Sherwood Zhang, Matthews Asia

Matthews Asia remains constructive on China’s equity earnings growth outlook and continues to seek out investments at reasonable valuations, Sherwood Zhang, fund manager at Matthews Asia, told FSA.

China is one of the first countries to normalise monetary policies post the Covid-19 pandemic and, therefore, it may have more monetary and fiscal flexibility to support the economy as needed, he said.

However, in the near term, due to high base effects and increased regulatory risk, there could be down-side risk to Chinese corporates’ earnings. “When these potential earnings downgrades are fully discounted, the market should refocus on structural growth drivers to corporate earnings,” Zhang said.

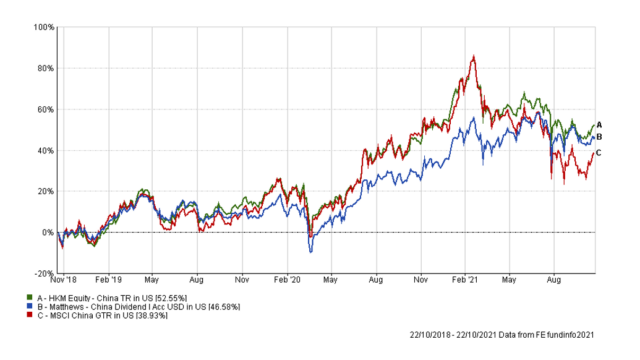

The $19.6m Matthews China Dividend Fund managed by Zhang has posted a 46.58% three-year cumulative return in US dollar, as compared with a 38.93% return by its benchmark MSCI China index and 52.55% by its sector average, according to FE fundinfo.

As at 31 August of 2021, the fund’s main sector allocations are consumer discretionary, information technology, industrials, communications services and consumer staples. Its top five holdings are: Tencent, Shanghai Baosight Software, China Suntien Green Energy, Bosideng International and Postal Savings Bank of China.

First half earnings results in China showed continued Covid recovery and were generally encouraging across the board, except for a weaker recovery in some parts of consumption sector, such as consumer staples, according to Zhang. The results also shed some light on potential government directives over the next year, which Zhang believes will be positively directed toward China’s efforts at increased domestic self-sufficiency across a myriad of supply chains (for example, technology and health care) and environmental efforts to further promote green energy developments.

“We believe that there are many opportunities in China that stand to benefit positively from these developments and expect to see meaningful volume expansions, helping to drive positive earnings growth across these supported industries,” he said.

Sector opportunities

Moreover, the pandemic has accelerated a structural transition from offline to online economic growth that was already taking place. Technology is at the forefront of several long-term, secular trends that are driving growth in the region, argued Zhang.

Continuing trade tensions between the U.S. and China are driving the growth of indigenous technology businesses in China as the country seeks to be less reliant on U.S. imports, he added.

Zhang is also positive on the healthcare sector as Asia’s consumers will continue to play an important role in the growth of health care-related services, with patients seeking better quality care and services as incomes rise.

“We also see opportunities in contract research organisations (CRO) companies. China has the largest number of STEM (science, technology, engineering and mathematics) graduates in the world, and CROs are capitalizing on China’s research and engineering talent pool at a lower labour cost compared to developed markets,” Zhang added.

However, Zhang believes that for international retail investors, timing their investment in China is hard. Investors tend to rush into China during periods of high historical returns or exciting economic growth, and they tend to exit the market equally rapidly.

“In my view, this current cycle is no different. Thus, instead of timing the market, investors should really decide whether China belongs in their long-term portfolio; if it does, then stick with a strategy best fit for their long-term goal,” he said.

After the recent selloff of Chinese equities, it is important for investors to recognise that one cannot blindly believe Chinese internet companies will follow the route of US internet giants in a “winner-takes-all-game, “as the culture and regulatory environment are totally different”.

“That’s why investors must have a true local perspective to analyse Chinese companies,” Zhang said.

Matthews China Dividend Fund vs benchmark and sector average