1%) and Hong Kong (7.5%). The predominant credit rating of the holdings is BBB, according to the fund factsheet.

Chan also reminded investors to beware assuming “implicit” government support of SOEs in China. More than 30% of the JP Morgan Asia Credit Index, the fund’s benchmark, comprises SOEs or quasi- sovereign debt.

“Historically you’ll find that the government will only react to and provide support for these types of entities when it’s a little bit too late in the day. I think at the episode we’ve seen with Huarong (China’s largest bad-debt manager) this year is a good example of that,” he explained.

Investors need to be selective when they look at SOE names, Chan stressed, and must consider the standalone credit profile of bond issuers, as well as assessing the likelihood of government support.

The markets have typically priced SOEs in such a way that there is little spread dispersion. Spreads have been compressed and fairly homogeneous throughout the SOE universe, he said.

“But I think things have changed over the past few months; there’s been a much broader reassessment of previous assumptions about government support.”

Investors are now seeing greater spread dispersion between some of the stronger or more strategic SOEs, compared with the weaker or more commercial ones. Chan is certain that dispersion is here to stay.

T Rowe Price Asia Credit Bond Fund vs benchmark and sector average